The 2014 Atlantic hurricane season is officially underway on Sunday,

June 1. What will this year's hurricane season bring? My top six

questions for the coming season:

1) When will the first "Invest",

tropical depression, and named storm of the 2014 Atlantic hurricane

season form? We have a chance of all three of these events occurring in

the Gulf of Mexico during the first week of hurricane season, though the

models are currently hazy about this. An area of disturbed weather in

the Eastern Pacific located a few hundred miles south of Southeast

Mexico is forecast to move slowly northwards towards the Gulf of Mexico

Sunday through Tuesday. In their 8 am EDT Friday Tropical Weather Outlook, NHC gave this system a 50% chance of developing into a tropical depression or tropical storm by Wednesday. The 06Z Friday run of the GFS model

predicts that this disturbance will make landfall in Southeast Mexico

on Tuesday, then spread moisture northwards over the Gulf of Mexico late

in the week. The model predicts that wind shear will be light to

moderate over the Gulf late in the week, potentially allowing the

disturbance to spin up into a tropical depression. The 00Z Friday run of

the European model has a different solution, predicting that the

Eastern Pacific tropical disturbance will remain south of Mexico through

Friday.

However, the model suggests that moisture streaming into the

Gulf of Mexico late in the week will be capable of spawning an area of

low pressure with the potential to develop in the Southern Gulf of

Mexico's Bay of Campeche. In any case, residents of Southeast Mexico and

Western Guatemala appear at risk to undergo a multi-day period of very

heavy rainfall capable of causing flash flooding and dangerous mudslides

beginning as early as Monday. This disturbance may cross over Mexico

and into the Gulf of Mexico and create the Atlantic's first "Invest"

with the potential to develop late in the week, sometime June 5 - 7.

Figure 1.

Satellite image taken at 7:45 am EDT Friday May 30, 2014, showing an

area of disturbed weather a few hundred miles south of Southeast Mexico.

Will this disturbance cross over into the Gulf of Mexico and create the

Atlantic's first "Invest" of 2014 late in the week? Image credit: NASA/GSFC.

2) All of the major seasonal hurricane forecasts

are calling for a below-average to near-average season, with 9 - 12

named storms, 3 - 6 hurricanes, and 1 - 2 major hurricanes. Hurricane

seasons during the active hurricane period 1995 - 2013 averaged 15 named

storms, 8 hurricanes, and 4 major hurricanes. Will an El Niño event

indeed arrive, bringing reduced Atlantic hurricane activity, allowing

the pre-season predictions to redeem themselves after a huge forecast

bust in 2013?

Affordable drones are flooding the market. Our current favorites: The

capable DJI Spreading Wings S1000 and the budget-minded Blade 180 QX HD.

DJI Spreading Wings S1000

Price: $3600 Diagonal width: 41.1"

Flaunting eight powerful blades on retractable carbon-fiber arms, the

S1000 octocopter is as steady as it is daunting. The remote-controlled

workhorse lugs up to 15 pounds of camera equipment—enough to shoot next

summer's blockbuster. What's more, the UAV stays aloft for 15 minutes

and can maintain stability even in the event of a midair rotor loss.

Watching the attachable lower gimbal fluidly move to keep a camera

steady as its rotors maneuver above is almost creepy.

Blade 180 QX HD

Price: $150 Diagonal width: 11.5"

The 180 QX is compact enough to land on the palm of your hand, but this

3.3-ounce bot packs a lot of tech under its shell. With the drone's

adjustable flight-stability software, built-in 720-pixel camera, and

intuitive remote control, it flies smoothly for 10 minutes per charge

and delivers quality video that easily competes with its larger

rivals'—at a fraction of the cost. Ready to go right out of the box,

it's an ideal starter for the uninitiated.

A SENIOR executive at Macquarie Group was involved in establishing a

fake family office to extract confidential financial information from a

competitor.

An investigation by The Australian Financial Review

has found that Tim Hornibrook, head of Macquarie Agricultural Funds

Management, obtained sensitive details about a competitor's profits, fee

structure and returns by posing as a wealthy investor.

Mr

Hornibrook sought the information on his competitor at a time when

Macquarie was trying to raise $700 million through the investment

vehicle Macquarie Crop Partners, sources said.

An email was sent

in late 2011 from a Macquarie office in London claiming to be from a

private investor called the Brook Family Office.

Using the

address investments@brookfo.com, the email said the fictitious company

was considering investing in the fund and needed detailed financial,

performance and organisation information. The competitor, believing it

was a legitimate potential investor, provided a detailed response days

after receiving the email.

The email's details show it originated

from the computer of a junior marketing employee at Macquarie Funds in

London. A Macquarie spokesman said the bank "expects the highest

standards of its employees and will be fully investigating this matter".

Mr Hornibrook, a well-known figure in agribusiness investment,

did not respond to questions put to him through Macquarie. The

revelations are likely to focus attention again on how it conducts

business at a time when global investment banks are still under fire for

their role in the global financial crisis.

The competitor that unwittingly disclosed the information to Macquarie

does not wish to be named and is considering taking legal action....MORE

"1 billion, gagillion, fafillion, shabolubalu million illion yillion..."*

From Barron"s:

There are a million ways to die in the market–and A Million Ways to Die in the West. The former we’ll get to in a minute; the latter is a new movie from the Family Guy’sSeth MacFarlane that spoofs films like Once Upon a Time in the West, AFistful of Dollars and any number of classic westerns. Rolling Stone’s Peter Travers gives A Million Ways to Die a middling review but notes that “there are lots of ways to die laughing at this Western raunchfest,” while the Wall Street Journal’sJoe Morgenstern says it’s “seldom as funny as it promises to be.” The New York Times Stephen Holden says you “might call the movie ‘Revenge of the Übernerd.’” A Million Wayswon’t top the box office–that honor will go toWalt Disney’s (DIS) Maleficent–but if nothing else its a reminder of just how nasty, brutish and short life was back in the good old days of the Wild West.

Just like trading in the markets. The financial markets love to

punish those who think they know all the answers, and that’s exactly

what they’ve done this year. Very few people thought Treasury yields

would fall this year, but that’s exactly what they’ve done. And no one

expected the complete wash out in high-flying stocks like Twitter (TWTR) and Amazon (AMZN), but that’s exactly what we got.

