If history adheres to timeless long-term trends, Walter Isaacson’s recent book on the digital revolution, The Innovators, could reveal a lot about the future of our digital age. Last week Isaacson, known for his biographies of Steve Jobs and Albert Einstein, spoke about the geniuses behind the last century of innovation at the New-York Historical Society, as part of the World Science Festival. Here are the biggest lessons that future innovators can learn from the recent past....MORE

A new advance, however mechanical, will be a good partner.

Ada Lovelace predicted the partnership between humans and technology in the 1800s, when she saw mechanical looms that weaved tapestries based on the patterns in punched cards. She predicted that machines might one day perform various tasks based on symbols, creating everything from music to math. Yet while others feared the replacement of human thought by technology, Lovelace guessed that machines would remain inextricably intertwined with their makers. More than 100 years later, Isaacson says she was right.

A new advance will be personal.

In the 1960s, computer scientists invented many different devices to help users interact with computers. Yet it was a mouse, similar to the ones we use today, that took root. It’s popular because it exploits instinctive motions, such as pulling downwards to move a visual curser lower on the screen.

The technology will look beautiful.

Isaacson described the day that Steve Jobs unveiled a Macintosh computer, and it displayed the words, “Hello, I’m MacIntosh,” in an attractively styled typeface. “People gasped,” Isaacson said. While most computer engineers had scoffed at fanciful font, considering it unnecessary, Jobs saw power in the beauty of a graphical user interface.

It will be fun.

By the 1980s, researchers realized that inventions ranging from air defense consoles to video games would get faster uptake when they were fun, interactive, graphical, and responsive to the user, says Isaacson.

Further, fun is a good business plan because youth drive change. That’s why Jennifer Lawton, the CEO of the 3D printing company MakerBot, who joined Isaacson on stage at the event, bragged that the plastic in her printers is non-toxic— safe enough for a child or dog to chew on. “We have a mission to get a 3D printer into every school in America,” she says. “We want to make sure that kids see it as a tool to solve problems, or bring an idea to life.”

Like a good host, it will connect the right people.

“The Internet wasn’t designed to be a community-formation thing, but it became that,” said Isaacson. The most successful platforms have been those that facilitate interactions between geographically distant people. The culture that’s emerged from the digital revolution isn’t just a do-it-yourself culture, Isaacson said, but a do-it-ourselves culture....

Friday, October 31, 2014

"6 Traits of Tomorrow’s Blockbuster Digital Technologies"

From Nautil.us Magazine's Facts So Romantic blog:

New High On the Dow Industrials, Not Quite On the S&P 500, Now What? (DIA; SPY)

Thus far in today's session the DJIA's 17,395.54 top-tick is a new all-time high while the S&P's high print of 2,017.45 falls a bit short of the 2019.26 record.

The interesting thing to note about today's action is the lack of euphoria.

Where's the market going?

Higher.

How high?

Don't know.

We've been fortunate just to get the direction right.

Oct. 18 following the Friday close of 1,886.76:

The interesting thing to note about today's action is the lack of euphoria.

Where's the market going?

Higher.

How high?

Don't know.

We've been fortunate just to get the direction right.

Oct. 18 following the Friday close of 1,886.76:

We are looking for a run back to new highs before we break the recent lows which were 1820.66 on the S&P 500, 15,855.12 on the DJIA....Oct. 23 at S&P 1950:

We're still of the opinion that we see new highs on the S&P 500 (above 2,019.26) before we re-visit the recent 1820.66 low. 1950.82 last.We'll have more tomorrow or Sunday or whenever the computers grace us.

Gaming the System: Are Hedge Fund Managers Talented, or Just Good at Fooling Investors?

From Dilbert.com:

And a repost from April 2008:

From Knowledge@Wharton:

Eugene Fama: Do Active Managers Earn Their Fees?

Fama/French: "Luck versus Skill in Mutual Fund Performance" (LMVTX)

The optimal design of Ponzi schemes in finite economies

And a repost from April 2008:

From Knowledge@Wharton:

...'Fake Alpha'Possibly related:

It's easy for an unscrupulous hedge fund manager to make himself look better than he is, as Foster and Young demonstrate in their paper. "We show, in particular, that managers can mimic exceptional performance records with high probability (and thereby earn large fees) without delivering exceptional performance."

An investment pool's returns come in two parts: beta, which is merely riding the coattails of a rising market, and alpha, the extra return produced by smart investment choices. Because hedge funds use leverage, or borrowed money, and invest in derivatives, it is fairly easy to produce "fake alpha," the researchers say.

In their hypothetical example, a fund manager named Oz sets up a $100 million hedge fund with the goal of earning 10 percentage points a year above the 4% annual yield of one-year government bonds. The fund will run for five years and charge a management fee of 2% of assets and an incentive fee of 20% of any profits that exceed the bond yield.

Oz creates and sells a series of "covered calls" and sells them for $11 million. Each call is a stock option that will pay the investor who bought it $1 million if the stock market rises by a given percentage. Using historical information, Oz figures there is only a 10% probability the market will rise that much. If it does, the hedge fund will be virtually wiped out by being forced to pay $111 million to the call owners. If it does not, the fund will pay nothing -- and the $11 million received from the call buyers will be profit.

Oz now has $100 million received from his investors, plus $11 million from the options sales. He invests the $111 million in risk-free U.S. Treasury bills earning 4%. After a year, the fund thus grows to $115.5 million. To his investors, this is a 15.5% return on their original $100 million.

Oz earns his 2% management fee on the $115.5 million, plus 20% of the return exceeding what came from the 4% Treasury yield -- or 20% of $11.5 million.

There's a 59% chance this process can continue for five years without a market downturn annihilating the fund, allowing Oz to collect $19 million in fees as compounding makes the fund grow larger and larger. If the market does crash, Oz can close the fund, leaving the investors with devastating losses but keeping the fees he's been paid to that point.

This simplified "piggy-back strategy" involves no borrowing, or leverage. A real-world manager could inflate his incentive fee by borrowing money to increase the size of his bets, though that would deepen the investors' losses if things went wrong.

The bottom line is that Oz's investors, who don't know what he is doing, may well believe his market-beating results come from brilliant stock picking or other wizardry. In fact, anyone could set up this simple strategy. Moreover, the investors are in the dark about the risks they are taking. They might well assume that if they make in excess of 15% one year, they might lose 15% in another. In fact, there's a 10% chance they will lose more than 95% of the money they put in.>>>MORE

Eugene Fama: Do Active Managers Earn Their Fees?

Fama/French: "Luck versus Skill in Mutual Fund Performance" (LMVTX)

The optimal design of Ponzi schemes in finite economies

GOLD COLLAPSES

The 2013 double bottoms at $1179 and $1181, recently (early Oct.) tested at $1183, have given way and now become overhead resistance. December futures $1165.30 down $33.30 last trade.

Silver has broken $16 at $15.89 down 53 cents.

Our gold target remains $875.00.

From Kitco:

A.M. Kitco Metals Roundup: Gold Sharply Down, Hits 4-Yr Low, on Technical Selling, Strong US Dollar, Rallying Equities

Stage Set For Big Leg Down In Gold Price: Wyckoff

From FinViz:

Silver has broken $16 at $15.89 down 53 cents.

Our gold target remains $875.00.

From Kitco:

A.M. Kitco Metals Roundup: Gold Sharply Down, Hits 4-Yr Low, on Technical Selling, Strong US Dollar, Rallying Equities

Gold prices are sharply lower, hit a four-year low and fell below major long-term technical support that was located at the $1,180.00 area in early U.S. trading Friday. The precious metals are still feeling the bearish effects of a strong rally in the U.S. dollar index. The big rally in world stock markets late this week is also a negative that is pulling away funds from the precious metals markets. December Comex gold was last down $25.60 at $1,173.10 an ounce. Spot gold was last quoted down $26.00 at $1,173.40. December Comex silver last traded down $0.345 at $16.07 an ounce.Also at Kitco (Oct. 30):

There’s a lot going on in the world market place Friday, on this last trading day of the week and of the month. There are three features at work Friday morning: U.S. stock indexes hit fresh record or multi-year highs overnight, the U.S. dollar index is surging, and gold prices have slumped to a four-year low. All have occurred in the wake of Wednesday afternoon’s FOMC statement that was deemed surprisingly hawkish on U.S. monetary policy.

The world equity markets and the greenback got an added boost overnight when the Bank of Japan surprisingly announced further and somewhat aggressive monetary policy easing measures. The BOJ move is an attempt to ward off deflationary pressures that have wracked Japan’s economy for at least the past 15 years. The Japanese yen sunk on the news, but Japan’s Nikkei stock index rallied on the BOJ easing. Other Asian and European stock markets also rallied Friday....MORE

Stage Set For Big Leg Down In Gold Price: Wyckoff

From FinViz:

Did We Just Witness the Slickest Transfer Of Assets In History?

