The best performing stock in the

S&P 500 this year isn’t Google or Nvidia or Domino’s, but AMD—a

chipmaker that’s recently changed its strategy to chipping away Intel’s

data-center revenue.

The company,

founded in Silicon Valley in 1969, has historically played the role of

lagging competitor rather than star of its own show—it’s been

overshadowed by Intel’s dominance in the central processing unit (CPUs) market and Nvidia’s meteoric rise on the back of demand for its graphics processing units (GPUs).

But now AMD’s stock growth is outperforming both its major competitors,

thanks to strong earnings reports and new products meant for commercial

data centers. The stock has risen about 120% in 2018, compared to

Nvidia’s 28% growth and Intel’s loss in stock value since the unvalorous exit of CEO Brian Krzanich.

Its most recent bright spot was the launch of its new Radeon server

card, which makes it easier to run virtual PCs at the same time on data

centers....MORE

A link in this morning's Further Reading post at FT Alphaville, "Current accounts and retained earnings" from the Swiss National Bank reminded me of this piece which fell out of one of the feedreaders on Wednesday.

And before moving on, thanks to FTAV for the Climateer linkage.

From the Council on Foreign Relations, August 29:

Almost all oil-importing emerging economies with current account deficits are under market pressure to adjust ...

The question is a bit rhetorical.

Some other advanced economies still are running current account

deficits. And I don’t think China is really in current account deficit,

and if it was, I personally don’t think a small deficit would pose any

real problem. China in theory could fund a modest deficit with the

interest income on its still substantial reserves ...

But there is no doubt that almost all the oil-importing emerging

economies that ran external deficits last year are facing pressure to

adjust.

All have seen their currencies fall significantly this year.

I don’t expect Turkey’s troubles will prove

contagious in the same way as Asia in 1997— India and Brazil have

substantial reserves, and thus there is no real risk that a weaker

currency will cause them trouble in repaying their external debt. South

Africa and Indonesia don’t have access to comparable reserve stockpiles,

but they are doing the right thing by letting their currencies adjust.

Turkey and Argentina really did stand out as the two emerging economies

with the most obvious vulnerabilities going into 2017—they had the

largest current account deficits going into 2018, and insufficient

reserves on standard debt-based metrics. The others are in a stronger

position to manage the crisis through currency adjustment alone, without

needing to borrow reserves to avoid a sovereign or bank default.*

But that doesn’t mean the pressure on

oil-importers to adjust—meaning tighten policies, slow growth, and look

more to exports to reduce their current account deficits—won’t have a

global effect.

No deficits in oil-importing emerging economies and a higher surplus

among the oil-exporters (who generally adjusted their imports down after

the 2014 oil price shock and now “break-even” with prices in the 50s) means, mechanically, that there need to be adjustments elsewhere....

but not getting a lot of enthusiasm from the industry. It might have

something to do with 90-year old marketing materials. Maybe update the

pics:...

Et voilà, Hellenic Shipping News, August 31:

Testing Begins On First Product Tanker Vessel Utilising Wind Propulsion Technology

Norsepower Oy Ltd., together with project partners Maersk Tankers,

Energy Technologies Institute (ETI) and Shell Shipping & Maritime,

today announced the installation of two Norsepower Rotor Sails onboard

Maersk Pelican, a Maersk Tankers Long Range 2 (LR2) product tanker

vessel.

The Rotor Sails are large, cylindrical mechanical sails that spin to

create a pressure differential – called the Magnus effect – that propels

the vessel forward. The Rotor Sails will provide auxiliary wind

propulsion to the vessel, optimising fuel efficiency by reducing fuel

consumption and associated emissions by an expected 7-10% on typical

global shipping routes.

Two 30×5 metres Norsepower Rotor Sail successfully installed onboard the Maersk Pelican.

The Rotor Sails are the world’s largest at 30 metres tall by five

metres in diameter and were installed on the product tanker vessel in

the port of Rotterdam. The first voyage with the Rotor Sails installed

will commence shortly.

“This project is breaking ground in the product tanker industry.

While the industry has gone through decades of technological

development, the use of wind propulsion technology onboard a product

tanker vessel could take us to a new playing field. This new technology

has the potential to help the industry be more cost-competitive as it

moves cargoes around the world for customers and to reduce the

environmental impact,” said Tommy Thomassen, Chief Technical Officer,

Maersk Tankers.

The Rotor Sails have completed rigorous land testing, including

thorough testing of various mechanical and performance criteria, and is

the first Rotor Sails to be Class approved for use on a product tanker

vessel. Extensive measurement and evaluation of the effectiveness of the

Rotor Sails will now take place to test the long-term financial and

technical viability of the technology. Independent experts from Lloyd’s

Register’s (LR’s) Ship Performance team will acquire and analyse the

performance data during the test phase to ensure an impartial assessment

before technical and operational insights as well as performance

studies are published.

Andrew Scott, Programme Manager HDV marine and offshore renewable

energy, ETI explained: “We commissioned this project to provide a unique

opportunity to demonstrate the untapped potential of Rotor Sails.

Auxiliary wind propulsion is one of the few fuel-saving technologies

that is expected to offer double-digit percentage improvements. The

technology is projected to be particularly suitable for tankers and dry

bulk carriers, and this test will assist in determining the further

potential for Rotor Sails in the product tanker industry.”

Tuomas Riski, CEO, Norsepower, added: “We have great ambitions for

our technology and its role in decarbonising the shipping industry. The

installation of our largest ever Rotor Sails in partnership with these

industry leading organisations shows that there is an appetite to apply

new technologies.

“With this installation on the Maersk Pelican, there are now three

vessels in daily commercial operation using Norsepower’s Rotor Sails.

Each of these cases represents a very different vessel type and

operational profile, demonstrating the widespread opportunity to harness

the wind through Flettner rotors across the maritime industry.”...MORE

Google's next big thing will likely come from

one of its new priority areas, like cloud, transportation, and

healthcare. Each has a massive, global addressable market and plays well

to Google's strength in AI.

As the digital world evolves, Google is taking a multi-pronged

approach to maintaining its dominance in the search and ad business,

which makes up the vast majority of its revenue.

Search is migrating across mediums, with users gradually moving from

desktop to mobile devices and voice assistants — a shift that directly

threatens Google’s moat in search and advertising.

As competition rises in the mobile and digital assistant space, and

concerns over privacy and data management mount, Google has been forced

to adapt.

To maintain its foothold and protect its main source of revenue,

Alphabet (Google’s parent company) is positioning itself to dominate

adjacent sectors — such as digital commerce, branded hardware products,

and content — and attempting to integrate its services into every aspect

of the digital user experience.

The company is also seeking out new streams of revenue in sectors

with large addressable markets, namely on the enterprise side with cloud

computing and services. Furthermore, it’s looking at industries ripe

for disruption, such as transportation, logistics, and healthcare.

Unifying Alphabet’s approach across initiatives is its expertise in

AI and machine learning, which the company believes will help it become

an all-encompassing service for both consumers and enterprises.