Now everyone is simply confused. Sure, the S&P 500 gained 1.2% to 1,923.53 this week–another record high–while the Dow Jones Industrial Average rose 0.7% to 16,717.17–also a record high. The Nasdaq Composite jumped 1.4% to 4,242.62. The CBOE Volatility Index, also known as the VIX, fell to 11.40. That’s very low.

Strategists, however, would like to see bigger gains from the beaten-down Russell 2000, which advanced just 0.7% to 1,134.50 and continues to lag big caps. The 10-year Treasury yield

fell 0.19 percentage points to 2.46% this week, the third lowest this

year–causing more worry among those who think the bond market is always

right.

The mixed signals were apparent even among the S&P 500′s best performing stocks, including Exelon (EXC), a utility that’s nearing completion of a merger with Pepco Holdings (PHI), and Priceline (PCLN),

a high-flying internet stock that rose, well, because it could. Exelon

gained 7.9% to $36.83 this week, while Priceline rose 6.8% to $1,278.63.

Bespoke Investment Group sums up the market’s vibe:

It was a short week for traders and investors due to the

Memorial Day holiday on Monday, but that didn’t stop the market from

continuing to amaze (or confuse) as many as possible. In a week where Q1

GDP was revised down to negative 1% on an annualized basis, which was

the lowest level of growth in three years, the S&P 500 followed

through from last week’s peek to new highs and continued to trade at

levels never before seen.

Citigroup’s Robert Buckland and team aren’t worried about falling bond yields:

This year’s rally in US Treasuries has caught most

investors by surprise. 10 year yields have fallen from 3.0% at the start

of the year to 2.4% at present, despite the previous consensus

expectation of yields rising towards 3.25% by the end of the year. So

why has the US bond market caught so many out? Perhaps the most obvious

reason is that too many investors were already positioned for a further

increase in treasury yields. There has been a classic bear squeeze....MORE

*That's Dr. Evil's demand (in Yen) in the third Austin Powers film about which Wikipedia comments:

This time his demand is met with simple confusion from the world leaders.

Because the last thing you need is some grizzled old time-traveler looking at you and sneering "Rookie". (it's all about how to think)

From Quirkbooks:

Author's Note: I assume that some day, this article will serve as

an invaluable guide and warning for our time traveling ancestors-to-be

(who will of course be unable to read books and learn these lessons for

themselves, either because [a] all the books will have been burned, or

[b] kids will have stopped reading books entirely, because grumble

grumble, god damn kids, when I was your age, video games, blah blah,

detriment to society, buncha hooligans, kids these days, no respect,

etc). In the meantime, just enjoy it for all of its delightfully

entertaining/convoluted/paradoxical pleasures.

As anyone who’s anyone who’s read any time travel story ever could

easily tell you, time travel is a tricky subject. Temporal paradoxes

might seem simple and straightforward at the start (no they don’t), but

they always devolve quite quickly (linear time-wise) into some sort of

trippy, philosophically complicated, timey-wimey conundrum that makes

even the most convoluted middle school relationship make sense by

comparison. Come to think of it, maybe the reason that all those cool

kids in middle school suffer from impossibly complicated and

melodramatic romances to begin with is because they’re all too “cool” to

read time travel stories in the first place, which would obviously

teach them the benefits of temporally linear dating, if nothing else.

I’m looking at you, River Song.

For the most part, any paradox related to time travel can generally

be resolved or avoided by the Novikov self-consistency principle, which

essentially asserts that for any scenario in which a paradox might

arise, the probability of that event actually occurring is zero -- or,

to quote from LOST, “whatever happened, happened,” meaning that no

matter what anyone does, they can’t actually create a paradox, because

the laws of quantum physics will self-correct to avoid such a situation.

Still, I’m wary of such a loose explanation for things, and so below,

I’ve compiled a list of a few of the more popular time travel paradoxes

-- and what to do to avoid them.

ONTOLOGICAL PARADOX: Also known as the “Bootstraps

Paradox,” an ontological paradox arises when a person or object is sent

through time and recovered by another person, whose actions then lead to

the original person or object back to the time from when it came in the

first place, thus creating an endless loop with no discernible point of

origin. Thus, the original person or object is essentially “pulling

itself up by its own bootstraps,” hence the nickname (thanks in no small

part to the Robert Heinlein story “By His Bootstraps”).

Example: The Terminator films are a prime and

popular example of the Ontological Paradox. In the future, a Terminator

is sent back in time to kill the mother of resistance leader John Connor

before he is born. While the original T-800 is ultimately destroyed,

the leftover pieces are found by scientists who use the technological

to...develop and create Skynet, and the Terminator-series robots. Skynet

would have never been created if Skynet hadn’t taken over the world and

then sent a Terminator back in time to get destroyed and ultimately

lead to the creation of Skynet. Trippy, right?

There's also the fact that Future John Connor sends his buddy Kyle

Reese back in time to protect his mother from the T-800, only Kyle ends

up totally bangin' John's mom (dude high five! I mean, not cool, man)

and impregnates her with his buddy John Connor. So to top it all off, if

John hadn't sent his friend back in time, his friend would never have

had sex with John's mom, and John would never have been born (meaning

that Kyle Reese is either the best or worst friend, ever).

How to Avoid: No one’s really sure if a real-life

ontological paradox would lead to some massive hemorrhaging of

spacetime, or if the closed loop is kind of automatically self-corrected

since it all works itself out evenly in the end anyway. Still, better

to avoid these kind of complicated situations, and the best way to do

that would simply be to stop taking candy from strangers -- “candy” in

this case being mysterious or alien artifacts with questionable origins,

possibly given to you by mysterious people who may or may not come from

the future. See? Maybe all those warnings that your Mom gave you when

you were a little kid still mean something today. Or maybe all along she

was just trying to prevent you from sending your friends back in time

to sleep with her. Or perhaps encourage it....MUCH MORE

I am reasonably competent at manipulating language and other symbols,

and in recognizing the techniques of rhetoricians and homilists.*

Sometimes though, politicians baffle me....

*Sting nailed it in "De Do Do Do De Da Da Da"

Poets, Priests and Politicians

Have words to thank for their position

Words that scream for your submission

And no-one's jamming their transmission

'Cos when their eloquence escapes you

Their logic ties you up and rapes you...

