...note: the transmission effect of allowing the instruments to mature is not nearly as instantaneous as the opposite action of open-market purchases. In the case of a roll-off the treasury (or Fannie and Freddie) simply pay the Fed cash for the maturing amount. It is not as if the Fed is selling into the market.From Wolf Street, May 3:

The actual effect would come in later Treasury (or agency) debt offerings when the size of subsequent auctions would be increased to fund maturing debt, interest due and new deficits....

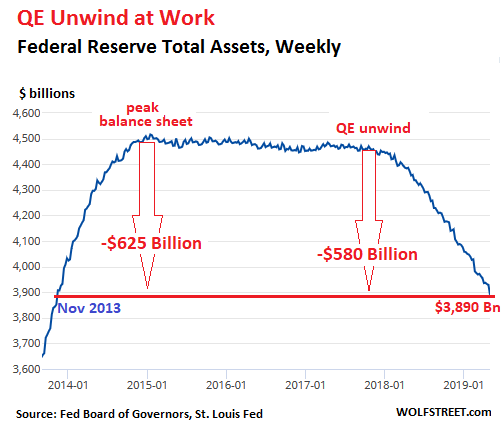

Fed sheds $46 Billion, Total QE Unwind Reaches $580 Billion. Assets drop to lowest level since Nov 2013.

In April, total assets on the Fed’s balance sheet fell by $46 billion, as of the balance sheet for the week ended May 1, released Thursday afternoon. This drop reduced the assets to $3,890 billion, the lowest since November 2013. Since the beginning of the “balance sheet normalization” process, the Fed has shed $580 billion. Since peak-QE in January 2015, the Fed has shed $625 billion:

According to the Fed’s old “balance sheet normalization” plan, which was still on autopilot in April, the QE-unwind would shed “up to” $30 billion in Treasuries and “up to” $20 billion in mortgage-backed securities (MBS) a month for a total of “up to” $50 billion a month, depending on the amounts of bonds that mature that month.

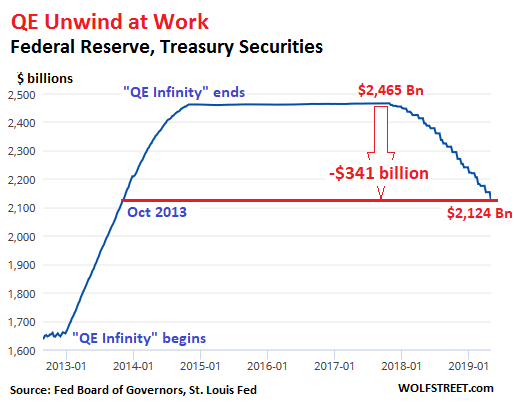

Treasury Securities

The Fed doesn’t actually sell its Treasury securities but allows them to “roll off” without replacement when they mature at mid-month or at the end of the month.

On April 15, $10 million in Treasury Inflation-Protected Securities (TIPS) and $169 million in Treasury securities in the Fed’s portfolio matured. On April 30, two issues of Treasuries matured, totaling $28 billion. Since all of it combined was below the $30-billion “cap,” all of it rolled off without replacement. This brought the Fed’s Treasury holdings down to $2,124 billion, the lowest since October 2013:

Mortgage-Backed Securities (MBS)The residential MBS that the Fed still holds were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. All holders of MBS, including the Fed, receive pass-through principal payments as the underlying mortgages are paid down on a monthly basis with each mortgage payment, or are paid off when the house is sold or the mortgage is refinanced. The remaining principal is paid off at maturity.......MUCH MORE