In this teardown, we dive into Google’s approach to maintaining its

search platform dominance, outlining the strategic investments,

acquisitions, and partnerships across its top priorities moving forward.

Alphabet’s structure and background

Alphabet is broken out into its core Google business and a number of other subsidiaries, which it deems “Other Bets.”

The majority of Google’s business comes from advertising revenues,

which the company generates through its search engine as well as a

number of other Google-affiliated and partnership websites.

Outside of search and advertising, Google generates revenue from

products including cloud and enterprise, consumer hardware, mapping, and

YouTube.

In addition to Google, Alphabet encompasses a host of other

subsidiaries called “Other Bets.” These companies are more experimental

in nature, and as a result are not material to Alphabet’s bottom line.

Google’s Other Bets include:

GV and capitalG, two of Google’s investment vehicles

Waymo, Google’s self-driving car initiative

Verily and Calico, two healthcare subsidiaries

Alphabet Access & Energy, which houses the company’s telecommunications projects and energy initiatives

DeepMind, an AI research arm acquired by Google in 2014 that has the company develop neural networks

Cybersecurity spinoff Chronicle, which focuses on security solutions for Google’s cloud business

Project Loon, a subsidiary working to bring internet access to rural and remote areas

Project Wing, which is developing an autonomous delivery drone service

Google X, an R&D facility focused on “moonshot” technologies aimed at improving the world

Given that Google makes up the vast majority of Alphabet’s business,

the company’s initiatives across subsidiaries have largely focused on

protecting Google’s moat in search and advertising.

In recent quarters, the company has seen notable increases in traffic

acquisition costs (TAC), which is the largest cost associated with

Google’s main stream of revenue, ad and search. As the company faces

increasing regulation (e.g. the EU’s $5B fine on Android) and an ongoing

shift to mobile from desktop, TAC is expected to rise.

In addition to rising TAC, competition is growing from peers like

Apple, Amazon, and Microsoft, all of which are racing to capitalize on a

growing digital economy to capture data and access new streams of

revenue.

As a result, Google is doing everything in its power to capitalize on

potential growth areas and maintain its foothold in search and

advertising.

Below, we outline the company’s main priorities, detailing the

initiatives, investments, and acquisitions across its subsidiaries.

1. Embrace an AI-centric approach and solidify lead in machine learning

Artificial intelligence is critical to Alphabet’s long-term

outlook. AI is the thread that runs through search & advertising,

cloud, autonomous driving, healthcare, and a host of the company’s Other

Bets, as we’ll outline futher below.

WHAT it’s DOING now

In a keynote presentation to launch Google’s new high-end Pixel

smartphones in October 2016, CEO Sundar Pichai highlighted the

importance of artificial intelligence to the tech landscape moving

forward, explaining, “It is clear to me we are evolving from a

mobile-first to an AI-first world.”

Since then, AI has become the company’s focus across its investments, acquisitions, and internal spending.

Investments

Google has launched two funds dedicated solely to AI: Gradient Ventures and the Google Assistant Investment Program.

Gradient Ventures was launched in July 2017. Unlike GV and capitalG,

which run separately from Google under the Alphabet corporate framework,

Gradient Ventures is accounted for on Google’s balance sheet. That

said, the fund plans to break off from the main company once it ramps up

its investment pace.

So far, Gradient has only invested in early-stage deals, primarily

focusing on the US — though a recent investment was in Canada-based

Benchsci, a medical sciences startup using AI to accelerate biomedical

discoveries.

Google has also launched a fund to build out its capabilities for Google

Assistant, Google’s virtual assistant that uses natural language

processing to take voice commands from users and search the internet,

schedule events, set alarms, among a host of other tasks. Launched in

May, the Google Assistant Investment Program is focused specifically on

early-stage startups working with Google’s virtual assistant....

The 919 Evo is quite fast.

This is the second-to-last opportunity to see it following the Nürburgring in May and the Goodwood Festival of Speed in July.

From Ars Technica, June 30:

In May of this year, Porsche treated the fans at the 24 Hours Nürburgring

race to some exhibition laps by the 956

(which set the record in 1983)

and the 919 Evo.

Porsche shatters the Nürburgring record we thought was unbreakable

There must be something in the air. On Friday, we brought you news

about Romain Dumas and Volkswagen breaking records at the Pikes Peak

International Hill Climb. Just five days after Dumas' made it to the top

of the mountain, his colleagues at Porsche Motorsport—the team with

which he won Le Mans in 2016—have gone and shattered another record some thought would never be broken. The track is the 12.9-mile (20.8km) Nürburgring Nordschleife, and Porsche factory driver Timo Bernhard drove a Porsche 919 Evo around it in just 5:19.55.

35 years ago

Until now, the fastest man to ever lap the Nordschleife was the late

Stefan Bellof. By the time of his run in 1983, the track was considered

too dangerous for Formula 1, but little else had changed since the

1920s. Nordschleife was still workable for Group C though, which held

its 1983 1000kms of Nürburgring there. During qualifying for the race,

Bellof—driving a works Porsche 956—lapped the place in 6:11.13. (There's

no in-car footage of his run, but teammate Derek Bell did carry a camera for a practice lap that isn't that much slower.)

The 919 unleashed

After Porsche won Le Mans for the third time with the 919 Hybrid—bumping to 18 its total overall wins at the French race—the car maker decided to end the 919 Hybrid racing program. But instead of just sticking the race cars in the museum, Porsche decided to see how fast they could really go.

New engine management software and no need to abide by a fuel-flow

restriction bumped the 919's turbocharged V4 engine output from 500hp

(373kW) to 720hp (537kW). The hybrid system is 10-percent stronger at

440hp (328kW)....MORE

And from Brands Hatch:

Festival of Porsche

Brands Hatch (Indy)

Sunday 02 September 2018

Festival of Porsche returns to Brands

Hatch this September for a special celebration of Germany’s most iconic

sports car manufacturer, complete with racing, demonstrations and

displays.

The event’s return, for the first time since 2014, is ideally timed

as it coincides with the 70th anniversary of the founding of Porsche.

On-track action will be headlined by Porsche Club GB’s very own

Porsche Club Championship, starring a wide range of the manufacturer’s

race-prepared cars across a number of classes. The Porsche Classic

Restoracing Competition has launched this year to celebrate 20 years of

the Porsche Boxster. To celebrate this milestone, Porsche Centres across

the UK are sourcing and restoring 986 Boxster S models to race in a

dedicated championship, with a pair of twenty five minute races. There

will also be racing action from a selection of 4-Cyclinder Porsche cars,

together with a round of the Porsche Club Speed Championship.