Back in the '90s I was approached by some guys who thought they had "the breakthrough" to make VR real but they just couldn't solve the 'uncanny valley'*. I'm not sure that Oculus Rift has either but it's much closer.

From Wired:

As he flew from Orange County to

Seattle in September 2013, Brendan Iribe, the CEO of Oculus, couldn’t

envision what the next six months would bring. The rhapsodic crowds at

the Consumer Electronics Show. The around-the-block lines at South by

Southwest. Most of all, the $2 billion purchase by Facebook. That fall

Oculus was still just an ambitious startup chasing virtual reality, a

dream that had foiled countless entrepreneurs and technologists for two

decades. Oculus’ flagship product, the Rift, was widely seen as the most

promising VR device in years, enveloping users in an all-encompassing

simulacrum that felt like something out of Snow Crash or Star Trek.

But it faced the same problem that had bedeviled would-be pioneers like

eMagin, Vuzix, even Nintendo: It made people want to throw up.

This was the problem with virtual reality. It couldn’t just be really

good. It had to be perfect. In a traditional videogame, too much

latency is annoying—you push a button and by the time your action

registers onscreen you’re already dead. But with virtual reality, it’s

nauseating. If you turn your head and the image on the screen that’s

inches from your eyes doesn’t adjust instantaneously, your visual system

conflicts with your vestibular system, and you get sick.

There were a million little problems like that, tiny technical

details that would need to be solved if virtual reality were ever to

become more than a futurist’s fantasy. The Rift had made enough headway

to excite long-suffering VR enthusiasts, but it was still a long way

from where it needed to be.

“This is the first time that we’ve succeeded in stimulating parts of the human visual system directly.”

But then Iribe got a call from Michael Abrash, an engineer at Valve;

the gaming software company had conducted VR research for a while and

had begun collaborating with Oculus. Valve had a new prototype, and it

didn’t make people sick. In fact, no one who had tried the demonstration

had felt any discomfort. Iribe, who was famously sensitive to

VR-induced discomfort—“cold sweat syndrome,” he calls it, or sometimes

“the uncomfortable valley”—flew up to Valve’s offices outside Seattle to

be the ultimate guinea pig.

Abrash escorted Iribe into a small room tucked off a hallway. The

walls and ceilings were plastered with printouts of QR-code-like symbols

called fiducial markers; in the corner, a young engineer named Atman

Binstock manned a computer. Connected to the computer was Valve’s

prototype headset—or at least the very beginnings of a headset, all

exposed circuit boards and cables. Iribe slipped it over his head and

found himself in a room, the air filled with hundreds of small cubes.

He turned his head to look behind him—more floating cubes. Cubes to

the left, cubes to the right, cubes overhead, floating away into

infinity. Iribe leaned forward and peered around to see the side of the

cube closest to him; he crouched and could see its underside. A small

camera on the headset was reading the fiducial markers on the (real)

wall and using that spatial information to track his position among the

(virtual) cubes. So far, so good; no motion sickness yet....MORE

The "uncanny valley" usually applies to human

aesthetics. It describes that vague sense of revulsion you get when you

see a fabricated person—a robot, usually—who looks aaaaalmost human …

but not quite. So, for example, this lady. This dude. Anything displayed here.

The "valley" refers to the emotional reactions humans have toward

anthropomorphized machines, when those reactions are charted: It's the

deep dip in comfort level we tend to experience, based on our finely

honed survival instincts, when we humans come face-to-quasi-face with

beings that are at once extremely like us and extremely not....MORE

Mary Meeker can synthesize trends, pinpoint interesting numbers and

research, and deliver hundreds of slides like nobody’s business. The

Kleiner Perkins partner presented her annual Internet trends report at

the inaugural Code Conference this week.

Falcone, whose Harbinger Capital hedge fund owns the bankrupt

LightSquared, a high-speed wireless start-up, is asking the Federal

Communications Commission to take “immediate” action to stem the barrels

of red ink flowing from the company.

In a letter to the FCC, Falcone is

urging the regulator to “mitigate further damage” to Harbinger, which

invested $3 billion in LightSquared only to see the agency pull the plug

on the company in 2012. On Wednesday, Falcone asked the FCC to take

“immediate, positive action” to reverse Harbinger’s losses, according to

the letter sent by his legal team. [NYP]

Humans have long wondered whether we are alone in the universe.

According to scientists working with the Search for Extraterrestrial

Intelligence (SETI) Institute, the question may be answered in the near

future.

"It's unproven whether there is any life beyond Earth," Seth Shostak, senior astronomer at the SETI Institute, said at a HouseCommittee on Science, Space and Technology hearing Wednesday (May 21). "I think that situation is going to change within everyone's lifetime in this room."...

Gold is at $1245.00, down $11.30 and down $46.70 for the week.

From Kitco:

Comex Gold Extends Slide On Technically Oriented Selling

U.S. gold futures are extending the losses from earlier this week

Friday largely on technically oriented selling, traders said.

As of 11:17 a.m. EDT, gold for August delivery

was $12.10, or 1%, lower to $1,245 per ounce on the Comex division of

the New York Mercantile Exchange. The contract bottomed at $1,243.70,

its weakest level since February. July silver was down 24.9 cents, or 1.3%, to $18.765 an ounce.

“It’s technical more than anything else,” said Charles Nedoss, senior market strategist at LaSalle Futures Group.

The market dipped below the roughly

$1,250-an-ounce level that was offering support after prior weakness

this week. “You picked up some (sell) stops there,” Nedoss said. These

are pre-placed orders activated when certain chart points are hit,

either to book profits, exit a losing position or establish a fresh one....MORE

While both of the "Money" metals are looking weak, silver in particular is interesting as it goes through what had been support:

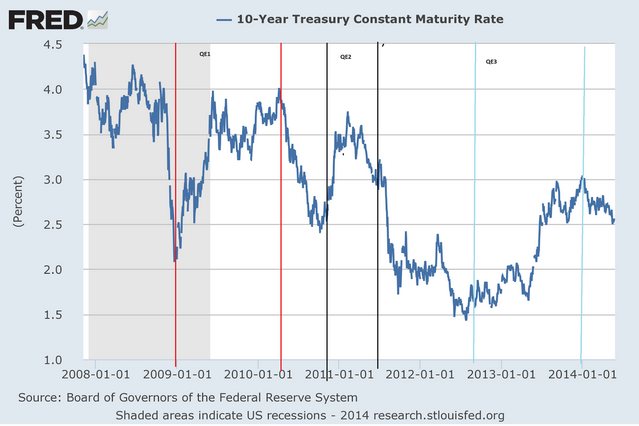

A lot of people are puzzled over why US yields are falling when nothing has changed on the Fed communication side, and QE is supposed to be slowing.