SPY is the ETF for the S&P 500 and, except for a moment of insanity when it was surpassed by the gold ETF, is the largest and most active, some 121 million shares per day at a three figure price.

Looking at this chart from PastStat you see one sweet little fakeout:

Just think of all those shares shaken loose and dumped on the way down and at the bottom. It's almost enough to make one believe in conspiracy theories.

We did our best to stand against the storm, warning this decline was coming, catching the bottom and then calling the upmove. To no avail, the herd does what the herd always does.

This morning's premarket trade is up $2.05 at $201.47.

Today's link is from from PastStats, Oct. 30:

next what ? -> when $SPY posts 10 or more higher lows

ok we are not sure of the data feed that we received at the time of writing :) , but anyway looks like $SPY posted 11 consecutive higher lows’s which triggers below trading strategies

1) $SPY posts 10 or more consecutive higher low’s in row

below the trading odds , for $SPY longs , for the next 1/2/3/4/5 trading days , data since Feb 1993 , minus today’s instance

Looking at this chart from PastStat you see one sweet little fakeout:

Just think of all those shares shaken loose and dumped on the way down and at the bottom. It's almost enough to make one believe in conspiracy theories.

We did our best to stand against the storm, warning this decline was coming, catching the bottom and then calling the upmove. To no avail, the herd does what the herd always does.

This morning's premarket trade is up $2.05 at $201.47.

Today's link is from from PastStats, Oct. 30:

next what ? -> when $SPY posts 10 or more higher lows

ok we are not sure of the data feed that we received at the time of writing :) , but anyway looks like $SPY posted 11 consecutive higher lows’s which triggers below trading strategies

1) $SPY posts 10 or more consecutive higher low’s in row

below the trading odds , for $SPY longs , for the next 1/2/3/4/5 trading days , data since Feb 1993 , minus today’s instance

| Date | $SPY | t+1 % | t+2% | t+3% | t+4% | t+5% | 1st +’ve % |

| 29-Oct-14 | 198.11 | ?? | ?? | ?? | ?? | ?? | ?? |

| 20-May-13 | 162.09 | 0.15 | -0.6 | -0.88 | -0.97 | -0.38 | 0.15 |

| 17-May-13 | 162.1 | -0.01 | 0.14 | -0.6 | -0.89 | -0.97 | 0.14 |

| 16-May-13 | 160.55 | 0.97 | 0.96 | 1.11 | 0.36 | 0.07 | 0.97 |

| 15-May-13 | 161.31 | -0.47 | 0.49 | 0.48 | 0.63 | -0.12 | 0.49 |

| 15-Mar-13 | 151.32 | -0.56 | -0.79 | -0.09 | -0.95 | -0.15 | -0.15 |

| 30-Jan-13 | 145.08 | -0.25 | 0.78 | -0.36 | 0.65 | 0.72 | 0.78 |

| 27-Jul-09 | 88.45 | -0.46 | -0.71 | 0.33 | 0.46 | 2.13 | 0.33 |

| 24-Jul-09 | 88.19 | 0.29 | -0.17 | -0.42 | 0.62 | 0.76 | 0.29 |

| 15-Nov-04 | 97.07 | -0.72 | -0.13 | 0.01 | -1.1 | -0.64 | 0.01 |

| 12-Nov-04 | 96.83 | 0.25 | -0.48 | 0.11 | 0.26 | -0.86 | 0.25 |

| 11-Nov-04 | 96.07 | 0.79 | 1.04 | 0.31 | 0.91 | 1.05 | 0.79 |

| 10-Nov-04 | 95.35 | 0.76 | 1.55 | 1.8 | 1.07 | 1.67 | 0.76 |

| 9-Nov-04 | 95.27 | 0.08 | 0.84 | 1.64 | 1.89 | 1.15 | 0.08 |

| 8-Nov-04 | 95.46 | -0.2 | -0.12 | 0.64 | 1.44 | 1.69 | 0.64 |

| 30-Dec-03 | 89.61 | 0.09 | 0.04 | 1.13 | 1.23 | 1.57 | 0.09 |

| 29-Dec-03 | 89.59 | 0.02 | 0.11 | 0.07 | 1.15 | 1.25 | 0.02 |

| 26-Dec-03 | 88.42 | 1.32 | 1.35 | 1.44 | 1.39 | 2.49 | 1.32 |

| 24-Dec-03 | 88.35 | 0.08 | 1.4 | 1.43 | 1.52 | 1.47 | 0.08 |

| 8-Mar-02 | 91.33 | 0.22 | 0.15 | -0.81 | -0.95 | 0 | 0.22 |

| 29-Nov-96 | 55.5 | 0.04 | -1.68 | -1.41 | -1.68 | -2.25 | 0.04 |

| 27-Nov-96 | 55.29 | 0.38 | 0.42 | -1.3 | -1.03 | -1.3 | 0.38 |

| 23-Jun-95 | 39.12 | -1.2 | -1.38 | -0.87 | -1.05 | -1.1 | -1.1 |

| avg | 0.07 | 0.15 | 0.17 | 0.23 | 0.38 | 0.30 | |

| med | 0.08 | 0.13 | 0.09 | 0.54 | 0.40 | 0.24 | |

| vs all days since 1993 | 0.04 | 0.08 | 0.12 | 0.16 | 0.2 | 0.16 | |

| %wins | 64 | 59 | 59 | 64 | 55 | 91 |

ps: t+1 to t+5 are the percentage changes , and the 1st +’ve is when the entry is set to current close and exit at the first higher close than the entry , with-in the next five trading days , else with a loss at the end of the fifth trading day....MORE

"point is 13/13 times , $SPY posted a higher close than the current close over the next 5 trading days , at some point of time"

CJR: When News Organizations Abet a Scam

From the Columbia Journalism Review:

What should news outlets do when it becomes clear they’ve treated scams as legitimate stories?

On September 15, 2011, executives of Arevenca, an Aruba-based oil company, and Avic Xac, a Chinese state aircraft company, signed the biggest oil deal in history in Madrid. The agreement promised $200 billion a year in trade over 10 years at a total value of $2 trillion. Francisco Javier González, the president of Arevenca, spoke at the signing about plans to supply not only fuel but also ports and railways.

Within hours, the news was out. Scores of news websites around the world carried a wire story from EFE, Spain’s biggest news agency. Viewers could also see a Spanish-language video news report on EFE’s own page or on its YouTube channel; an extended English-language version promptly appeared on González’ YouTube channel.

EFE had been played. Arevenca was little more than a website full of lies and an office in Aruba. The money involved, $200 billion, was comparable to the annual revenue of global corporations like Chevron. Avic Xac has nothing to do with ports. There was barely anyone at the signing ceremony—no ambassadors, no bankers, and, notably, no oil reporters. Despite enough red flags to stock a Communist Party parade, EFE ran its story, both in print and video. Commenters on YouTube quickly said the event was a fraud, but the video is still there. (The article and video have been removed from EFE’s website.)

The screwup would have been long since forgotten, like an unfunny “Yes Men” prank, except that González is a prolific con man. He and his front men have consistently referred back to the EFE coverage as proof of the company’s seriousness as it convinces victims to wire advance payments for oil products which then never arrive—the type of fraud often referred to as a Nigeria scam. A civil court in Puerto Rico judged González liable for stealing $7.8 million from an asphalt company there, and he is now facing criminal complaints in Spain.....MORE

Thursday, October 30, 2014

"SEC Might, Might Not Be Doing Its Job Vis-à-Vis Bitcoin"

From DealBreaker:

There are things at which the Securities and Exchange Commission should probably have a look. Like, say, the unregistered issuance of securities by companies dealing in fake currencies. You know, just a gander, if for no other reason than to demonstrate that they’re expected to follow all of those boring, stupid rules they hate so much. And so they have! Or perhaps not.

Co-founder Evan Wagner said Counterparty had not received any letter from the SEC and that he and his colleagues were unaware of any being received by other firms using its software. Either way, he said, Counterparty is not responsible for the actions of these third-party firms….Perhaps certain octogenarians have played a hand in this relatively free hand….MORE

BitBeat received similarly confident assurances from other prominent Bitcoin 2.0 companies, which seek to facilitate decentralized, middleman-free commercial enterprises.

Ooh, Ooh: "Why didn’t QE3 raise inflation expectations?"

Because Keynes?

Counterfactuals?