Significant racing cars from the manufacturer’s past will appear too,

including the three-times Le Mans winning Porsche 919 Hybrid, taking to

the track for special demonstration runs on the Indy circuit. The last

Festival of Porsche featured appearances from Le Mans-winning Porsche

956s and 962s, and a whole host of other famous, mouth-watering Porsche

cars will be on display in the garages to view throughout the day - plus

some will be involved on-track for special demonstrations (click here

to view a list of cars that will be attending). In addition to the main

race day on the Sunday, Festival of Porsche’s activities will include a

Porsche Club member’s soiree on the Saturday night....MORE

*As Ars notes in their piece above:

...You can spot the Evo at Rennsport Reunion at Laguna Seca here in the US (September 27-30). That

last one should be special: we've been told by Porsche the aim is to

break the 1-minute barrier at the Californian circuit...

The following information about Imports and Exports is taken from London in 1731 by Don Manoel Gonzales. The full text is available from Project Gutenberg. The lists of traded items are taken verbatim from that document.

Country

Controlled by

Britain exports

Britain imports

Germany

Hamburg/German Merchants

broad-cloth, druggets, long-ells, serges, and several sorts of

stuffs, tobacco, sugar, ginger, East India goods, tin, lead, and several

other commodities

prodigious quantities of linen, linen-yarn, kid-skins, tin-plates, and a great many other commodities

Russia

Russia Company

coarse cloth, long- ells, worsted stuffs, tin, lead, tobacco, and a few other commodities

hemp, flax, linen cloth, linen yarn, Russia leather, tallow, furs, iron, potashes, etc., to an immense value

Norway and Denmark

Eastland Company

guineas, crown-pieces, bullion, a little tobacco, and a few coarse woollens

vast quantities of deal boards, timber, spars, and iron

Sweden

Eastland Company

gold and silver, and but a small quantity of the manufactures and production of England

near two-thirds of the iron wrought up or consumed in the kingdom, copper, boards, plank, etc.

Turkey and the Eastern Mediterrean

Turkey/Levant Company

broadcloth, long-ells, tins, lead, and some iron (also sugar sourced from France and Lisbon)

raw silk, grogram yarn, dyeing stuffs of sundry kinds, drugs, soap; leather, cotton, and some fruit, oil, etc.

India and China

East India Company

great quantities of bullion, lead, English cloth, and some other goods

tea, china ware, cabinets, raw and wrought silks, coffee, muslins, calicoes, and other goods

Africa

Royal African Company

[slaves]1

gold dust and other commodities, as red wood, elephants' teeth, Guinea grain

Canary Islands

Canary Company

baize, kerseys, serges, Norwich stuffs, and other woollen

manufactures; stockings, hats, fustians, haberdashery wares, tin, and

hardware; as also herrings, pilchards, salted flesh, and grain; linens,

pipe- staves, hoops, etc.

wines, logwood, hides, indigo, cochineal, and other commoditiesi, the produce of America and the West Indies

Canada

Independent Merchants

woollen goods and haberdashery wares, knives, hatchets, arms, and other hardware

beaver-skins, and other skins and furs

Italy

Independent Merchants

broad-cloth, long-ells, baize, druggets, callimancoes, camlets, and

divers other stuffs; leather, tin, lead, great quantities of fish, as

pilchards, herrings, salmon, Newfoundland cod, etc., pepper, and other

East India goods

raw, thrown, and wrought silk, wine, oil, soap, olives, some dyer's wares, anchovies, etc.

Spain

Independent Merchants

broad-cloth, druggets, callimancoes, baize, stuff of divers kinds, leather, fish, tin, lead, corn, etc.

wine, oil, fruit of divers kinds, wool, indigo, cochineal, and dyeing stuffs

Portugal

Independent Merchants

broad-cloth, druggets, baize, long- ells, callimancoes, and all

other sorts of stuffs; as well as tin, lead, leather, fish, corn, and

other English commodities

great quantities of wine, oil, salt, and fruit, and gold, both in bullion and specie

France

Independent Merchants

Wool [mostly smuggled], tobacco, sugar, tin, lead, coals, a few stuffs, serges, flannels, and a small matter of broad-cloth

wine, brandy, linen, lace, fine cambrics, and cambric lawns, to a

prodigious value; brocades, velvets, and many other rich silk

manufactures

Flanders

Independent Merchants

serges, a few flannels, a very few stuffs, sugar, tobacco, tin, and lead

fine lace, fine cambrics, and cambric-lawns, Flanders whited

linens, threads, tapes, incles, and divers other commodities, to a very

great value

Holland

Independent Merchants

broad-cloth, druggets, long-ells, stuffs of a great many sorts,

leather, corn, coals, and something of almost every kind that this

kingdom produces; besides all sorts of India and Turkey re-exported

goods, sugars, tobacco, rice, ginger, pitch and tar, and sundry other

commodities of the produce of our American plantations

great quantities of fine Holland linen, threads, tapes, and

incles; whale fins, brass battery, madder, argol, with a large number of

other commodities and toys; clapboard, wainscot, etc.

Ireland

Independent Merchants

fine broad-cloth, rich silks, ribbons, gold and silver lace,

manufactured iron and cutlery wares, pewter, great quantities of hops,

coals, dyeing wares, tobacco, sugar, East India goods, raw silk,

hollands, and almost everything they use, but linens, coarse woollens,

and eatables

woollen yarn, linen yarn, great quantities of wool in the fleece, and some tallow

Sugar Plantations2

Independent Merchants

all sorts of clothing, both linen, silks, and woollen; wrought

iron, brass, copper, all sorts of household furniture, and a great part

of their food

sugar, ginger, and several commodities, and all the bullion and gold they can meet with

Tobacco Plantations3

Independent Merchants

clothing, household goods, iron manufactures of all sorts, saddles,

bridles, brass and copper wares; and notwithstanding they dwell among

the woods, they take their very turnery wares, and almost everything

else that may be called the manufacture of England

not only what tobacco is consumed at home, but very great quantities for re-exportation

1. The Africa Company did not export as such. Instead it gathered and

sold African slaves for use on plantations and paid for imports with

the proceeds.

2. 3. Sugar and Tobacco Plantations are listed in the same way as

countries, demonstrating the enormous wealth these entities generated.

You remember the Lamborghinis parked outside the cryptocurrency get-togethers earlier this year, right?

And that it was all fantasy?

I think someone at FTAV noted they were hourly rentals, this was one of the headlines they pointed to:

Anyway here's something real to aspire to.

From LEGO:

Testament that with LEGO Technic you can build for real,

this non-glued, fully-functional and self-propelled LEGO Technic model

can fit two passengers inside and accelerate to over 20km/h

Perfectly recreating the organic design lines of

the world’s fastest production car – the iconic Bugatti Chiron – the

LEGO Technic life-size model pushes the boundaries of what LEGO builders

imagined was possible to build in LEGO elements.

The model is the first large scale movable construction developed using over 1,000,000 LEGO Technic elements and powered exclusively using motors from the LEGO Power Function platform.

Packed with 2,304 motors and 4,032 LEGO Technic gear wheels, the engine

of this 1.5 tonnes car is generating 5.3 horse power and an estimated

torque of 92 Nm.