Frances Coppola notes

an even stranger phenomenon. When you look at the very big picture you

realise that if there is a correlation between QE and rates, it’s

actually a very counterintuitive one:

Every time QE is announced, yields rise: when it ends,

they fall. And no, this doesn’t just affect the 10-year yield. The same

basic shape can be observed on just about any maturity over 1 year

(short-term rates are propped up by the positive IOER policy).

It’s counterintuitive because people tend to believe that QE

suppresses rates by creating a bid where there otherwise wouldn’t be

one.

The standing theory, consequently, is that a QE exit should encourage rising yields....MUCH MORE

Who can forget where they were when they first saw this:

From IEEE Spectrum:

So, Where Are My Robot Servants?

Tomorrow’s robots will become true helpers and companions in people’s homes—and here’s what it will take to develop them

Four years ago, researchers at the University of California, Berkeley, uploaded a video to YouTube. It featured a demonstration they’d done using a powerful new robot called PR2,

a dishwasher-size machine with two hefty arms and six camera eyes on

its face. In the demo, PR2 stands before a disorderly pile of small

towels. Then, slowly but surely, it stretches its arms, picks up a

towel, and neatly folds it, even patting it gently to smooth out the

wrinkles. The robot repeats the routine until no more towels are left in

the heap.

The researchers

were pleased with their work, but they didn’t quite expect what came

next: Their video went viral. Within days, hundreds of thousands of

people watched it as news of the robot spread through social media and

the blogosphere. Reports popped up on newscasts and publications around the world. One Twitter user humorously summed up what the achievement might portend: “I, for one, welcome our towel-folding robot overlords.”

This robotic laundry experiment had obviously struck a nerve. The idea of robots doing choresaround the house

has long captured people’s imaginations. For some, robots would mean

freedom from tasks they don’t have time for or don’t want to do. For

others, robots would mean even more: They would help them liveindependently longer, providing care and perhaps even some degree of companionship.

It’s disappointing, then, that other than robotic toys and vacuum cleaners,

robots are a rare sight in our homes today. And yet, here we are, still

eagerly waiting for this technology to blossom. So, where are the robot

servants?

Some recent developments suggest that they might not be too far away.

Processors, sensors, and other components that robots need have gotten

much better and cheaper, propelled by advances in smartphone technology....MORE

The science of inequality What the numbers tell us

In 2011, the wrath of the 99% kindled

Occupy movements around the world. The protests petered out, but in

their wake an international

conversation about inequality has arisen, with tens

of thousands of speeches, articles, and blogs engaging everyone from

President

Barack Obama on down. Ideology and emotion drive

much of the debate. But increasingly, the discussion is sustained by a

tide

of new data on the gulf between rich and poor.

This special issue uses these fresh waves of data to explore the origins, impact, and future of inequality around the world.

Archaeological and ethnographic data are revealing how inequality got its start in our ancestors (see pp. 822 and 824). New surveys of emerging economies offer more reliable estimates of people's incomes and how they change as countries develop

(see p. 832).

And in the past decade in developed capitalist nations, intensive

effort and interdisciplinary collaborations have produced

large data sets, including the compilation of a

century of income data and two centuries of wealth data into the World

Top

Incomes Database (WTID) (see p. 826 and Piketty and Saez, p. 838).

It is only a slight exaggeration to liken

the potential usefulness of this and other big data sets to the enormous

benefits

of the Human Genome Project. Researchers now have

larger sample sizes and more parameters to work with, and they are also

better able to detect patterns in the flood of

data. Collecting data, organizing it, developing methods of analysis,

extracting

causal inferences, formulating hypotheses—all of

this is the stuff of science and is more possible with economic data

than

ever before. Even physicists have jumped into the

game, arguing that physical laws may help explain why inequality seems

so

intractable (see p. 828)....MORE

This whole thing could have been avoided with a little peer review but no; Piketty had to write a book and commenters had to comment without the least bit of effort beyond turning the pages.

I swear economists have to be the most worthless, most self-absorbed bunch of scamsters one is likely to run into.

So there I was, gathering my thoughts, such as the above, for the 700K word comment when Chris Giles drops out of one of the feedreaders.

From Money Supply:

Capital in the 21st Century – a response

Professor Thomas Piketty has given a more detailed response to the Financial Times articles and blogs on his wealth inequality data in Capital in the 21st Century (here, here, here and here). He says it is “simply wrong” to suggest he made errors in his data.

There are a few things on which we agree. First, the source data on

wealth inequality is poor. I have written that it is “sketchy” and Prof

Piketty says it is “much less systematic than we have for income

inequality”. Second, it would have been preferable for Prof Piketty to

have used a more sophisticated averaging technique than a simple average

of Britain, France and Sweden to derive an estimate for European wealth

inequality. Third, the available data suggests a broad trend of

reduction in wealth inequality during most of the 20th Century.

There are more aspects on which there remains disagreement. Prof

Piketty does not explain the multiple missing data points in his data or

tweaks to it; he explains transcription errors as deliberate

adjustments to overcome discontinuities in data, but does not provide

formulas or an explanation of why these undocumented adjustments should

apply to only one data point in a time series; he does not explain why

it is consistent to favour household surveys over estate tax records for

the US but not the UK; nor why his UK series showing rising wealth

inequality differs so materially from his source materials, which show falling UK wealth inequality in eight of the most recent nine decades....MORE

In the News: Russian natural gas pipeline exports to Western Europe grow 20%

In 2013, Russia exported an average of 15.6 billion cubic feet

per day (Bcf/d) of natural gas on pipelines to countries in Eastern and

Western Europe, 16% more than in 2012, according to data from the U.S.

Energy Information Administration, Eastern Bloc Research, and Russian

Energy Monthly. Russia's natural gas pipeline exports to Western Europe

drove most of this increase, rising by 20%, to 12.3 Bcf/d.

