July 31, 2015: "Electricity from natural gas surpasses coal for first time, but just for one month"

From the Energy Information Administration's Today in Energy:

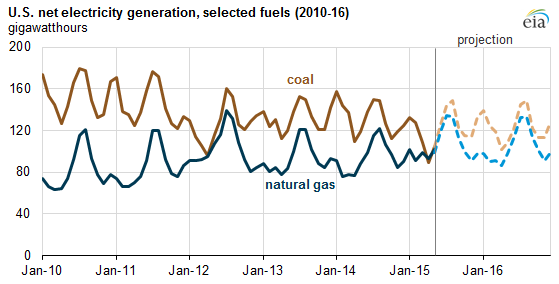

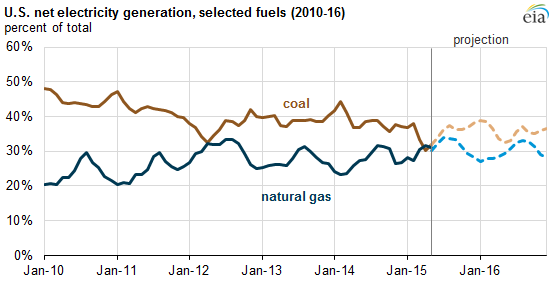

Source: U.S. Energy Information Administration, Electric Power Monthly and Short-Term Energy Outlook, July 2015

In April, traditionally the month when total electricity demand is lowest, U.S. generation of electricity fueled by natural gas exceeded coal-fired generation for the first time since the start of EIA's monthly generation data in 1973. However, EIA's latest Electric Power Monthly shows that coal's generation share once again exceeded that of natural gas during May. Total generation from coal and natural gas in May increased 14% from its April level, with increased coal generation accounting for 65% of the combined increase.

Total generation from coal- and natural gas-fired generators is seasonal: higher during summer and winter months when electricity demand is highest, and lower in the spring and fall when electricity demand is lower. Many units take advantage of these months of low demand to schedule maintenance. As demand increases towards its summer peak level, the utilization rates for both coal- and natural gas-fired units tend to rise.

In April 2012, the last time monthly natural gas generation came close to surpassing coal-fired generation, spot prices for natural gas were near $2 per million Btu ($/MMBtu) on a monthly average, before returning to about $3.50/MMBtu in the last months of 2012. Low natural gas prices make gas-fired generation economically attractive during periods of low demand when operators in many parts of the country have more flexibility to choose between coal- and natural gas-fired units based on their dispatch cost.

On an annual average basis, coal has lost generation share to natural gas and, to a lesser extent, renewables. The current downward trend in coal-fired generation began in 2007, when increased U.S. production of natural gas (particularly from shale) led to a sustained downward shift in natural gas spot prices and increased generation from natural gas-fired generators.

Source: U.S. Energy Information Administration, Electric Power Monthly and Short-Term Energy Outlook, July 2015

Monthly coal-fired generation is expected to continue exceeding natural gas-fired generation for the remainder of 2015, as natural gas prices slowly rise from their April average price of $2.61/MMBtu to about $3.30/MMBtu by December....MORESeptember's $2.715 down 5.3 cents.

I don't know if that price call is going to pan out, what with El Niño and all. It appears we are about to break the trendline of higher lows from the late April lows. If that happens the market may be telling us something about expected demand this winter.