Science?

From FT Alphaville:

None of the above?

The inflation talk was a red herring dragged across the path of wealth transfer?

Counterfactuals?

Science?

From FT Alphaville:

The Fed’s balance sheet is no longer in expansion mode, which means it’s time for post-mortems of the most recent asset purchase programme. (Our colleague John Authers has a very good round-up of what did and didn’t happen since QE3 began.)

We want to focus on the fact that the most recent round of bond-buying seemed to have no inflationary impact. If anything, an observer of the data who had no preconceptions about monetary policy operations would conclude that QE3 was disinflationary. Alphaville writers have been exploring this possibility for years (though without firm conclusions).

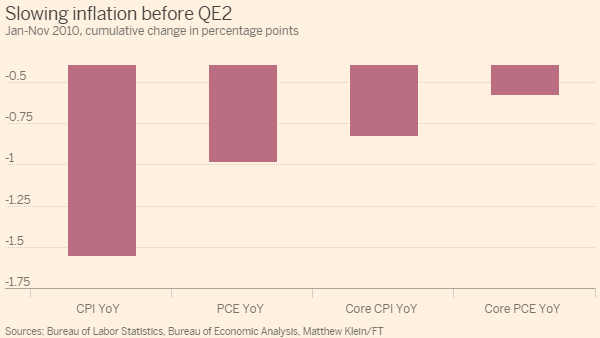

Let’s start by looking at the changes in actual inflation since the start of 2010.

Inflation was slowing dramatically in the period before QE2. Between January, 2010 and Bernanke’s teaser speech at Jackson Hole at the end of August, annual inflation measured by changes in the consumer price index had slowed by 1.4 percentage points, while the annual growth rate of the personal consumption expenditure deflator had decelerated by about 0.8 percentage points. Even price indices that excluded food and energy were slowing sharply.

Inflation continued to slow down until asset purchases began in November, 2010:

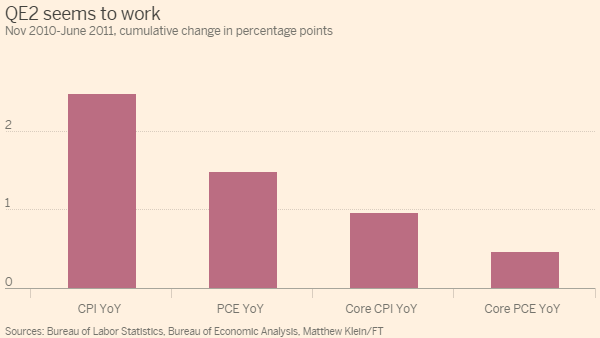

No matter how you measure it, inflation quickly accelerated. The next chart shows how things stood as QE2 was coming to a close in June, 2011:

In fact, the acceleration in inflation since the start of QE2 more than outweighed the initial slowdown in inflation that prompted the Fed to consider the programme in the first place. (We aren’t implying any causal connection, merely noting certain coincidences in timing.)Magic?

Moreover, inflation continued to accelerate in the months after QE2 ended but before Operation Twist and reinvestment of maturing agency MBS began at the end of September. Headline CPI and PCE inflation both peaked in September, 2011. The annual rate of core CPI inflation continued to accelerate until April, 2012, while the rate of core PCE inflation was speeding up until March, 2012.

Thanks to welcome declines in commodity prices due to the combination of increased supply and reduced demand in the rest of the world, headline rates of inflation sharply decelerated after September, 2011. Core inflation slowed down as the spring of 2012 turned into summer, although the pace of core inflation was still significantly faster than when QE2 ended....MUCH MORE

None of the above?

The inflation talk was a red herring dragged across the path of wealth transfer?

Municipal Bonds: "Judge Approves California City’s Bankruptcy-Exit Plan"

From the Wall Street Journal:

Stockton to Slash Payments to Bondholders and Raise Taxes While Not Cutting City Pensions

Judge approves Stockton bankruptcy plan; worker pensions safe

Stockton to Slash Payments to Bondholders and Raise Taxes While Not Cutting City Pensions

The federal judge overseeing the bankruptcy of Stockton, Calif., ruled Thursday the city can exit court protection after slashing payments to bondholders and raising taxes in order to avoid cutting the city’s pensions.And the Los Angeles Times' take on things:

U.S. Bankruptcy Judge Christopher Klein called the city’s reorganization plan “the best that can be done” during a hearing in Sacramento.

Judge Klein approved the city’s reorganization plan over protests from two Franklin Templeton Investments-managed funds, which underwrote the bonds for Stockton’s fire stations and parks. The funds argued that the city could afford to repay more than its $4 million offer.

“We are disappointed,” said Franklin Templeton lawyer James Johnston after the ruling.

The restructuring didn’t call for cutting pension obligations to California Public Employees’ Retirement System, despite critics saying the city would still struggle to afford the state-mandated payments....MORE

Judge approves Stockton bankruptcy plan; worker pensions safe

A federal bankruptcy judge approved the city of Stockton’s bankruptcy recovery plan, allowing the city to continue with planned pension payments to retired workers.

The case was being closely watched after the judge ruled earlier this month that the city’s payments to the California Public Employees’ Retirement System could be cut in bankruptcy just like any other obligation.

If Judge Christopher M. Klein had rejected Stockton’s plan and forced the city to slash its payments to CalPERS, it could have opened the door for other cities struggling with escalating pension costs to follow suit.

Stockton officials had argued that they couldn’t afford to cut pensions or to create another retirement plan for its employees. They said employees would leave Stockton for other cities offering retirement benefits through CalPERS....MORE

"Gold Drops Below $1200 On Heavy Volume, Silver Freefalls To Feb 2010 Lows"

We are still betting on $875 before the decline is done but, as we were saying before the recent action in the equity markets, silver is the easier call.* CME Dec. gold now $1198.30, silver $16.41.

From ZeroHedge(!):

...MORE

*See for example:

Oct. 3

"Technical Trading: Charts Don't Lie, No Sign Of A Bottom In Silver" (SLV)

Or:

Sept. 30

Gold, Silver Resume Decline

...We continue to believe the collapse in precious is the highest probability trade you'll find and that silver is the easier call of the two....

Sept. 19

Gold Down, Silver Collapses

Sept. 11

Chartology: "The Downside Target in Silver is Below $15"

As we've noted over the last few months when posting on gold and silver "...The easier call has been silver".

Sept. 10

Silver Bounces at Support For the Fourth Time In 14 Months

Sept.5

An Argument For $13 Silver and $1100 Gold

Sept. 2

Gold: "There's something wrong with our bloody ships today, Chatfield"

...The easier call has been silver:

Gold, Silver Continue Fearless Decline

From ZeroHedge(!):

It appears the machines forgot the shift in DST across the pond and started their European close flush a little early. Someone/something decided it was an opportune time to dump thousands of contracts of gold and silver futures this morning - clearly ignoring Alan Greenspan's advice. Gold ETF holdings are now back at levels first seen in April 2009. Gold's break below $1,200 likely brought some momentum chasers but Silver is in freefall, down over 5% and back to Feb 2010 lows. WTI Crude also broke below the crucial $81 level...

Gold

And Silver...

...MORE

*See for example:

Oct. 3

"Technical Trading: Charts Don't Lie, No Sign Of A Bottom In Silver" (SLV)

Or:

Sept. 30

Gold, Silver Resume Decline

...We continue to believe the collapse in precious is the highest probability trade you'll find and that silver is the easier call of the two....

Sept. 19

Gold Down, Silver Collapses

Sept. 11

Chartology: "The Downside Target in Silver is Below $15"

As we've noted over the last few months when posting on gold and silver "...The easier call has been silver".

Sept. 10

Silver Bounces at Support For the Fourth Time In 14 Months

Sept.5

An Argument For $13 Silver and $1100 Gold

Sept. 2

Gold: "There's something wrong with our bloody ships today, Chatfield"

...The easier call has been silver:

Gold, Silver Continue Fearless Decline

"Why the Next Financial Crisis Will Be Different"

From Knowledge@Wharton:

Major financial crises seem to rear their ugly head about every decade or so somewhere in the world, each different from the preceding one.