The entire increase in Russian natural gas exports to Western Europe

in 2013 occurred in three countries – Italy, Germany, and the United

Kingdom:

Italy had the largest increase in natural gas pipeline imports from

Russia in 2013, receiving 2.4 Bcf/d of natural gas. This reflected a 1.0

Bcf/d increase over 2012. Italy accounted for 16% of total Russian

natural gas pipeline exports to Eastern and Western Europe in 2013,

versus 11% in 2012. Italy can receive Russian natural gas on the

Bratstvo (Brotherhood) and Soyuz (Union) pipelines, which pass through

Ukraine.

Germany saw its natural gas pipeline imports from Russia increase in

2013 to 3.9 Bcf/d. This was 0.7 Bcf/d over 2012 levels. Germany can

receive Russian gas on the same pipelines as Italy, as well as the

Yamal-Europe and Northern Lights pipelines. However, most of Germany's

Russian gas imports now flow via the Nord Stream pipeline, which

bypasses transit states, such as Ukraine and Poland, and brings gas

directly from Russia via the Baltic Sea.

The United Kingdom's natural gas pipeline imports from Russia

increased to 1.2 Bcf/d in 2013, 0.4 Bcf/d more than in 2012. The United

Kingdom mainly imports natural gas from Russia via the Nord Stream

pipeline, along with other interconnecting pipelines.

Currently, Russia's entire natural gas pipeline exports flow to

Europe, with the exception of small volumes to Armenia, in Eurasia....MUCH MORE

In The Capitalist’s Dilemma, Clayton

Christensen and Derek van Bever introduce a powerful new theory which

explains the relative paucity of growth in developed economies. They

draw a causal relationship between the mis-application of capital in

pursuit of innovation and the failure to grow.[1]

In particular, they observe that capital is allocated toward the type

of innovations which increase efficiency or performance and not toward

those which create markets (and hence long term growth and jobs.) This

itself is caused by a prioritization and rewarding of performance ratios

rather than cash flows and that itself is due to a perversion of the

purpose of the firm.[2]

For this statement of causality to be confirmed we need to observe

whether it predicts measurable phenomena. For instance, we need to see

whether companies which create markets apply capital toward

market-creating innovations and whether companies which create value

through efficiencies or performance improvements hoard abundant capital.

Over the entire global economy, the pattern of capital over-abundance is easy to see. The amount of cash or securities on balance sheets is extraordinary and unprecedented (estimated at $7 Trillion, doubling over a decade). However, growing cash is not a perfect indicator of inactivity. Cash is the by-product of earnings after

investment. So if operating profits are growing and investment is

growing, but not as fast, then it’s possible to grow cash while still

growing investment.

The better measure is investment in capital equipment or, more specifically, purchases of plant, property and equipment.[3] Indeed, on a global scale, capital expenditure as a percent of sales is at a 22-year low.

CapEx is a good proxy for non-financial “investment”. It’s also a

measure that can be easily obtained as companies report this activity in

their Cash Flow Statements....MORE

A new paper via the Social Science Research Network:

Abstract:

We investigate the relationship between value, growth

and momentum investment styles across a wide range of developed and

emerging economy equity markets. As would be anticipated, value

investing generally beats growth. We then determine whether the

application of relative momentum or trend following filters can enhance

the risk-adjusted performance for either value or growth investors. We

find that both value and growth portfolios benefit from momentum filters

but particularly the latter, though the application of such a filter

still leaves investors with return volatility that is typical of equity

markets along with negative skewness and with high maximum drawdowns.

However, our results show that the use of a simple trend following

filter typically delivers a much more favourable investment performance

than relative momentum with considerably lower volatility and smaller

drawdowns. Furthermore, the application of a simple trend following

filter either on its own or in combination with a relative momentum

filter, not only reduces the performance advantage of value over growth

investing but actually reverses this advantage.

The family and followers of one of India’s wealthiest Hindu spiritual

leaders are fighting a legal battle over whether he is dead or simply

in a deep state of meditation.

His Holiness Shri Ashutosh Maharaj, the founder of the Divya Jyoti

Jagrati Sansthan religious order with a property estate worth an

estimated £100 million, died in January, according to his wife and son.

However, his disciples at his Ashram have refused to let the family

take his body for cremation because they claim he is still alive.

According to his followers, based in the Punjab city of Jalandhar, he

simply went into a deep Samadhi or meditation and they have frozen his

body to preserve it for when he wakes from it.

His body is currently contained in a commercial freezer at their Ashram....MORE

“Companies, especially financial institutions, will do almost anything

to avoid a tough enforcement action and therefore have a natural and

powerful incentive to make prosecutors believe that death or dire

consequences await,” he said. “I have heard assertions made with great

force and passion that if we take any criminal action, the skies will

darken; the oceans will rise; nuclear winter will be upon us; and the

world as we know it will end.”

-Preet Bharara,

U.S. Attorney for the Southern District of New York

The other day, while I was navigating Reddit I found an interesting post that was called The 10 Algorithms That Dominate Our World by the author George Dvorsky

which was trying to explain the importance that algorithms have in our

world today and which ones are the most important for our civilization.

Now if you have studied algorithms the first thing that could come to your mind while reading the article is “Does the author knows what an algorithm is?” or maybe “Facebook news feed is an algorithm?” because

if Facebook news feed is an algorithm then you could eventually

classify almost everything as an algorithm. So I’m going to try to

explain in this post what an algorithm is and which are the real 10 (or

maybe more ) algorithms that rule our world.

What is an algorithm?

Informally, an algorithm is any well-defined computational procedure that takes some value, or set of values, as input and produces some value, or set of values, as output. An algorithm is thus a sequence of computational steps that transform the input into the output. Source: Thomas H. Cormen, Chales E. Leiserson (2009), Introduction to Algorithms 3rd edition.

In

simple words is possible to say that an algorithm is a sequence of

steps which allow to solve a certain task ( Yes, no just computers use

algorithms also humans use them). Now, an algorithm should have three

important characteristics to be considered valid:

It should be finite: If your algorithm never ends trying to solve the problem it was designed to solve then it is useless

It should have well defined instructions: It has to be precisely defined each step of the algorithm; the instructions should be unambiguously specified for each case.