Lena Dixen, Senior Vice President of Product and Marketing at the LEGO Group said:

“This

life-size model is a first of its kind in so many ways and with it, we

wanted to push the boundaries of our own imagination. For over 40 years,

LEGO Technic has allowed fans of all ages to test their creativity with

a building system that challenges them to go beyond just creating new

designs, to also engineering new functions. Our Technic designers and

the engineers from the Kladno factory in the Czech Republic, the place

which also builds the impressive models for LEGO Stores and LEGOLAND

parks, have done an amazing job both at recreating the Chiron’s iconic

shapes and making it possible to drive this model. It’s a fascinating

example of the LEGO Technic building system in action and its potential

for creative reinvention.”

BEIJING, Aug 30 (Reuters) - China has

launched a platform, which includes a mobile app, that lets the public

report "online rumours" and even uses artificial intelligence to

identify reports that are false, as Beijing cracks down on what it views

as socially destabilising content.

The platform,

launched on Wednesday, comes as Beijing steps up efforts to police the

internet, especially social media used by people to discuss politics and

other sensitive subjects, despite stringent censorship.

Besides

a website, the platform Piyao - which means "refuting rumours" - also

has a mobile app and social media accounts with social media giants

Weibo and WeChat.

Via those channels, Piyao will

broadcast "real" news, sourcing reports from state-owned media,

party-controlled local newspapers, and various government agencies.

"Rumours

violate individual rights; rumours create social panic; rumours cause

fluctuations in the stock markets; rumours impact normal business

operations; rumours blatantly attack revolutionary martyrs," Piyao said

in a promotional video of the launch on its website.

Official

data show internet regulators received 6.7 million reports of illegal

and false information in July, with most of the cases coming from Sina

that owns Weibo, Tencent which owns Wechat, Baidu, and Alibaba .

Chinese

laws dictate that rumour-mongers could be charged with defamation, and

they face up to seven years in prison. Online posts that contain rumours

visited by 5,000 internet users or are reposted more than 500 times

could also incur jail sentences.

Hosted by the

Central Cyberspace Affairs Commission in affiliation with the official

Xinhua news agency, Piyao has integrated over 40 local rumour-refuting

platforms and uses artificial intelligence to identify rumours....MORE

Here's commentary from Fleetwod Mac:

Probably not suitable for play in China.

What with the Rumours and the Go your own way, and all.

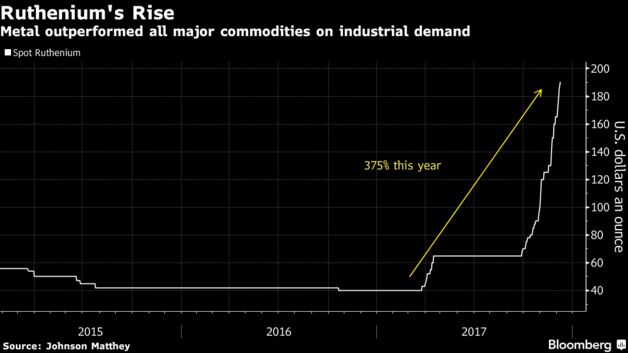

We've been posting on lithium for over a decade, but when given the choice in 2016 between touting lithium or cobalt, went with the latter, which then became the top performing tradable commodity 2016-2018.

All good things come to an end, we moved on to ruthenium, and haven't had much on either of the battery elements.

Some links below.

Today's story is from Reuters, Aug. 29:

As global demand for lithium hits overdrive, Albemarle Corp is investing

millions of dollars to engineer specialized types of the light metal

for electric car batteries, part of a strategy to remain the niche

market’s top producer.

The pivot comes as battery makers such as Panasonic Corp, the sole

battery supplier to Tesla Inc, increasingly demand more purified

versions of lithium that can help boost electricity storage and increase

a battery’s charge, shaping Albemarle’s strategy, according to sources

and documents reviewed by Reuters and confirmed by the company.

Once

used primarily as a pharmacological treatment for bipolar disorder,

lithium has become one of the world’s most in-demand commodities thanks

to the rising popularity of electric vehicles powered by lithium-ion

batteries.

Roughly 500,000 electric vehicles were sold globally

in 2016, a figure that is expected to jump sevenfold by 2022, according

to estimates from the U.S. Energy Information Administration.

Albemarle’s

strategy, which includes developing a battery research center near its

North Carolina headquarters, is aimed at setting it apart from its major

competitors, including Chile’s SQM and China’s Tianqi Lithium Corp.

Albemarle

has historically sold basic types of lithium under short-term

contracts, much like rivals. Now, the company is diverging from rivals

and developing dozens of lithium products that can help boost

electricity storage and increase a battery’s charge.

The pivot comes as battery makers such as Panasonic Corp, the sole

battery supplier to Tesla Inc, increasingly demand more purified

versions of lithium that can help boost electricity storage and increase

a battery’s charge, shaping Albemarle’s strategy, according to sources

and documents reviewed by Reuters and confirmed by the company.

Once

used primarily as a pharmacological treatment for bipolar disorder,

lithium has become one of the world’s most in-demand commodities thanks

to the rising popularity of electric vehicles powered by lithium-ion

batteries.

Roughly 500,000 electric vehicles were sold globally

in 2016, a figure that is expected to jump sevenfold by 2022, according

to estimates from the U.S. Energy Information Administration.

Albemarle’s

strategy, which includes developing a battery research center near its

North Carolina headquarters, is aimed at setting it apart from its major

competitors, including Chile’s SQM and China’s Tianqi Lithium Corp.

Albemarle

has historically sold basic types of lithium under short-term

contracts, much like rivals. Now, the company is diverging from rivals

and developing dozens of lithium products that can help boost

electricity storage and increase a battery’s charge...MORE

It's been a tough year for ALB as well as for the world's other largest producer, SQM:

The US International Trade Commission officially nixed the Trump

administration's tariffs on Canadian newsprint on Wednesday, overturning

a decision made earlier this year by the US Commerce Department that

caused paper costs to increase by as much as 35% and publishers to institute further cutbacks in an already struggling industry.

Wilbur Ross, the embattled US Secretary of Commerce and former private

equity titan, originally instituted the tariffs in March after North Pacific Paper Company (aka

NORPAC), a mill in Longview, WA, that's owned by One Rock Capital,

argued that Canadian newsprint was being subsidized and "dumped" into

the US at unfairly low prices. Of the five US-based mills still in

operation, NORPAC was the only company to complain.

Ross' decision drew a swift rebuke from the publishing industry and

beyond. Last month, newspaper publishers were joined by a bipartisan

group of lawmakers in appealing the decision to the US Commerce

Department. Ross ultimately relented a bit, lowering the duty by about 5

percentage points and capping the tariffs below 20%.

In reaching its unanimous 5-0 decision, the ITC determined that there

was no material harm being caused the Canadian mill's pricing. In other

words, NORPAC's argument was paper thin....MORE

That we were going to revisit in a couple weeks for the crypto angle.

Thinking about it now, she may have been on to something, regarding not just the HODLers but investing in general, a point that one of the great financial writers, E.F. Hutton & Co's Gerald Loeb* made a few times.

