It’s not the 1930s so…

Currency wars are either everywhere or nowhere. We know that much.

What we also probably know is that currency devaluations in today’s environment are indeed approaching beggar thy neighbour policy without commitments to be irresponsible and/ or supportive fiscal action.

HSBC’s Stephen King broadly agrees.

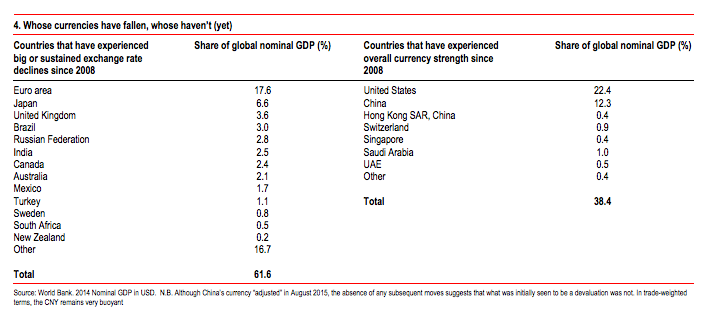

Devaluations alone, although the path of least resistance and very probably the primary avenue through which monpol seems to work, just aren’t going to cut it anymore. Yes, says King, “a small country might benefit from a major currency decline but, since the latest bout of currency wars began in 2008, three-fifths of the world economy has devalued or depreciated against the remaining two-fifth”.

(Note China and note that stability following its trip to band camp is what most analysts are predicting. Other see another larger deval as nailed on, of course. We’re going to be contrarian and say we don’t know)

And, says King, “the aggregate effect of currency declines has failed to reduce the risk of deflation at the global level and, by adding to uncertainty, may have limited the size of the trade multipliers more typically associated with post-war economic recoveries. Ultimately, the world as a whole cannot devalue.”

It’s something we’ve heard David Woo say before and Eichengreen rebut with caveats.

Caveats that King builds on. His ultimate point being that for devaluations to work at the global level they need to signal a major revolution in domestic monetary (and fiscal) regimes. Something, he argues, the 1930s did:

There are four alternatives [to currency devaluations taking the world to a cliff edge -- his phrasing, we quickly stress]:

The first, and probably the most fatalistic, is to accept that monetary policy can do little more to boost economic growth. The world’s major industrialised nations have been slowing down decade by decade (see chart 21). This appears to reflect a series of structural constraints that are unlikely to be influenced significantly by monetary policy. More needs to be done on the supply-side as opposed to the demand-side, in particular in order to tackle the persistent absence of decent productivity growth....MORE