While there has been a lot of research on the causes of the latest global financial crisis that began in 2008 — and how to prevent it happening again — many experts argue that any new crisis will be different. Like the old saw noting that “generals always fight the last war,” there have been questions raised about whether or not researchers have focused enough on what might cause a future financial crisis, particularly with regard to central bank behavior.In an effort to avoid planning for the past when it comes to global financial crises, Wharton finance professor Franklin Allen has collaborated on a research paper titled “Financial Connections and Systemic Risk” with colleagues Ana Babus of the University of Cambridge and Elena Carletti of the European University Institute.Allen spoke with Knowledge@Wharton about his paper and what regulators need to be concerned about in order to avoid future crises.An edited transcript of the conversation follows.On what the research is about:The research I’m going to talk about is part of a long agenda. It has to do with the way that central banks and governments intervene in the economy.For the last 20 or 30 years, central banks have, by and large, focused on fighting inflation. After we had the big shocks in the 1970s, that was the major problem, and that’s what they’ve spent their main efforts doing. Some of the central banks, like the Federal Reserve, have a dual mandate. In addition to worrying about inflation, they also have to worry about unemployment.The way that this has been implemented in most countries, either explicitly or implicitly, is that the central bank has focused on inflation, and it’s usually granted formal independence from the government. The idea there is to stop it from lowering interest rates just before an election and making the economy boom, but then having inflation going up and so on. That was an idea that has been widely accepted for some time.Financial stability was in the mix, but it was usually regarded as something that was secondary — so that was dealt with either by the central bank or in many countries, such as the U.K. or Japan, by a separate financial services authority or FSA. They would deal with problems to make sure that there were no difficulties in transmitting monetary policy because banks were having problems. The way they did that was to stop banks taking risks, one by one. They would look at each bank and make sure that they weren’t doing risky things. The idea was that would stop any problems in the financial system.Fiscal policy was done separately by the treasury or the finance ministry, depending on the country. We could break up all these different parts of the way the government and central banks intervened, and they could all do their job separately. Now the problem is — what the crisis has shown — is that system didn’t work properly. What we need to do, I argue in this research, is to think carefully about how we should proceed going forward....MUCH MORE

Oil: There's Bearish and There's Betting On $50/Barrel Bearish

As to an eventual bottom our models, apparently backdooring Goldman's, guess at $70. Did I say guess?

From Reuters:

Fund manager Andurand says US oil could fall to $50/bbl

Oct. 21

Oil Sell-off, the Goldman View (XLE; ERY)

Oct. 22

Oil: Goldman Lowers Forecast, Brent and WTI Both Down

Oct. 27

Oil Shows Some Resiliance (today)

Oct. 28

More Goldman on Oil and a Correction on the Stimulative Effects of Oil Price Declines

Oct. 29

Godfather of the Bakken: "There Is No Oil Glut" (CLR)

From Reuters:

Fund manager Andurand says US oil could fall to $50/bbl

Pierre Andurand, one of the most respected and successful fund managers in the oil industry, said he believed U.S. light crude oil could fall as low as $50 per barrel.See also:

The U.S. benchmark oil price, also known as WTI, "will be volatile, but assuming no more supply disruptions, I think we can overshoot down to $50 a barrel," Andurand told Reuters on the sidelines of the Oil & Money conference on Wednesday.

"The move will mainly be in the front of the curve, but not just the first three months - the first six months or so," he said, adding that Brent would come down as well.

Andurand was co-founder of hedge fund BlueGold, which racked up record returns during the steep rise in oil prices in 2008 and the subsequent collapse in 2008-2009.

Bluegold's returns were lower in 2010, and the fund posted a loss the following year. Its co-founders eventually went their separate ways, and Andurand now runs a smaller hedge fund under his own name, which returned more than 25 percent last year and is up marginally year-to-date in 2014.

Andurand told the Oil and Money conference that he thought it unlikely that OPEC would cut production, even though current supply and demand trends suggested the market could be in a 2 million barrel-per-day surplus next year....MORE

Oct. 21

Oil Sell-off, the Goldman View (XLE; ERY)

Oct. 22

Oil: Goldman Lowers Forecast, Brent and WTI Both Down

Oct. 27

Oil Shows Some Resiliance (today)

Oct. 28

More Goldman on Oil and a Correction on the Stimulative Effects of Oil Price Declines

Oct. 29

Godfather of the Bakken: "There Is No Oil Glut" (CLR)

Bear Market: The Junior Gold Miners ETF Is Down 84.56% (GDXJ)

On Dec. 6, 2010 the Market Vectors Junior Gold Miners ETF traded at $179.44. Today it's at $27.70.

Not quite as bad as the 89% drop in the DJIA 1929-1932 but worse than Japan's 81.59% decline in the Nikkei, 1989-2008.

From Barron's:

Not quite as bad as the 89% drop in the DJIA 1929-1932 but worse than Japan's 81.59% decline in the Nikkei, 1989-2008.

From Barron's:

The Federal Reserve’s move to end its long-running bond-purchase program is slamming gold prices and shares of companies that mine precious metals.

Wednesday’s 4.3% swoon to $19.64 in the Market Vectors Gold Miners ETF (GDX) drives the ETF under $20 a share for the first time since October 2008, during the depths of the financial crisis.

The Global X Silver Miners ETF (SIL), falls 3.5% to close at $9.67, its lowest finish since its launch in April 2010.

The Market Vectors Junior Gold Miners ETF (GDXJ) was battered for a loss of 7.2%.

Miner stocks and gold prices extended their losses after the Fed’s announcement that it will wind down its “QEIII” program at the end of the month.

The SPDR Gold Shares (GLD) dropped 1.4% to $116.41.

The Fed’s move, while expected, was paired with a more upbeat assessment of the U.S. labor market. Those factor at once damp gold’s appeal versus income-generating assets, as a hedge against inflation and as a haven from economic uncertainty.......MORE

You Can Buy This Abandoned CT Town For Less Than A Brooklyn Apartment

From Gothamist:

This cute, abandoned town in Connecticut is basically Stars Hollow from Gilmore Girls, and it's currently being sold off at auction with a starting bid of $800,000. That's less than a brownstone in Brooklyn. That's less than some studio apartments here. It's a whole goddamn town! That's 62-acres, plus plenty of homes and General Store type structures that may or may not be haunted by cool, historic ghosts. Here's the deal:

Miss Patty's dance studio

This cute, abandoned town in Connecticut is basically Stars Hollow from Gilmore Girls, and it's currently being sold off at auction with a starting bid of $800,000. That's less than a brownstone in Brooklyn. That's less than some studio apartments here. It's a whole goddamn town! That's 62-acres, plus plenty of homes and General Store type structures that may or may not be haunted by cool, historic ghosts. Here's the deal:

"Why are they selling an entire town? Well, for starters, it’s been vacant for more than 20 years and through its history, has been abandoned not once, not twice, but three times Dating back to the 1830s, Johnsonville was once a thriving mill town and popular recreation spot set along the Moodus River, with amenities including a restaurant called the Red House Restaurant, a general store and a one-room schoolhouse.

Victorian and colonial-style houses with fireplaces and pillared porches were built by the families of the mill-owners where they lived contently up until the 1950s. All the historic buildings still remain. But then modernization crept up on the quaint community, work dried up and Johnsonville became a ghost town for the first time."...MORE

Exposed--An Explicit Full Frontal View of What's Really Going On In Big Cities: Money, Sex and Power

I intro'd Sunday's "San Francisco Is Smarter Than You Are" with:

Well, there must be something in the air regarding the reality of big cities and a bit of honesty among journos writing about the current zeitgeist. There are some realities that should probably be faced.

On Monday we linked to "RIP, NYC's Middle Class: Why Families are Being Pushed Away From the City" by New Geography.

Yesterday The Atlantic published "Why Middle-Class Americans Can't Afford to Live in Liberal Cities" which we originally threw in the link-vault to use as background on another story but which I'll copy out here for the Trulia link:

Blue America has a problem: Even after adjusting for income, left-leaning metros tend to have worse income inequality and less affordable housing.

Rich Households = Unaffordable Houses?

And probably more racist.And moved on about my business.

Depending on the source, San Francisco's population is between 6.0 and 6.6% black vs. 14.2% for the country as a whole. S.F. city and county use zoning laws to keep black folks out.

The same goes for Seattle and Portland. Someone should do a story on it....

Well, there must be something in the air regarding the reality of big cities and a bit of honesty among journos writing about the current zeitgeist. There are some realities that should probably be faced.

On Monday we linked to "RIP, NYC's Middle Class: Why Families are Being Pushed Away From the City" by New Geography.

Yesterday The Atlantic published "Why Middle-Class Americans Can't Afford to Live in Liberal Cities" which we originally threw in the link-vault to use as background on another story but which I'll copy out here for the Trulia link:

Blue America has a problem: Even after adjusting for income, left-leaning metros tend to have worse income inequality and less affordable housing.

On April 2, 2014, a protester in Oakland, California, mounted a Yahoo bus, climbed to the front of the roof, and vomited onto the top of the windshield.