In the same mold is Dan McCrum, second-in-command/acting editor at FT Alphaville.

He is so gimlet-eyed [read: doubting] I found myself changing the lyrics to the song from Disney's "The Happiest Millionaire" from "Fortuosity, that's me byword!" to "Dubiosity that's me byword!"

Here's FT Alphaville:

Elm Partners had great intellectual success three years ago with a

bullish argument for long term equity returns, even if their clickbaity

claim for “the most important number you won't find in the Wall Street

Journal” failed to bait many clicks:...

***

...However the asset manager has doubled down with a similar argument in blog form.

No matter that stock markets have been rising for the best part of a

decade, long term returns for investors are going to be great! A precise

5.3 per cent a year, after inflation no less:

How

do we arrive at our estimate of 5.3% real return? First, we need a

simple and fundamentally sound predictor for each major regional equity

market. One such measure is the Cyclically Adjusted Earnings Yield, i.e.

1 / CAPE, as suggested 30 years ago in a seminal paper by Shiller and

Campbell.3 While

there isn’t enough historical data to statistically derive a high level

of confidence in this predictor, such evidence as there is combined

with its fundamental economic rationale supports its use as a reasonable

indicator.4 By

way of anecdotal context, the Cyclically Adjusted Earnings Yield in

1968 was 4.6% for US equities, and the actual real return over that

period has been 5.8% – not spot on, but not too bad either given all

that’s happened over those 50 years.5

A lot to unpack there, not least the passing reference to a much debated indicator which lacks the data to give statisticians confidence.

As we have noted before, there is also a lot of looking back

to the late 1960s and early 1970s at the moment, possible as the well

of post-Carter Administration analysis has run dry. Over half a century,

stock market returns have been good, but the 15 year years after 1968

were diabolical for stock market investors.

Here, for instance, is the inflation-adjusted index level for the S&P 500 for that period, as calculated by Macrotrends:...

There is reason to believe the current bull market has simply pulled-forward the expected returns of the next decade meaning the recent past is definitely not prologue.

More on that another time.

*Among other things, Mr. Loeb thought it important that the general public be exposed to matters financial and to that end tried to recognize the exposers (that sounded better in my head):

The Gerald Loeb Awards were established

in 1957 by the late Gerald Loeb, a founding partner of E.F. Hutton. His

intention was to encourage reporting on business and finance that would

inform and protect the private investor and the general public. As the

most prestigious honor in business journalism, distinguished journalists

and outlets nationwide submit entries to the competition....

The results were pretty grim statewide, with one

exception: Those polled in the Bay Area tend to be much more optimistic

about their chances in the Golden State compared to Californians in

surrounding regions.

Some illustrative examples from the data:

Californians don’t believed in the “American dream”: Asked

whether they believed those who work hard will eventually get ahead, a

plurality 47 percent of workers statewide said yes. However, another 43

percent said that this was true in the past but no longer the case. And

10 percent are of the opinion it was never true in the first place.

Neither does the Bay Area: Despite the fact that Bay

Area residents say they’re better off financially than the rest of the

state, local figures are slightly worse for the American dream question:

only 45 percent still believe in it, versus 44 percent who say it’s

come and gone and 11 percent who believe it was a myth in the first

place.

Bay Area more likely to believe in the “California dream”:

Asked whether it’s easier to get ahead in California versus other

states, only 16 percent of California workers agreed. Fifty-five percent

said it’s harder here. In the Bay Area the number of those who say

easier is slightly higher—18 percent—but so too is the number of those

who call it harder: 59 percent.

Most Californians ready to tell others to “go east”:

Overall, some 64 percent of those polled across the state would advise

younger people to try their luck getting ahead in some other state. The

only exception to this trend was in the Bay Area, where 55 percent

advised people stay here and give California a shot....

A twofer. First up the link that was in the queue, CNBC August 29:

Campbell Soup is undergoing an operational review in which it will assess the entirety of its portfolio.

Its "no sacred cows" approach has left industry sources wondering whether the soup company could put itself up for sale.

The company's iconic cans are a fixture of American culture.

Campbell Soup was founded shortly after the Civil War, and for the majority of its lifespan has been a family company.

It's uncertain how much longer it will remain one.

The soup company is undergoing

an operational review that will assess the entirety of its portfolio.

While a "no sacred cows" approach has left industry sources wondering

whether the soup giant could put itself up for sale, the company has

weathered such speculation before. Every time that speculation has

arisen, Campbell — and the family that together comprises its largest

shareholders — has opted to keep it a family heirloom.

Times have changed. The

descendants of John T. Dorrance — the man who many say invented

condensed soup — are now in their fourth generation. Some of his family

members have decreased their stake in the soup company. Many have not

worked for it for extended periods of time.

Campbell's problems are many, and growing. Retailers like Walmart,

which once needed Campbell on its shelves, have lost patience with its

declining soup sales. It also faces competition from upstart brands that

appeal to the younger generation's focus on health and newness.

Its once arch-enemy, The H. J. Heinz Company, was acquired by Berkshire

Hathaway and private equity firm 3G Capital back in 2013. Heinz went on

to merge with Kraft Foods Group in 2015 to create Kraft Heinz.

As of Friday's market close, the ketchup and snack giant has a market

capitalization of over $73 billion, compared to around $12 billion for

Campbell....MORE

And this morning, again from CNBC:

Campbell Soup plans to sell international and fresh food businesses, remains 'open' to sale

Campbell Soup reveals its plans to turnaround the company after announcing a top-to-bottom strategic review in May.

The company is selling its fresh food business, including Bolthouse Farms, as well as its Arnott's and Kelsen brands overseas.

Activist shareholder, Dan Loeb is calling for Campbell to sell itself.

We don't much care for these so-called food companies having posted on General Mills and Kellogg in particular as the stocks were halved over the last couple years. Here's our last post on Campbell Soup, May 2018:

A serious look at the golden arches.

From Nanalyze:

We spend the vast majority of our waking hours trying to figure out

the best way to invest in disruptive technologies, but that’s not where

we actually allocate the lion’s share of our investments. Instead, our

hard-earned dollars can be found in boring industries like insurance or consumer goods which

are more likely to provide predictable cash flows in the form of

dividends that grow slowly over time. It’s probably the “safest” way

we’ve seen to invest in equities, provided that you diversify across

industries and hold a large enough number of stocks for diversification.

Additionally, we like to invest in large multinational firms to avoid

being over-reliant on those crazy Yanks.

Speaking of which, one

thing you’ll see in Yankee land is a whole lot of overweight people. At

least that’s what one of our Danish MBAs remarked as he experienced a

McDonald’s (MCD)

drive-through for the very first time in his life. In Denmark, they

don’t have drive-throughs, and they’re also crazy enough to believe that

big isn’t beautiful, it’s unhealthy. Denmark has a total of 88

McDonald’s outlets, less than 0.02% of the 37,404 total Mickey D’s

restaurants that can be found occupying some of the most prime real

estate in 120 countries around the world. All those restaurants have

collectively helped McDonald’s pay dividends every single year for 42

years, each year more than the last. So how can McDonald’s continue to

grow those payments moving forward? Well, they can increase sales or

decrease costs.