It should be effective: The

algorithm should solve the problem it was designed to solve. And it

should be possible to demonstrate that the algorithm converges with just

a paper and pencil.

Also is

important to say that algorithms are used in Computing Sciences but they

are a mathematical entity, in fact the first mathematical algorithms

that we have registry are from 1600 BC — Babylonians develop earliest known algorithms for factorization and finding square roots.

So here we have the first problem with the post mentioned before, it

treats algorithms as computing entities, but if you take the formal

meaning of the word the real top 10 algorithms that rule the world can

be found in a book of arithmetic (addition, subtraction, product, etc).

But

lets take computing algorithms as our definition of algorithm in this

post, so the question remains: Which are the 10 algorithms that rule the

world?. Here a put a little list of which are this algorithms in no

particular order.

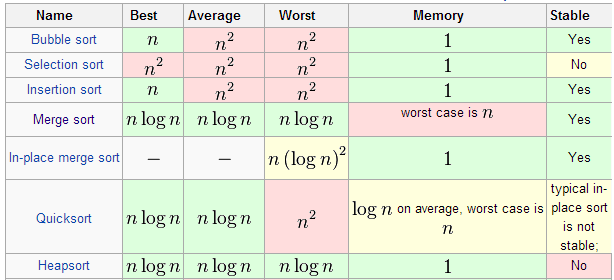

What

is the best algorithm to sort elements? It depends in what you need and

that’s why I put the three more used sort algorithms in the same place,

maybe you have a preference in one of them but all of them are equal

important.

The Merge Sort algorithm

is by far one of the most important algorithms that we have today. It is

a comparison-base sorting algorithm that uses the approach divide and

conquer to solve a problem that once was a O(n^2). It was invented by

the mathematician Jhon von Neumann in 1945.

Quick

Sort is a different approach to the sorting problem, it can use

in-place partition algorithms and is a divide and conquer algorithm too.

The problem with this algorithm is that is not a stable sort but is

really efficient for sorting RAM-based arrays.

Finally,

Heap Sort algorithm uses a priority queue that reduces the search time

in the data. This algorithm is also an in-place algorithm and is not

stable sort.

These algorithms are a

big improvement over other approaches used like bubble sort, in fact is

thanks to them that today we have Data mining, artificial intelligence,

link analysis and most of the computing tools in the world including the

web.

2. Fourier Transform and Fast Fourier Transform

Our

entire digital world uses these simple but really powerful algorithms

that transform signals from their time domain into their frequency

domain and viceversa. In fact, you are seen this post thanks to these

algorithms.

The internet, your WiFi,

smartphone, phone, computer, router, satellites, almost everything that

has a computer inside use this algorithm to work, in one way or another.

You can’t study a degree in electronics, computing or

telecommunications without studying these important algorithms.

3. Dijkstra’s algorithm

Is

not crazy to say that the internet wouldn't work as efficient as it

does if it wasn't because of this algorithm. This graph search algorithm

is used in different applications where the problem can be modeled as a

graph and you have to find the shortest path between two nodes.

Even

when today we have better solutions for the problem of finding the

shortest path, Dijkstra’s algorithm is still used in systems that

require stability....MORE

Uber will eventually replace the people who drive its cars with cars

that drive themselves, CEO Travis Kalanick said today at the Code

Conference. A day after Google unveiled the prototype

for its own driverless vehicle, Kalanick was visibly excited at the

prospect of developing a fleet of driverless vehicles, which he said

would make car ownership rare. "The reason Uber could be expensive is

because you're not just paying for the car — you're paying for the other

dude in the car," Kalanick said. "When there's no other dude in the

car, the cost of taking an Uber anywhere becomes cheaper than owning a

vehicle. So the magic there is, you basically bring the cost below the

cost of ownership for everybody, and then car ownership goes away."...MORE

The stock is at $21.18, up $1.71. For the last couple years the money has definitely not been in the module or polysilicon makers but rather in the installers and financiers, especially the latter, links after the jump.

From MarketWatch:

SunEdison Inc. rallied Thursday following news its “yieldco” subsidiary has filed for an initial public offering.

TerraForm Power will own and operate clean-power plants and other assets acquired from SunEdison SUNE+8.65%

and other companies, SunEdison said.

Goldman Sachs and Barclays are the joint bookrunners, and price and number of shares have not been decided yet, it added.

SunEdison is following on the footsteps of giant NRG Energy Inc., which

last year launched NRG Yield Inc., bundling solar and natural gas

power-generation assets and raising nearly $500 million in capital in

July.

Shares of Missouri-based SunEdison rose 9.4%.

Several solar companies are looking into bundling existing solar-power

plants and projects into subsidiaries, known in the industry as

“yieldcos.”

Revenues would flow from long-term, predictable power purchase

agreements with utilities, and shares of the yieldcos would trade in

stock exchanges just like any stock, providing liquidity and

transparency....MORE

Finally

for investors in rent-seeking organizations there is the real risk that

the politicians will change the rules. Heed the words of Sen. Simon

Cameron (R&D!-Pa.):

Our Hero

"The honest politician is one who when he is bought,

Putin forms ex-Soviet trade bloc to challenge EU, US

Astana, Kazakhstan—Russian President Vladimir Putin Thursday signed a

treaty with his counterparts from Kazakhstan and Belarus creating a

trading bloc of more than 170 million people to challenge the United

States and European Union.

The formal creation of the Eurasian Economic Union in the Kazakh

capital of Astana marks the culmination of two decades of talks between

former Soviet republics.

Kyrgyzstan and Armenia are seeking to join the union by the end of the

year, the countries’ leaders said at the signing ceremony today.

Putin, facing sanctions from the US and EU for his annexation of

Crimea from Ukraine, said the three countries will “gradually align”

their currency and monetary policies to facilitate trade and minimize

risks. The Russian leader has pushed for Ukrainian membership in the

union and, before relations soured with the EU, urged the creation of a

free-trade zone from Lisbon to Vladivostok on the Pacific Ocean.

“The Eurasian Union is a realization of Putin’s geopolitical dream,”

said Nikolay Petrov, a scholar at the Carnegie Moscow Center research

group. “The Eurasian Union is a demonstration that Russia is not alone.”...MORE

No word on what this means for Kazakhstan's "Don't call me Stan" name change.