If not the year's most persuasive act of dissent, it was certainly one of the most memorable demonstrations in the Bay Area, where residents have marched, blockaded, and retched in protest of San Francisco's economic inequality and unaffordable housing. The city's gaps—between rich and poor, between housing need and housing supply—have been duly catalogued. Even among American tech hubs, San Francisco stands alone with both the most expensive real estate and the fewest new construction permits per unit since 1990.

But San Francisco's problem is bigger than San Francisco. Across the country, rich, dense cities are struggling with affordable housing, to the considerable anguish of their middle class families.

Among the 100 largest U.S. metros, 63 percent of homes are "within reach" for a middle-class family, according to Trulia. But among the 20 richest U.S. metros, just 47 percent of homes are affordable, including a national low of 14 percent in San Francisco. The firm defined "within reach" as a for-sale home with a total monthly payment (including mortgage and taxes) less than 31 percent of the metro's median household income.

If you line up the country's 100 richest metros from 1 to 100, household affordability falls as household income rises, even after you consider that middle class families in richer cities have more income. [The graph below considers only the 25 richest US metros to keep city names moderately legible within the computer screen.]

Rich Households = Unaffordable Houses?

The line isn't smooth—and there are exceptions—but the relationship is clear: In general, richer cities have less affordable housing.But there's a second reason why San Francisco's problem is emblematic of a national story. Liberal cities seem to have the worst affordability crises, according to Trulia chief economist Jed Kolko.In a recent article, Kolko divided the largest cities into 32 “red" metros where Romney got more votes than Obama in 2012 (e.g. Houston), 40 “light-blue” markets where Obama won by fewer than 20 points (e.g. Austin), and 28 “dark-blue” metros where Obama won by more than 20 points (e.g. L.A., SF, NYC). Although all three housing groups faced similar declines in the recession and similar bounce-backs in the recovery, affordability remains a bigger problem in the bluest cities....MORE

Finally, and probably of most interest to our readers, this morning's FT Alphaville post:

Affordable housing and the legit big-city whinge

Someone should probably do a story, eh?

Affordable housing and the legit big-city whinge

When city-dwellers moan about their high cost of living, they often elicit the unsympathetic retort that they should shut up and praise the ghost of Jane Jacobs for the cultural vibrancy of their neighborhoods, the lucrative jobs, and the artisanal pizza.

Living in a great city is a consumption good, you whinging ninnies — you SHOULD have to pay for it! Why do you think you’re entitled to live wherever you want?

Hey, fair enough.

But there’s a difference between grumblings about $5 cinnamon macchiatos and the more useful outrage about meaningful troubles that can be solved — a difference between #firstworldproblems and the healthier expression of annoyed patriotism towards one’s habitat.

I like living here and want to keep living here, which is why the problems I complain about aren’t enough to push me out. I’d rather stick around and see the problems solved. But those problems suck, so let’s start doing something about them.

To complain that rents, for instance, could and should be lower isn’t always a sign of yuppie entitlement. Nor is it mutually exclusive with appreciating the wonderful aspects of city life. Sometimes the gripe really is legitimate.*

A doorstopping thud of a McKinsey report dropped last week, canvassing the issue of insufficient affordable housing in cities throughout the world.

The biggest contributing problem is idle land, which can be freed for development with fairly straightforward, but always politically intractable, ideas. Amend anti-density zoning regulations. Loosen bureaucratic restrictions on new construction. Allow more building on government-owned land, or privatise it. Eliminate rent controls where possible.

The report included a useful, brief case study of New York City that makes plain the effects of insufficient affordable housing on its workers, a problem shared by so many of the world’s biggest cities.

A few excerpts follow, and we’ve bolded the highlights if you want to race through it:

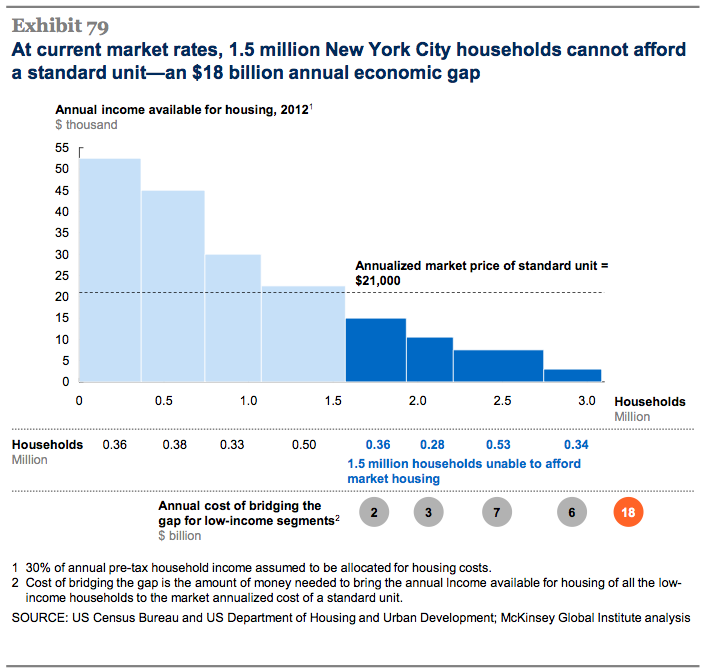

We estimate that half of New York households cannot afford basic housing using 30 percent of their income. In New York City, median household income is $51,000. If we define low-income households as those earning 80 percent of the median, 1.2 million households (of about 3.1 million) would be classified low- income. …

We estimate that the affordability gap is about $18 billion per year (Exhibit 79). This represents about 4 percent of New York City’s GDP.

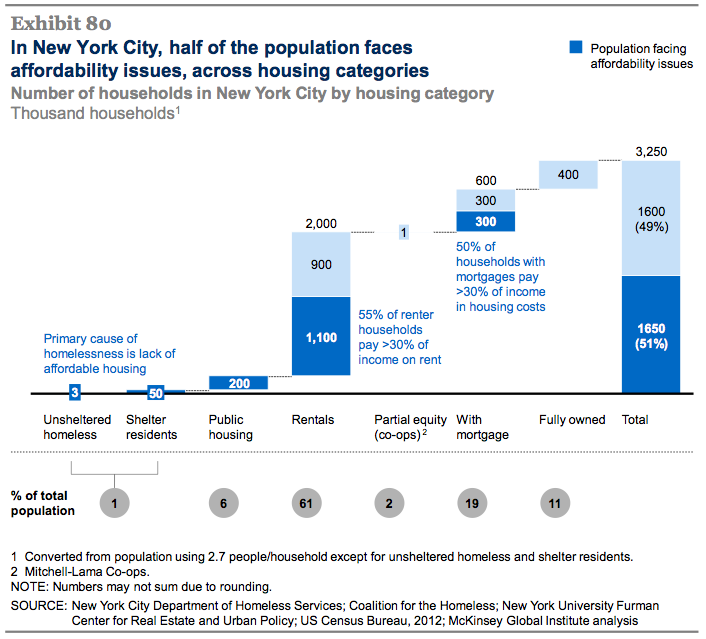

This ties well with current statistics, about 1.6 million households in New York City face housing challenges across different housing categories (Exhibit 80). About 55 percent of renters and 50 percent of households with mortgages are financially stretched, paying more than 30 percent of income on housing costs.

Housing issues affect low-income households disproportionately: 89 percent of households earning less than 30 percent of area median income are financially stretched by housing costs. Of households earning 30 to 50 percent of area median income, 83 percent are financially stretched by housing costs, and 66 percent of households earning 50 to 80 percent of area median income pay more than 30 percent of income for housing.......MUCH MORE

Someone should probably do a story, eh?

Wednesday, October 29, 2014

It Appears There Is A Volcano Threat In Japan That Could Wipe Out The Country

Didn't have this in the models. Have a big earthquake, not this.

From ENE Energy News:

HT: ZeroHedge

From ENE Energy News:

Experts warn of volcano destroying Japan at any moment, causing nation’s extinction — Millions buried by lava in minutes, ‘hopeless’ for 120,000,000 people — Reactors would be devastated and spread nuclear waste worldwide — Gov’t: Volcano near nuke plant is shaking, tremor 7 minutes long… ‘Stay away’ — Increased eruption risk due to 3/11 quake...MORE

Wall St Journal, Oct. 23, 2014 (emphasis added): One major volcanic eruption could make Japan “extinct,” a study by experts at Kobe University warns… “We should be aware… It wouldn’t be a surprise if such gigantic eruption were to take place at any moment.”