Increasing Sales or Decreasing Costs?

When it comes to increasing sales, that might come from entering new markets like Kenya,

being more clever with advertising spend, or developing new food

products to increase sales (think all day breakfasts). When it comes to

decreasing costs, the biggest bang for the buck appears to be reducing

labor costs. At least that’s the case for franchised McDonald’s

restaurants where labor is the biggest expense at 24% of net sales:

McDonald’s Franchise Income Statement

The

above numbers were taken from a firm called Janney Capital markets, and

we can’t confirm the accuracy of the data nor the date it was

published. Still, let’s assume employing humans amounts to 24% of costs.

Then, add to that the whole minimum wage debate about paying workers

$15 an hour, something that a previous McDonald’s executive said would

result in “a job loss like you can’t believe“. This, of course, led to some rumors that McDonald’s may decrease costs by adopting the type of robotics technology we talked about before in our article on A High-Tech Burger Joint of the Future:...

The world’s largest container shipping line says adhering to stricter

environmental standards could add at least $2 billion to its annual

fuel bill from 2020, one of the clearest examples yet of how vessel

owners will be affected by rules to curb sulfur emissions that take

effect in 16 months’ time.

High crude prices, tight availability of compliant

fuels, and investment in research and development are among issues that

will combine to drive up the cost of complying with IMO 2020, said Simon

Bergulf, director for regulatory affairs at A.P. Moller-Maersk A/S, the

Copenhagen-based operator of hundreds of container ships and smaller

craft like tug boats.

“I wouldn’t call it a perfect storm, but it’s close,” Bergulf said,

adding that marine fuel suppliers who Maersk is in contact with aren’t

concerned about a ship-fuel shortage.

While there’s a growing consensus that the new rules to

limit sulfur emissions will have far-reaching consequences for oil

refiners, shippers and even trade, few large companies have attempted to

quantify that impact publicly. Maersk, which spent $3.37 billion on

fuel last year, says the increase could even exceed $2 billion — and

that’s before taking into account further spending on things like

research and development.

There isn’t currently a single, widely traded contract

that captures the price of the new fuel vessels will have to use. ICE

Gasoil, lower in sulfur than would be necessary, is more than double the

price of high-sulfur fuel in January 2020, when the new rules start,

according to data compiled by Bloomberg.

Large increases to expenses could tempt some companies to cheat by

using fuel that doesn’t meet the regulations set out two years ago by

the International Maritime Organization.

Rule Breaking

A large container ship hauling goods to Europe from Asia

might save in the region of $700,000 just for one delivery if it broke

the rules, Bergulf said, adding that Maersk is committed to full

compliance....MORE

Not "next" as in tomorrow but next as in the next major trend.

It's pretty easy, most folks can see it out there on the horizon. the bend at the end of the current trend, friend.

(sorry, old line, repurposed)

The trick is getting the timing right, or at least right enough for Q3 and Q4 to nail down some bonus money.

Here's Martin Feldstein, currently at Harvard and President Emeritus of the National Bureau of Economic Research. In a prior life he was chairman of the Council of Economic Advisers and picked up a John Bates Clark Medal.

From Project Syndicate, August 28:

August 22 marked the longest period of rising share

prices in US history. But the stock market's nine-year bull run won't

last much longer, as three factors drive up long-term interest rates,

reducing the present value of future corporate profits and providing

investors with an alternative to equities.

CAMBRIDGE

– The US stock market achieved its longest rise in its history on

August 22, with the Standard and Poor’s 500 index up by 230% since 2009.

Although this wasn’t the biggest increase in a bull market, it marked

the longest period of increasing share prices.

Several forces

contributed to this impressive nine-year run. The primary driver has

been the extremely low interest rates maintained by the Federal Reserve.

The Fed cut its short-term federal funds rate to near-zero in 2008 and

did not begin to increase it above 1% until 2017. Even now, the federal

funds rate is lower than the annual inflation rate. The Fed also

promised to keep the short rate low for a long period of time, causing

long-term rates to remain low as well. With interest rates so low for so

long, investors seeking higher returns bought shares, driving up their

prices.

A rational model of

share prices sets them equal to the present value of future profits. Low

interest rates raised the present value of future profits, and the

corporate tax reform enacted at the end of 2017, together with

deregulation in several industries, has raised both current profits and

expected future profits, contributing to the present value of future

profits.

But even with rising

profits, low interest rates have caused share prices to increase faster

than profits. As a result, the S&P price-earnings ratio is now more

than 50% higher than its historic average.

With real

(inflation-adjusted) GDP rising at more than 3% this year, the strength

of the US economy has induced foreign investors to shift their holdings

to US equities. And in recent months, US households that had not owned

stocks in the past, fearful of missing out on the bull market, have

joined the equity bandwagon.

But what of the

future? Stock-market booms don’t die of old age; they are generally

killed by higher interest rates. That often happens when the Fed raises

the short-term interest rate to stop or reverse rising inflation.

Although the Fed’s preferred rate of inflation – the price of consumer

expenditures – has just reached its target of 2%, other measures of

price growth are rising more rapidly. The overall Consumer Price Index

(CPI) is now 2.9% higher than it was a year ago. Even “core” consumer

inflation, which strips out more volatile food and energy prices, has

increased by 2.4% over the past year.

The Fed’s short-term

interest rate is now just 1.75%, implying that the real rate is still

negative. The Fed’s Open Market Committee has now projected

that it will raise the federal funds rate to 2.4% by the end of 2018,

to 3.1% by the end of 2019, and to 3.4% by the end of 2020.

My judgment is that

the greatest risk to the stock market is the future increase in

long-term interest rates. The interest rate on ten-year Treasury bonds

is now about 2.9%, implying a zero real rate when compared to the

current level of the CPI. Historically, the real ten-year Treasury rate

has been about 2%, implying that the ten-year rate might rise to 5%.

Three factors will

contribute to the rise in the long-term rate. The Fed’s projected

increase in the federal funds rate will put upward pressure on the

ten-year interest rate. With the unemployment rate at 3.9% and likely to

decline further in the year ahead, the rate of inflation should

continue to increase. And even if that does not cause the Fed to raise

the federal funds rate at a faster pace, higher inflation by itself will

cause investors to demand higher long-term rates to compensate for the

loss of their funds’ real value....MORE

The 10-year at 5% would definitely curb enthusiasm for equities and much else.

We aren't there yet, and until markets have their collective Wile E. Coyote moment calling the top in equities is a tough thing to do.

And for what it's worth, that slightly negative real short rate is the only thing supporting gold.

The economy continues to grow, yet wages remain flat. Corporate concentration may be to blame.