We had estimates coming in at 107-111 bcf but as always it's the second derivative that matters: not the actual number and not what the other guy thinks the number will be but how Guy the second reacts to what he thinks Guy the first is thinking.

Front futures $4.594 down 2.1 cents.

The headline at Natural Gas Intelligence is:

Bears Barely Moving Following Stout EIA Storage Report

Natural gas futures dropped Thursday morning following the release of

government storage figures that were somewhat on the high side of what

traders were expecting.

The injection report of 114 Bcf was about 4 Bcf higher than market

surveys and independent analyst projections. For the week ended May 23,

the Energy Information Administration (EIA) reported an increase of 114

Bcf in its 10:30 a.m. EDT report. July futures fell to a low of $4.529

shortly after the number was released but by 10:45 a.m. July was at

$4.587, down 2.8 cents from Wednesday's settlement.

Prior to the release of the data, analysts were looking for a build

just above 110 Bcf. A Reuters survey of 24 traders and analysts revealed

an increase of 110 Bcf with a range of 100 Bcf to 115 Bcf. United ICAP

forecast a build of 113 Bcf and Bentek Energy's flow model anticipated

an injection of 111 Bcf.

A New York floor trader remarked that with the reaction to the storage

report "nothing has really changed. We are still in the range of $4.25

to $4.75. It's not an 'a-ha' moment. It was not a significant

development."...MORE

From the Energy Information Administration:

....Summary

Working gas in storage was 1,380 Bcf as of Friday, May 23, 2014,

according to EIA estimates.

This represents a net increase of 114 Bcf from the previous week.

Stocks were 748 Bcf less than last year at this time and 922 Bcf below

the 5-year average of 2,302 Bcf.

In the East Region, stocks were 438 Bcf below the 5-year average

following net injections of 64 Bcf.

Stocks in the Producing Region were 374 Bcf below the 5-year average of

918 Bcf after a net injection of 31 Bcf.

Stocks in the West Region were 110 Bcf below the 5-year average after a

net addition of 19 Bcf.

At 1,380 Bcf, total working gas is below the 5-year historical range...MORE

This is earlier in the cycle than expected. I mentioned the transmutations that small companies can go through back in 2008's "Chameleons on the Pink Sheets":

...A classic history

would be a Vancouver "junior resource" company in 1979, after the

collapse of the oil and gold markets became a solar deal in '81 , an

Aloe Vera deal to the yuppies mid '80's, a biotech in '86 ("we're the

next Amgen"or "A cure for AIDS"), then on to neutraceuticals or spas,

Indian casinos, software, then the great "i", "e-" and ".com" gold

rush. Someday I'll get around to checking if some lunatic scammer

actually went with "e-iTrade.com".

The next group of parasites were the "homeland security" companies,

then land deals. The "resource" scams never went away and became more

prominent in 2002 after gold had moved off its $252 bear market low. We're in the Green boom (happy Earth day by the way) now, who knows what's next....

From Kitco:

With the mining sector proving to be ruthless in the junior mining

space as a lack of capital in the industry continues, junior miners

turned their heads to new opportunities, including the lucrative medical

marijuana industry.

March saw several penny stocks jump as juniors essentially

told the market they were looking at possibilities with medical

marijuana.

The move was generally hiring consultants to explore the

possibility in the field. However, in Canada, mining companies would

have to go through the same steps as anyone to receive one of the few

medical marijuana producers’ licenses. Only 12 have been handed out to

date.

In a statement to Kitco News, Department of Health Canada said

“to become a licensed producer, all applicants must meet all of the

requirements of the new Marihuana for Medical Purposes Regulation,

including obtaining the proper personal security clearances, meeting

the physical security requirements for the cultivation and storage

areas, and submitting a completed licensed producer application."

Supreme Pharmaceuticals (TSX:CL), formerly metals mining company Supreme Resources, has applied to Health Canada for a “Marihuana for Medical Purposes Regulations” (MMRP) license.

The company recently completed the acquisition of a greenhouse

complex for medical marijuana production on May 23, and said they will

be able to begin production upon receipt of an MMRP license.

Satori Resources Inc. (TSXV:BUD) recently completed a strategic alliance with Jourdan Resources Inc. (TSXV:JOR)

involving the Picnic Phosphate property in Quebec, which is focused on

phosphate minerals for specialized agriculture and fertilizer....MORE

For most Londoners, the most common view they enjoy as they trudge to

work is the back of another commuter's head but now, thanks to the

Streetmuseum app, anyone traipsing through the capital's streets can

step back in time to see what London looked like in the 19th and 20th

century compared with today - all in the same image.

The pictures below are part of a series in which historic and

contemporary images are blended together, allowing users to see just how

much London's streets have been transformed.

An exterior shot of the completed Gloucester Road Station in 1868 and 2014. (Photo by Museum of London/Streetmuseum app)

A street seller

of sherbert and water on the streets of London in 1893 and the same

street in 2014. (Photo by Museum of London/Streetmuseum app)

The view north up

Brick Lane in Spitalfields, close to the markets in 1957 and 2014.

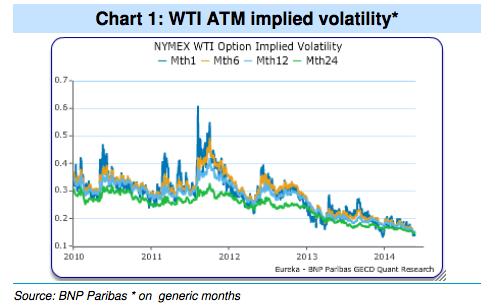

From Harry Tchilinguirian’s team at BNP Paribas, this is apparently what the death of volatility looks like:

And here’s the explainer:

More than mid-way through the second quarter, the oil

market has indeed been mostly range-bound. And despite geopolitical

flare-ups in Ukraine or Libya, implied oil volatility, be it on WTI or

Brent, has moved lower still from the time of our recommendation. As

volatility fell over the recent months, many in the market

initiated long volatility positions in the hope of mean reversion

higher, only to suffer from the cost of carry associated with time

decay, while volatility itself continued to erode.

We haven't linked to Cramer in so long I'd forgotten about him.

On the topic of oil prices we're thinking down then up but we've been thinking that for a year. From our March 29, 2014 post: Barron's Cover: "Here Comes $75 Oil"

There is a lot of the stuff sloshing around.