Japan Times, Oct. 24, 2014: Colossal volcanic eruption could destroy Japan at any time: study — Japan could be nearly destroyed by a volcanic eruption over the next century that would put nearly all of its population of 127 million people at risk… “It is not an overstatement to say that a colossal volcanic eruption would leave Japan extinct as a country,” Kobe University earth sciences professor Yoshiyuki Tatsumi and associate professor Keiko Suzuki said… A disaster on Kyushu… would see an area with 7 million people buried by flows of lava and molten rock in just two hours [and] making nearly the entire country “unlivable”… It would be “hopeless” trying to save about 120 million…

HT: ZeroHedge

"Economists React to the Fed Statement: ‘Surprisingly Hawkish’"

From Real Time Economics:

Here's commentary from junior gold miners on how hawkish the statement was:

The Federal Reserve on Wednesday announced the end of its long-running bond-buying program. The central bank also stuck to an assurance that short-term interest rates would remain near zero for a “considerable time.” Economists largely expected the end of the Fed’s third round of quantitative easing, as it was known. But many found the statement more “hawkish,” easing off concerns about progress in the labor market....MORE

Here’s what some economists are saying:

“In short, [the Fed's statement was] largely as expected, but, if anything, a more positive tone, at least on the labor market. We expect tightening will start by June 2015, but, of course, that will depend on the data. For now, there is no urgency for officials to use the statement to signal an imminent move. Bond yields have risen a few basis points since the statement was released.” –Jim O’Sullivan, High Frequency Economics

“As expected, the Fed today announced an end its third round of large-scale asset purchases (aka QE3). Slightly less expected, however, is that despite the recent market volatility, the statement issued after the FOMC meeting was, if anything, more hawkish…On balance, the Fed believes it is getting closer to meeting the full employment side of its mandate, while it is not necessarily convinced it is losing ground in meeting the price stability side of its mandate. We would say that was, if anything, a slightly hawkish shift. It’s also perhaps telling that it was the dovish Narayana Kocherlakota who dissented at this vote, whereas in previous FOMC meetings this year it is the hawks who dissented.” –Paul Ashworth, Capital Economics

“After getting knocked off its mark by recent equity market volatility, the FOMC has apparently returned to form, namely a slow but steady shift towards a more hawkish trajectory on policy. What better way, in fact, to get the equity market to rally in the face of eventually higher interest rates than to be more bullish on growth and shifting the focus of potential action from labor to now waiting for inflation. The FOMC also dropped any mention of fiscal policy being a drag on growth. Barring any unforeseen slowdowns, which the Fed never sees, we are now simply left to wait around for signals core inflation is on its way back towards 2%. Once signaled, the Fed is ready to shorten ‘considerable time’ to no time at all.” –Steve Blitz, ITG Investment Research

Here's commentary from junior gold miners on how hawkish the statement was:

"The Opportunity in Weak Commodity Prices"

That is Barron's magazine's headline, not ours.

We see commodities as tactical trading vehicles, not investments and see the larger macro picture as being shaped by a disinflationary-to-deflationary bias.

On the other hand Barron's has been around longer than I so they may be right with the six "Buy Oil" articles they've run in the last week.

But I'm doubting it.

From Barron's 'Wall Street's Best Minds' feature:

We see commodities as tactical trading vehicles, not investments and see the larger macro picture as being shaped by a disinflationary-to-deflationary bias.

On the other hand Barron's has been around longer than I so they may be right with the six "Buy Oil" articles they've run in the last week.

But I'm doubting it.

From Barron's 'Wall Street's Best Minds' feature:

Wells Fargo urges investors to use price pullbacks to invest in energy, metals, and agriculture.Oddly enough (or maybe not that odd) the disinflationary backdrop is actually a positive for the overall market whose best real returns usually occur in a 0-2% inflation regime.

Commodity markets – especially for crude oil -- continue to face headwinds from excess supply and uncertainties about divergent monetary policies. But nascent positive trends give commodity markets a more balanced outlook, in our view.Looking into the end of the year and into 2015, we feel investors should use the recent price pullbacks to take commodity allocations towards their long-term target allocations. We recommend an allocation split evenly between a broadly diversified position and another in energy (crude oil, refined products, and natural gas).For the past two months, investor anticipation of new and large monetary policy stimulus in Europe and Japan has rallied the U.S. dollar and raised the cost of raw materials in local currencies. In addition, worries about excess commodity supplies accompany slipping global economic data.We think the impact of these factors is overdone. During the coming weeks, expectations for dollar strength should moderate. The excess supply problem also seems to be resolving, especially in base metals, where miners are cutting production quickly and global markets are gradually rebalancing.The crude oil market is particularly concerned about excess oil supply and the strong U.S. dollar. After touching $115/barrel in June, the price of benchmark European Brent crude oil fell by $35/barrel by early October, finishing below $100 for the first time since political turmoil erupted in Egypt in 2011. The decline seems unjustified based on our supply and demand outlook, and we advise investors to be careful about assuming $80/barrel oil prices are here to stay. For example, the last $12 of oil price declines came as the dollar also declined this month.It is also risky to assume that OPEC and U.S. supply will become permanent sources of excess supply. Extra U.S. production does not add much to new excess supply. If OPEC would only cut by 500,000 barrels per day (1.5% of their daily output), it could effectively erase the contribution of this year’s gain in U.S. production. So why doesn’t OPEC cut? For perspective, oil prices are still in their four-year trading range of $80-$120 per barrel, and the collapse from $90 came quickly – possibly too quickly for OPEC’s factious members to form a consensus. Since the mid-1980s, OPEC has tried to steady oil prices, and potential price spikes are material risks – for example: if the Libyan production recovery falters and ISIS threatens large production facilities.Our monthly review of the major commodity sectors follows next:Energy: Energy prices continue to drag on concerns of excess crude oil supply and weak seasonal demand. However, seasonal petroleum and natural gas demand is poised to pick up, and consumption is still growing globally -- especially from strong Chinese automobile sales -- and should accelerate with improved global economic growth next year. We revised lower our 2014 year-end target for West Texas Intermediate crude oil to $90-$95 per barrel to account for temporary uncertainty and expect a rebound into year-end, followed by single-digit 2015 returns.Base metals: Base metals prices have fallen with the rising U.S. dollar, and weakening global manufacturing demand and falling real estate prices in China have sapped the construction consumption of industrial metals. However, 2015 global demand prospects look better, and miners are slashing output faster than we previously thought they would.Precious metals: Demand for platinum and palladium for catalytic converters has supported these markets somewhat, but no supply-demand rebalance is likely for gold and silver, which remain vulnerable to potentially higher U.S. interest rates sooner rather than later. Investors should use any gold or silver price rebound to reallocate into a diversified commodity position.Grains: The wet weather in the U.S. Midwest has slowed the harvest and boosted the soil conditions for wheat planting. As a further negative for price, robust foreign demand for corn and soybeans may fail to counteract excess supply and the strong dollar and put U.S. farmers at a competitive disadvantage....MORE

"Farmland Partners buys back shares, 3 months after selling them" (FPI)

From Agrimoney:

Farmland Partners revealed a share buyback only three months after raising $46.5m from shareholders, saying the turnaround reflected the unwarranted cheapness of the stock.The land investment group revealed a $10m stock repurchase programme, to be executed "from time to time, in amounts and prices as the company deems appropriate".The buyback "demonstrates our confidence in our ability to generate returns that are not reflected by our current stock price", said Paul Pittman, the group's founder and chief executive."Repurchasing our shares is a prudent use of our cash and a significant value creation opportunity for the company's stockholders."Farmland Partners in July sold 3.71m shares at $12.50 a share to raise cash for a land acquisition warchest.The shares closed last night at $10.36, representing a drop of 17% on the July sale price, although they rose 3.3% on Wednesday to $10.70 in lunchtime deals in New York.Soaring costsThe announcement came hours after Farmland Partners unveiled for the July-to-September period, its first full quarter since listing in April, earnings of $34,805, down from $169,418 a year before.While revenues more than doubled to $1.19m, a reflection of a spending spree which is on track to lift its portfolio above 38,000 acres, costs soared too, with general and administrative expenses rocketing above $645,000 from $7,873 a year before, a reflecting of its listing and more active operation....MORE

Grantham Mayo’s James Montier Calls Shareholder Value Maximization “The Dumbest Idea In The World”:

I can think of a few things dumber but let's roll with Jim on this.

From the CFA Institute:

Shareholder Value Maximization: The World’s Dumbest Idea?

From the CFA Institute:

Shareholder Value Maximization: The World’s Dumbest Idea?