The Kansas City Federal Reserve, one of the dozen reserve banks in the

U.S., gathered on Friday in Jackson Hole, Wyoming, to discuss a

signature puzzle of our times: How can the economy hum along, with

unemployment falling for years, without wage growth? How have the gains

from the economy been segregated from most Americans who do the work,

instead flowing into the hands of a small group at the top? And what can

the Fed, or anyone, do to reverse this?

The main culprit discussed at the economic policy symposiumwas

increasing corporate concentration: the limited number of firms in any

one industry. A series of working papers and speeches examined

monopolization’s impact on various aspects of the economy, from worker

bargaining power to capital investment to inflation. While the Fed isn’t

singularly responsible for policing market competition, it does have

the power of the megaphone, and the implications of the research

unveiled last week should signal a sea change across government: either

tame the corporate giants, or watch helplessly as they eat everything

not nailed down.

Northwestern University’s Nicolas Crouzet and Janice Eberly submitted a paper

about what they call “intangible capital”—intellectual rather than

physical property, such as patents, software, or even copyrighted

brands. Over the last two decades, businesses have invested more in

these intangibles than in physical capital like factories and workers;

according to the authors, this can account for nearly all of the drop in

physical capital investment since 2000. If you have a patented product

that nobody else can manufacture, why bother to spend money attracting

top talent?

Crouzet and Eberly show this dynamic is most

pronounced in the tech and health care sectors, where patents are

particularly valuable. “The platform developed by an online retailer is

just as crucial to producing revenue as an oil platform is to an energy

firm,” the authors write. And they see a link to market power, as large

firms use intangibles to exclude competitors.

This is important to the Fed because in economic downturns, it

lowers interest rates to entice capital expenditures and give the

economy a boost. Similarly, Congress often tries to kick-start the

economy with investment tax credits. If apps and drug patents are more

critical to the modern economy, these interventions won’t work as well.

An even more intriguing paper,

from Alberto Cavallo of the Harvard Business School, scrutinizes the

rise of online retail and the algorithms that cause prices to constantly

fluctuate. If Amazon finds that more people buy pens in the morning,

pens could be more expensive then, for example. And because the retail

world has a “follow-the-leader” mentality when it comes to Amazon, this

has been widely replicated, leading to a high degree of uniformity

across the country.

In other words, Amazon has created its own ecosystem, with precise,

rapid swings in prices not necessarily related to the common factors of

supply and demand. You might expect that Amazon’s presence lowers prices

generally, as it tries to undercut the competition. But by studying

thousands of prices, Cavallo finds that the “Amazon effect” can react

faster to “shocks” like spiking gas prices, natural disasters, a sudden

change in the value of the dollar, or tariffs. When these shocks happen,

companies can transfer the price to customers faster than ever. “The

implication is that retail prices are becoming less insulated from these

common nationwide shocks,” Cavallo writes....MUCH MORE

A new form of misinformation is poised to spread through online

communities as the 2018 midterm election campaigns heat up. Called

“deepfakes” after the pseudonymous online account that popularized the technique

– which may have chosen its name because the process uses a technical

method called “deep learning” – these fake videos look very realistic.

Because these techniques are so new, people are having trouble

telling the difference between real videos and the deepfake videos. My work, with my colleague Ming-Ching Chang and our Ph.D. student Yuezun Li, has found a way to reliably tell real videos from deepfake videos.

It’s not a permanent solution, because technology will improve. But

it’s a start, and offers hope that computers will be able to help people

tell truth from fiction.

Deepfake algorithms work the same way: They use a type of machine learning system called a deep neural network

to examine the facial movements of one person. Then they synthesize

images of another person’s face making analogous movements. Doing so

effectively creates a video of the target person appearing to do or say

the things the source person did.

Before they can work properly, deep neural networks need a lot of

source information, such as photos of the persons being the source or

target of impersonation. The more images used to train a deepfake

algorithm, the more realistic the digital impersonation will be.

Detecting blinking

There are still flaws in this new type of algorithm. One of them has

to do with how the simulated faces blink – or don’t. Healthy adult

humans blink somewhere between every 2 and 10 seconds, and a single blink takes between one-tenth and four-tenths of a second. That’s what would be normal to see in a video of a person talking. But it’s not what happens in many deepfake videos....

...In yesterday's "Questions America Wants Answered: How Will Brexit Affect The Art Market?"

I amused myself with the provincialism of the headline question,

somewhat akin to the old joke about the small Italian town that sent its

most esteemed resident, a tailor by trade, to represent said villaggio

at an audience with the Pope. Upon his return from Rome the citizens

crowded around and asked "What kind of man is Il Papa?

Their emissary replied, "About a 42 regular"....

We all see the world through our own self-created lenses. And on a

related provincialism point, easily the most terrifying news of the last

couple years:

The Desperate Quest for Genomic Compression Algorithms

Have you had your genome sequenced yet? Millions of people around the world already have, and by 2025 that number could reach a billion.

The more genomics data that researchers acquire, the better the

prospects for personal and public health. Already, prenatal DNA tests

screen for developmental abnormalities. Soon, patients will have their

blood sequenced to spot any nonhuman DNA that might signal an infectious disease.

In the future, someone dealing with cancer will be able to track the

progression of the disease by having the DNA and RNA of single cells

from multiple tissues sequenced daily.

And DNA sequencing of entire populations will give us a more complete picture of society-wide health. That’s the ambition of the United Kingdom’s Biobank,

which aims to sequence the genomes of 500,000 volunteers and follow

them for decades. Already, population-wide genome studies are routinely

used to identify mutations that correlate with specific diseases. And

regular sequencing of organisms in the air, soil, and water will help

track epidemics, food pathogens, toxins, and much more.

This vision will require an almost unimaginable amount of data to be

stored and analyzed. Typically, a DNA sequencing machine that’s

processing the entire genome of a human will generate tens to hundreds

of gigabytes of data. When stored, the cumulative data of millions of

genomes will occupy dozens of exabytes.

And that’s just the beginning. Scientists, physicians, and others who find genomic data useful aren’t going to stop at sequencing each individual just once [PDF]—in

the same individual, they’ll want to sequence multiple cells in

multiple tissues repeatedly over time. They’ll also want to sequence the

DNA of other animals, plants, microorganisms, and entire ecosystems as

the speed of sequencing increases and its cost falls—it’s just US $1,000 per human genome now and rapidly dropping. And the emergence of new applications—and even new industries—will compel even more sequencing.

While it’s hard to anticipate all the future benefits of genomic

data, we can already see one unavoidable challenge: the nearly

inconceivable amount of digital storage involved. At present the cost of

storing genomic data is still just a small part of a lab’s overall

budget. But that cost is growing dramatically, far outpacing the decline

in the price of storage hardware. Within the next five years, the cost

of storing the genomes of billions of humans, animals, plants, and

microorganisms will easily hit billions of dollars per year. And this

data will need to be retained for decades, if not longer.