Throw in the geopolitical angles (US/EU v. Russia; Saudia v. Persia) and a bit of downside protection may be in order.

Plus, we've been calling for it since $106-107, seven months ago and frankly I'm getting tired of the répétition, know what I'm sayin'?

Apparently contradicting the 'sloshing around' statement is the forward

curve for WTI, currently in pretty steep backwardation from May 2014 at

$101.67 to June 2016 at $84.73. That's a simplistic view however and

does not account for above ground oil entangled in financing deals (Hi

Izzy) and in situ storage. Remember July 4, 2008?

Oil began its historic decline from the previous day's all time high with the curve backwardated....

From CNBC:

The strength in oil prices may not be terribly long-lasting.

That's the broad takeaway from technical analysis provided by Carley Garner, author of "A Trader's First Book on Commodities."

Although Jim Cramer is first and foremost a

fundamental investor, he often turns to technical analysis for insights,

especially when an analyst has an impressive track record.

And Cramer says few analysts have been more

accurate than Garner. "So, when Garner says to be cautious about crude, I

take her seriously."

We have looked at the problem quite a few times especially from the natural gas angle and are pretty sure we will see $8.00 gas before we see $2.00 gas. For oil we are thinking down then up but WTI in particular has been quite stubborn about staying in a $90-$110 trading range.

From Bloomberg:

The U.S. shale patch is facing a

shakeout as drillers struggle to keep pace with the relentless

spending needed to get oil and gas out of the ground.

Shale debt has almost doubled over the last four years

while revenue has gained just 5.6 percent, according to a

Bloomberg News analysis of 61 shale drillers. A dozen of those

wildcatters are spending at least 10 percent of their sales on

interest compared with Exxon Mobil Corp.’s 0.1 percent.

“The list of companies that are financially stressed is

considerable,” said Benjamin Dell, managing partner of

Kimmeridge Energy, a New York-based alternative asset manager

focused on energy. “Not everyone is going to survive. We’ve

seen it before.”

Some investors are already bailing out. On May 23, Loews

Corp. (L), the holding company run by New York’s Tisch family, said

it is weighing the sale of HighMount Exploration & Production

LLC, its oil and natural gas subsidiary, at a loss.

HighMount lost $20 million in the first three months of the

year, after being unprofitable in 2013 and 2012, Loews said it

its financial reports. As with much of the industry, HighMount

has shifted its focus to oil after natural gas prices plunged

and has struggled to find sites worth developing, company

records show.

Mary Skafidas, a spokeswoman for Loews, declined comment.

Production Declines

Quicksilver acknowledges the company is over-leveraged,

said David Erdman, a spokesman for Quicksilver. The company’s

interest expense equaled almost 45 percent of revenue in the

first quarter. “We have taken concrete measures to reduce

debt,” he said.

Drillers are caught in a bind. They must keep borrowing to

pay for exploration needed to offset the steep production

declines typical of shale wells. At the same time, investors

have been pushing companies to cut back. Spending tumbled at 26

of the 61 firms examined. For companies that can’t afford to

keep drilling, less oil coming out means less money coming in,

accelerating the financial tailspin.

Interest Expenses

“Interest expenses are rising,” said Virendra Chauhan, an

oil analyst with Energy Aspects in London. “The risk for shale

producers is that because of the production decline rates, you

constantly have elevated capital expenditures.”

Chauhan wrote a report last year titled “The Other Tale of

Shale” that showed interest expenses are gobbling up a growing

share of revenue at 35 companies he studied. Interest expense

for the 61 companies examined by Bloomberg totalled almost $2

billion in the first quarter, 4.1 percent of revenue, up from

2.3 percent four years ago.

The drilling spree boosted U.S. oil production to 8.4

million barrels a day, 16 percent more than a year ago and the

highest since 1986. Growth has been driven by advances in

horizontal drilling and hydraulic fracturing, or fracking, which

unlocked crude and natural gas trapped in formations like North

Dakota’s Bakken shale or the Marcellus in the U.S. northeast....MORE

This is an extreme view, probably promulgated to sell a book, but it highlights the problem with decline rates.

There are some plays which are uneconomic over the life of the well

(more money in than out) but which are drilled anyway because of the

quick cash flow which can be used as the basis for another round of debt

or equity.

Stripped of all the hype, there are E&P companies that are basically

Ponzi schemes but with a tail long enough that the miscreants will

probably get away with it....

We are still in a bull market and markets being perverse we'll probably have a summer rally that drives the Sell in May folks insane. Their prayers for a correction to scale back in on go unanswered and in their madness to participate they put in the top.

Or something.

From Pension Partners:

Back in Time

Are you telling me that you built a time machine… out of a DeLorean?

Of course not. It’s 2014 and the environmentalists would go crazy. We built one out of a Tesla Model S and we’re headed back to…

May 2007. The economy is humming along and we’re over five years into

an expansion that began in late 2001. The S&P 500 is hitting new

bull market highs almost daily and investors are looking forward to a

fifth consecutive year of gains. The credit markets are booming, with

record demand for risky debt and high yield spreads hitting new lows.

There is some evidence of weakness in the housing market but this is

surely a healthy development considering the incredible advance over the

previous few years.

Given this backdrop, Investors are broadly optimistic, with Bulls

outnumbering Bears in the Investors Intelligence poll by over 2.5 to 1.

Also key to this bullishness is the new “low volatility regime,” with

the VIX trading between 12 and 14 after crossing below 10 briefly in

January and February. As long as volatility is low, Hedge Funds seem

more than happy to increase leverage and net exposure to “boost

returns,” creating a strong underlying bid beneath the market.

S&P 500, May 2007: What’s not to like?

While on the surface all is well in the markets, there is a subtle

rotation going on underneath. Energy and Materials are the leading

cyclical sectors while Consumer Discretionary and Financials are the

weakest sectors. Together, this backdrop is classic late cycle behavior

and not typically what you see in a strong economy....

"The parallels between May 2007 and May 2014 are unmistakable, with

broad market strength masking underlying weakness," according to the

post. "That is not to say what happens next will play out in the same

fashion this time around as it most certainly will not. But at the same

time, to completely ignore what the market is telling us here would be

foolish as well."

{kind=link}