If you agree with the economist John Maynard Keynes that “ideas shape the course of history,” then you ought to agree that the history of modern business and finance has been shaped by one influential idea: that the job of a company’s management is to maximize shareholder value. But according to James Montier, a distinguished investment professional and behavioural finance writer, shareholder value maximization is “a bad idea.” He believes it has not added any value for shareholders and has contributed to such major economic and social problems as short-termism and rising inequality.

Montier made his case against shareholder value maximization when delivering the closing keynote address at the 2014 European Investment Conference in London, a video of which can be viewed below. In his characteristic iconoclastic style with a generous use of ironic humour, Montier labeled shareholder value maximization, the way Jack Welch, the former CEO of GE, had once described it in 2009, as “the dumbest idea in the world.”

An Academic Opinion without Much Evidence

Montier said that the idea of shareholder value maximization didn’t come from businesses but rather originated as an opinion in academia and was unsupported by much evidence. It is most directly traced to an op-ed written by economist Milton Friedman in 1970. Over the years, academic research papers on the subject, such as those by Michael C. Jensen and William H. Meckling (PDF) and Jensen and Kevin J. Murphy (PDF), have made it inseparable from the alignment of incentives. That is, top management of companies should be offered financial incentives (e.g., stock ownership and call options) to align their interest with maximizing the stock price.

The idea of shareholder value and incentives then worked its way into practice. Montier gave the example of Business Roundtable (BRT), an association of CEOs of major US companies. He said that in 1981, the mission of BRT referred to making quality goods and services, earning a profit, and building the economy, but by 1997, it became firmly focused on shareholder value.

Failing Shareholders

Montier claimed that shareholder value maximization has failed the shareholders — its intended beneficiaries. Despite enormous increases in compensation of CEOs and a rising proportion of financial incentives through stock ownership and options, shareholders are not better off. To illustrate this point with a case example, Montier compared the return performance of IBM, which switched its focus to shareholder value maximization, to that of Johnson & Johnson, which retained its credo (PDF) emphasizing responsibility to customers, employees, and communities. Montier showed that during 1971–2013, the stock of Johnson & Johnson had indeed outperformed that of IBM....MORE

North Korea's Kim Jong Un Executes 10 Party Official for Watching Soap Operas, Graft

From the Inquisitr:

North Korean leader Kim Jong Un ordered the execution of 10 officials for charges ranging from watching soap operas to graft.

Bloomberg reports that it appears that Kim Jong Un is seeking to erase the remaining influence of his dead uncle by executing about 10 senior Workers’ Party officials on charges from graft to watching South Korean soap operas. The reports come from an aide to a South Korean lawmaker. The deaths, which occurred by firing squad, are likely part of Kim’s latest round of purges said Lim Dae Sung, an aide to ruling South Korean Saenuri Party lawmaker Lee Cheol Woo, who attended a briefing at the National Intelligence Service yesterday in Seoul. Kim had his uncle, Jang Song Thaek, killed in December last year....MORE

“Kim Jong-un is trying to establish absolute power and strengthen his regime with public punishments. However, frequent purges can create side effects.”

Gold Closes Near Two-Week Low as Oil Hits a Four Day High

Children, do not try this at home. I'm not kidding.

By the time you are calling opposite moves in monetary commodities (what, you've never heard of the BTU standard?) you are probably beyond hope and riding the fast train to loony land:

Gold Futures Closes Near Two-Week Low on Fed Speculation

Also at Bloomberg:

WTI Crude Rises to Four-Day High

WTI $82.46 up $1.04

Dec. gold $1223.3 down $6.1

By the time you are calling opposite moves in monetary commodities (what, you've never heard of the BTU standard?) you are probably beyond hope and riding the fast train to loony land:

Oct. 16-"(just kidding, a gold short at $1240 sounds lovely) "From Bloomberg:

Oct. 27-"...WTI is now only down 26 cents from today's settle, at $80.74. We're going lower but you may see a bit of a short squeeze this week."

Gold Futures Closes Near Two-Week Low on Fed Speculation

Also at Bloomberg:

WTI Crude Rises to Four-Day High

WTI $82.46 up $1.04

Dec. gold $1223.3 down $6.1

Godfather of the Bakken: "There Is No Oil Glut" (CLR)

Whatevs.

From CNBC:

Of course if he loses it it means that the loot wasn't really his to lose, that the wealth is a marital asset and... jeez, I see no upside to my prattling on about divorce law.

From CNBC:

Oil titan Harold Hamm told CNBC on Tuesday: Don't believe the hype. "There's not a glut in the market at all."Mr. Hamm is one of the 50 wealthiest people on the planet which is a good thing as, possibly as early as today, he is about to lose between $7 and $9 billion dollars in the most expensive divorce in U.S. history.

The billionaire founder of Continental Resources took issue with the reason mostly given for crude's slide to multi-year lows, and said he's not cutting production yet. But even if he did, he said, "You don't cap producing wells. What you do is cut back on new drilling."

"What we see here is people projecting next year that we might see [oversupply]," he said in a "Squawk Box" interview. "It would have to be a perfect world to see that. I, frankly, don't believe that's going to happen."

He disputed contentions from Goldman Sachs, which on Sunday predicted oil at $70 a barrel in the U.S. in the second quarter because of oversupply. West Texas Intermediate (WTI) crude was trading $81 in early trading Tuesday after dropping below $80 Monday for the first time since early summer of 2012....MORE

Of course if he loses it it means that the loot wasn't really his to lose, that the wealth is a marital asset and... jeez, I see no upside to my prattling on about divorce law.

WSJ Oct. 29, 1929: "Market Orderly In Record Drop"

"Continued Operation of Banker's Pool Prevents Repetition of Thursday's Hysteria"

From the Wall Street Journal's WSJ blog:

Oct. 28-29, 1929: Stock Crash

The 1929 crash that ushered in the Great Depression included Black Monday and Black Tuesday, during which the Dow Jones Industrial Average fell 13% and 12% back-to-back. Investors after Monday’s slide were assured that “banking interests” were supporting the market, “with a hand on the throttle.” Today in WSJ History.......MORE

Bundesbank Paper Flags Risks of Ultralow Rates to German Insurers

No kidding. Second only to the fact that the insurers have probably screwed up the longevity numbers à la the British,* is the fear they won't earn enough to meet the obligations they have incurred.

From MoneyBeat;

Potential flaw in UK mortality data may impact longevity re/insurers

From MoneyBeat;

A dozen German life insurance companies wouldn’t be sufficiently funded to face even a mild stress scenario in which German government bond yields decline further and stay super low, according to a paper released Monday by Germany’s central bank.*See for example at Artemis:

“The present analysis shows that a persistent low-interest-rate environment harbors a potential risk to the stability of the life insurance segment,” a pair of Bundesbank economists wrote in a study looking at year-end 2012 data from 85 German life insurers.

The study included what the authors called a “mild stress scenario” in which German Bund yields stayed at levels that have persisted in Japan “for an extended period.” Twelve of the 85 German life insurers wouldn’t be able to meet their own funding requirements by 2023 under this scenario, the authors found. The study didn’t identify individual companies....MORE

Potential flaw in UK mortality data may impact longevity re/insurers

Tuesday, October 28, 2014

The Timeless Allure of Stock-Market Timers

Dennis Gartman is not our favorite prognosticator. I've said in the past that Gartman will lose you money in equities* ("Warren Buffett is an idiot")

but in commodities, especially ags, but also commodities in general, he

exhibits what computer modelers call forecast skill and can generate

excess returns.

From Barron's Read This Spike That column:

August 2012

Gartman Rolling Out Four Gold ETF's Including A Fund-of-Funds to Buy the Other Three

October 2010

"The curious incident of the 300m bushels of corn" (BRK.B) CORN

Update on the Fisher/Gartman Volatility ETN's (ONN; OFF)

Following up on last week's "Fisher/Gartman Introduce Volatility ETN's; Short 'em Both (ONN; OFF)".