Compressing the data obviously helps. Bioinformatics experts already

use standard compression tools like gzip to shrink the size of a file by

up to a factor of 20. Some researchers also use more specialized

compression tools that are optimized for genomic data, but none of these

tools have seen wide adoption. The two of us do research on data

compression algorithms, and we think it’s time to come up with a new

compression scheme—one that’s vastly more efficient, faster, and better

tailored to work with the unique characteristics of genomic data. Just

as special-purpose video and audio compression is essential to streaming

services like YouTube and Netflix, so will targeted genomic data

compression be necessary to reap the benefits of the genomic data

explosion.

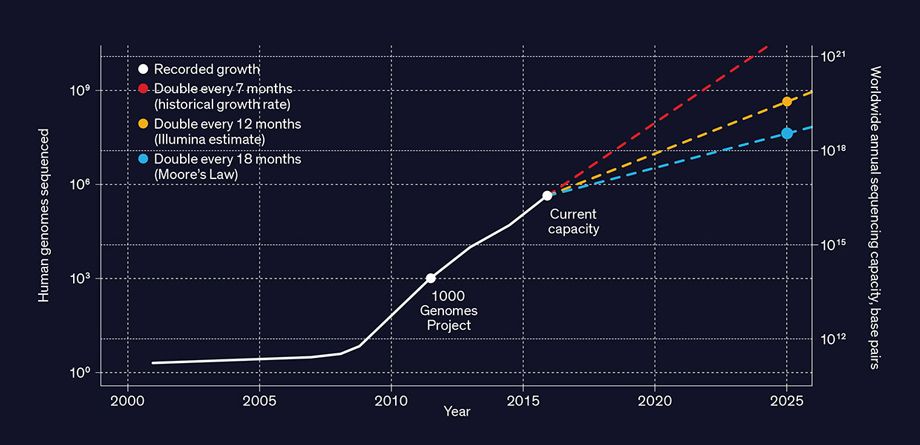

Growth of Human Genome Sequencing: Since the first

publication of a draft human genome sequence in 2001, there’s been a

dramatic increase in the pace of growth of both the number of genomes

sequenced and the sequencing capacity.

The numbers after 2015 represent

three possible projected growth curves.

Before we explain how genomic data could be better

compressed, let’s take a closer look at the data itself. “Genome” here

refers to the sequence of four base nucleotides—adenine, cytosine,

guanine, and thymine—that compose the familiar A, C, G, T alphabet of

DNA. These nucleotides occur in the chains of A-T and C-G pairs that

make up the 23 pairs of chromosomes in a human genome. These chromosomes

encompass some 6 billion nucleotides in most human cells and include

coding genes, noncoding elements (such as the telomeres at the ends of

chromosomes), regulatory elements, and mitochondrial DNA. DNA sequencing

machines like those from Illumina, Oxford Nanopore Technologies, and Pacific Biosciences are able to automatically sequence a human genome from a DNA sample in hours.

These commercial DNA sequencers don’t produce a single genome-long

string of ACGTs but rather a large collection of substrings, or “reads.”

The reads partially overlap each other, requiring sequence-assembly

software to reconstruct the full genome from them. Typically, when

whole-genome sequencing is performed, each piece of the genome appears

in no more than about 100 reads.

Depending on the sequencing technology used, a read can vary in

length from about 100 to 100,000 base pairs, and the total number of

reads varies from millions to tens of billions. Short reads can turn up

single base-pair mutations, while longer reads are better for detecting

complicated variations like deletions or insertions of thousands of base

pairs.

DNA sequencing is a noisy process, and it’s common for reads to

contain errors. And so, besides the string of ACGT nucleotides, each

read includes a quality score indicating the sequencing machine’s

confidence in each DNA nucleotide. Sequencers express their quality

scores as logarithms of error probabilities. The algorithms they use to

do so are proprietary but can be checked after the fact. If a quality

score is 20—corresponding to an error probability of 1 percent—a user

can confirm that about 1 percent of the base pairs were incorrect in a

known DNA sequence. Programs that use these files rely on quality scores

to distinguish a sequencing error from, say, a mutation. A true

mutation would show a higher average quality score—that is, a lower

probability of error—than a sequencing error would.

The sequencer pastes together the strings and the quality scores,

along with some other metadata, read by read, to form what is called a

FASTQ file. A FASTQ file for an entire genome typically contains dozens

to hundreds of gigabytes.

The files are also very redundant, which stems from the fact that any

two human genomes are nearly identical. On average, they differ in

about one nucleotide per 1,000, and it’s typically these genetic

differences that are of interest. Some DNA sequencing targets specific

areas of difference—for example, DNA-genotyping applications like 23andMe

look only for specific variations, while DNA profiling in criminal

investigations looks for variations in the number of repetitions of

certain markers.

But you need to sequence the whole genome if you don’t know where the

interesting stuff lies—when you’re trying to diagnose a disease of

unknown genetic origin, say—and that means acquiring much larger

quantities of sequencing data.

The repetition in sequencing data also comes from reading the same

portions of the genome multiple times to weed out errors. Sometimes a

single sample contains multiple variations of a sequence, so you’ll want

to sequence it repeatedly to catch those variations. Let’s say you’re

trying to detect a few cancer cells in a tissue sample or traces of

fetal DNA in a pregnant woman’s blood. That may mean sequencing each DNA

base pair many times, often more than 100, to distinguish the rare

variations from the more common ones and also the real differences from

the sequencing errors.

By now, you should have a better appreciation

of why DNA sequencing generates so much redundant data. This

redundancy, it turns out, is ideal for data compression. Rather than

storing multiple copies of the same chunk of genomic data, you can store

just one copy.

To compress genomic data, you could first divide each DNA sequence

read into smaller chunks, and then assign each chunk a numerical index.

Eventually, the sum total of indexes constitutes a dictionary, in which

each entry isn’t a word but a short sequence of DNA base pairs.

Text compressors work this way. For example, GitHub

hosts a widely used list of words that people can use to assign each

word its own numerical index. So to encode a passage of text into

binary, you’d replace each word with its numerical index—the list on

GitHub assigns the number 64,872 to the word compression—which

you’d then render in binary format. To compress the binary

representation, you could sort the dictionary by word usage frequency

instead of alphabetical order, so that more common words get smaller

numbers and therefore take fewer bits to encode.

Another common strategy— the Lempel-Ziv family of algorithms—builds

up a dictionary of progressively longer phrases rather than single

words. For example, if your text often contains the word genomic followed by data, a single numerical index would be assigned to the phrase genomic data.

Many general-purpose compression tools such as gzip, bzip2, Facebook’s Zstandard, and Google’s Brotli

use both of these approaches. But while these tools are good for

compressing generic text, special-purpose compressors built to exploit

patterns in certain kinds of data can dramatically outperform them.

Consider the case of streaming video. A single frame of a video and

the direction of its motion enable video compression software to predict

the next frame, so the compressed file won’t include the data for every

pixel of every frame....

Transportation & logistics: Disrupt the transportation and logistics industry

$95.42 down 1.30 [-1.34%].

$95.42 down 1.30 [-1.34%].