November 2011

Oh Now What? "Huge asteroid headed for close encounter with Earth"

From Barron's Read This Spike That column:

Twelve days ago, as the broader U.S. stock market was in the midst of its first sharp decline in years, popular newsletter editor Dennis Gartman appeared on a CNBC show and advised viewers to prepare for a bear market.“You stay in cash and you stay in short-term bonds and you don’t move out,” Gartman advised viewers before adding “this is the start of a bear market, and it could last for several more months I’m afraid.”But stocks quickly turned around and began to move toward the heights last seen in September. A chastened Gartman admitted late last week on another CNBC show that his bear-market call was all wrong. However, he’s still not willing to go long, instead maintaining a “neutral” position on the market as a whole, according to a CNBC.com report on Gartman’s rapid change of heart.Asked by CNBC what he missed about the current character of the market, he replied “I’m not sure what I missed. I really don’t know….This is the type of volatility that is absolutely beyond my ken. I’ve only been at this for 40-some years, so I’m relatively new to it. But quite honestly, I’ve never seen anything like the last two weeks.”While the volatility may have been beyond Gartman’s ken, it didn’t humble him enough to beg off the game of predicting where the stock market is heading. At least he hasn’t met the fate that Dante reserved for soothsayers in his classic 14th century work, The Divine Comedy: Those who attempt to divine the future should have their heads twisted around and be forced to walk backwards for eternity.But it would be wrong to just pick on Gartman. He is just one of a long list of market pundits who attempt to do what many respected investment minds argue is impossible—predict with some degree of confidence where stocks as a whole are heading and then often recommend a sharp shift in one’s asset allocation to play a bull or bear scenario....MORE

I've no idea where he was going with "I’ve only been at this for

40-some years, so I’m relatively new to it."

If he meant to be funny he missed, badly.

Some other Gartman posts:

We have very little patience with guys like Gartman.January 2013

Here's the "since inception" chart for the Horizons Gartman ETF:

You'll note the ETF underperformed the S&P 500 from day 1 and only got worse from there.

In June 2009 we had:

Last week MarketBeat had a post "Gartman: ‘Warren Buffett Is an Idiot’" that relayed Mr. Gartman's radio comment. I had a comment [of course you did -ed] as did 57 other MarketBeat readers. The post is still at the top of their most read list. 10:47 am June 19, 2009

A few days later he backtracked:

Gartman: Warren Buffett Isn't An "Idiot" .. But He Allowed "Inexcusable" Losses (BRK.A)

and a few weeks later:

Dennis Gartman is an Idiot (BRK.B; DXY)

On June 18, 2009 Dennis Gartman said "Warren Buffett is an idiot"* and announced to the world that he was short Berkshire Hathaway. Neither of these were very smart moves. As the chart below shows, Berkshire is up 40-odd percent since Gartman's call.DJIA 13,132.73

In fact BRK.b has outperformed the S&P 2:1 in the intervening months....

S&P 1,409.28

Gartman Rolling Out Four Gold ETF's Including A Fund-of-Funds to Buy the Other Three

October 2010

"The curious incident of the 300m bushels of corn" (BRK.B) CORN

Long time readers know that I've had some quibbles with Mr. Gartman (Dennis Gartman is an Idiot (BRK.B; DXY) regarding his understanding of Berkshire Hathaway and it's chairman.December 2011

(See links and chart after the jump)

Then there was his EUR/USD commentary. June 1 with the Euro at 1.22 he said it was "almost certainly" going under $1.20. Duh

We'd been making the same call since Nov. 2009 at $1.50.

The buck strengthened to $1.1877 and reversed, I think it was June 4.

On June 18 of this year he called the Euro doomed. That may be but it had bottomed two weeks earlier and was on its way to kicking Yankee butt.

Hmmm...

On the other hand he is a student of the grains. Here's FT Alphaville...

Update on the Fisher/Gartman Volatility ETN's (ONN; OFF)

November 2011

Oh Now What? "Huge asteroid headed for close encounter with Earth"

So there I was, shooting off my mouth over at MarketBeat:There's more but I'm sure gentle reader has things to do.

Stock Market Has Topped: Gartman

...“The investment objective of the Horizons AlphaPro Gartman ETF (the “ETF”) is to provide investors with the opportunity for capital appreciation through exposure to the investment strategies of The Gartman Letter, L.C. (“Gartman”), founded by Dennis Gartman….”And now this, via the Chicago Tribune:

The fund launched at the beginning of the big bull run in March, 2009, at $10.00 It’s at $8.56, down 14.4% since the launch. The S&P 500 is up 71.5%. This baby is one anti-correlated asset. The Gartman fund has recently begun to turn up which probably means there is an asteroid headed our way.”...

CAPE CANAVERAL, Fla (Reuters) - A huge asteroid will pass closer to Earth than the moon Tuesday, giving scientists a rare chance for study without having to go through the time and expense of launching a probe, officials said....

If the west wants to hurt Putin, could Saudi Arabia do its dirty work?

Just a reminder.

From The Guardian:

Wednesday 26 March 2014 12.21 EDT

From The Guardian:

Wednesday 26 March 2014 12.21 EDT

Europe depends on Russian oil and gas exports, so an embargo may not be practical. But there is another way to apply pressure

Russia is vulnerable to sanctions. Economic weakness caused the collapse of the Soviet Union a quarter of a century ago and – the self-enrichment of the oligarchs apart – not much has changed since. Energy exports to the rest of the world pay for imports of machines and consumer goods. The population is ageing and there has been little industrial diversification.

So, if the west really wants to hurt Vladimir Putin it should slap an oil embargo on Russia similar to that used against Iran. A drop in oil exports would mean Russia would not be able to afford German cars, French wine and Italian designer clothes.

It's not quite that simple. Europe is dependent on Russia for its energy supplies, so an embargo might be a classic example of shooting oneself in the foot, especially if Russia finds a way of sending its oil and gas east to energy-hungry China.

This, though, could not happen overnight, so what the west really needs is a way of hurting Putin that does not hurt itself. Neil Barnett of the Centre for Policy Studies says there is a way of doing this: persuade Saudi Arabia to do the dirty work.

There is a precedent. Angered by the Soviet invasion of Afghanistan in 1979, the Saudis turned on the oil taps, driving down the global price of crude until it reached $20 a barrel (in today's prices) in the mid-1980s. It would take a much smaller drop in the cost of oil – from $107 a barrel currently to somewhere south of $90 a barrel – to cause Russia severe financial and economic damage....MORE

Art: "Caravaggio and the Experts: Science v. Connoisseurs"

From Art Market Monitor:

It has been a busy week for Caravaggio experts. A long-simmering court case involving the Card Sharps, above, is finally reaching court in London just as a connoisseur is claiming to have found the true original to the painters Mary Magdalene in Ecstasy, according to The Guardian:...MORE

Mina Gregori, 90, president of the Roberto Longhi foundation of art history studies in Florence and author of several books on the baroque painter, said she was 100% sure she had found the original Mary Magdalene in Ecstasy.

“I have become a connoisseur,” she said. “And I know a Caravaggio when I see one.”

A number of elements had combined to give her complete certainty, she said, that the oil on canvas she was presented with this year was the real thing.

There are several different versions of the Mary Magdalene in Ecstasy, and until now the one thought most likely by art historians to be the 1606 original was lying in a private collection in Rome....

"Matt Taibbi Disappears From Omidyar’s First Look Media"

From New York Magazine:

Matt Taibbi, the star magazine writer hired earlier this year to start a satirical website for billionaire Pierre Omidyar's First Look Media, is on a leave of absence from the company after disagreements with higher-ups inside Omidyar's organization, a source close to First Look confirmed today.

Taibbi's abrupt disappearance from the company's Fifth Avenue headquarters has cast doubt on the fate of his highly anticipated digital publication, reportedly to be called Racket, which First Look executives had previously said would launch sometime this autumn.

When he was hired, amid much fanfare, Taibbi's website was meant to be the second in an envisioned fleet of titles to be published by First Look, an ambitious digital journalism company funded by Omidyar, the founder of eBay and one of the richest tech moguls in America. Like its counterpart the Intercept, launched earlier this year by Glenn Greenwald and others to pursue investigations of NSA surveillance and the intelligence world, it was a venture centered around a brand-name polemicist without much management experience. Prior to joining First Look, Taibbi made his name by gleefully skewering fat targets for Rolling Stone — most famously, he described Goldman Sachs as "a great vampire squid wrapped around the face of humanity" — and he said at the time of his departure that he was lured away by the chance to lampoon the financial industry in the "simultaneously funny and satirical voice" associated with the legendary magazine Spy. Over the succeeding months, the mission of the publication broadened to encompass political satire as well, and it brought on a number of high-profile names from the New York digital scene, including deputy editor Alex Pareene, formerly of Salon; Laura Dawn, a digital video producer who formerly worked with Moveon.org; and Edith Zimmerman, founding editor of the Hairpin.

"Journalists should be dark, funny, mean people," Taibbi told New York in an interview in March. "It's appropriate for their antagonistic, adversarial role."...MORE

Subscribe to:

Posts (Atom)

As donzoab points out, free cash flow is key. It allows you to play in the big leagues.

That and being able to cut opportunistic deals with a single phone call to Charlie or Sokol.

When Gartman takes Goldman as deep as Warren did, 10% money and warrents! (in the money $1.1 Bil.) I’ll pay attention to his comments on BRK.