From Bloomberg:

The U.S. shale patch is facing a shakeout as drillers struggle to keep pace with the relentless spending needed to get oil and gas out of the ground.Possibly also of interest:

Shale debt has almost doubled over the last four years while revenue has gained just 5.6 percent, according to a Bloomberg News analysis of 61 shale drillers. A dozen of those wildcatters are spending at least 10 percent of their sales on interest compared with Exxon Mobil Corp.’s 0.1 percent.

“The list of companies that are financially stressed is considerable,” said Benjamin Dell, managing partner of Kimmeridge Energy, a New York-based alternative asset manager focused on energy. “Not everyone is going to survive. We’ve seen it before.”

Some investors are already bailing out. On May 23, Loews Corp. (L), the holding company run by New York’s Tisch family, said it is weighing the sale of HighMount Exploration & Production LLC, its oil and natural gas subsidiary, at a loss.

HighMount lost $20 million in the first three months of the year, after being unprofitable in 2013 and 2012, Loews said it its financial reports. As with much of the industry, HighMount has shifted its focus to oil after natural gas prices plunged and has struggled to find sites worth developing, company records show.

Mary Skafidas, a spokeswoman for Loews, declined comment.

In a measure of the shale industry’s financial burden, debt hit $163.6 billion in the first quarter, according to company records compiled by Bloomberg on 61 exploration and production companies that target oil and natural gas trapped in deep underground layers of rock. And companies including Forest Oil Corp. (FST), Goodrich Petroleum Corp. (GDP) and Quicksilver Resources Inc. (KWK) racked up interest expense of more than 20 percent.

Production Declines

Quicksilver acknowledges the company is over-leveraged, said David Erdman, a spokesman for Quicksilver. The company’s interest expense equaled almost 45 percent of revenue in the first quarter. “We have taken concrete measures to reduce debt,” he said.

Drillers are caught in a bind. They must keep borrowing to pay for exploration needed to offset the steep production declines typical of shale wells. At the same time, investors have been pushing companies to cut back. Spending tumbled at 26 of the 61 firms examined. For companies that can’t afford to keep drilling, less oil coming out means less money coming in, accelerating the financial tailspin.

Interest Expenses

“Interest expenses are rising,” said Virendra Chauhan, an oil analyst with Energy Aspects in London. “The risk for shale producers is that because of the production decline rates, you constantly have elevated capital expenditures.”

Chauhan wrote a report last year titled “The Other Tale of Shale” that showed interest expenses are gobbling up a growing share of revenue at 35 companies he studied. Interest expense for the 61 companies examined by Bloomberg totalled almost $2 billion in the first quarter, 4.1 percent of revenue, up from 2.3 percent four years ago.

The drilling spree boosted U.S. oil production to 8.4 million barrels a day, 16 percent more than a year ago and the highest since 1986. Growth has been driven by advances in horizontal drilling and hydraulic fracturing, or fracking, which unlocked crude and natural gas trapped in formations like North Dakota’s Bakken shale or the Marcellus in the U.S. northeast....MORE

"US Shale Gas Won't Last Ten Years"

This is an extreme view, probably promulgated to sell a book, but it highlights the problem with decline rates.Natural Gas: The Astounding Production Decline Rates of Shale Wells

There are some plays which are uneconomic over the life of the well (more money in than out) but which are drilled anyway because of the quick cash flow which can be used as the basis for another round of debt or equity.

Stripped of all the hype, there are E&P companies that are basically Ponzi schemes but with a tail long enough that the miscreants will probably get away with it....

And one of the sharper analysts on oil:

Bernstein Research: "America’s shale oil bonanza won’t lead to an era of cheap energy"

Bernstein on Bakken Decline Rates and Estimated Ultimate Recovery (CLR; EOG; KOG; NFX)

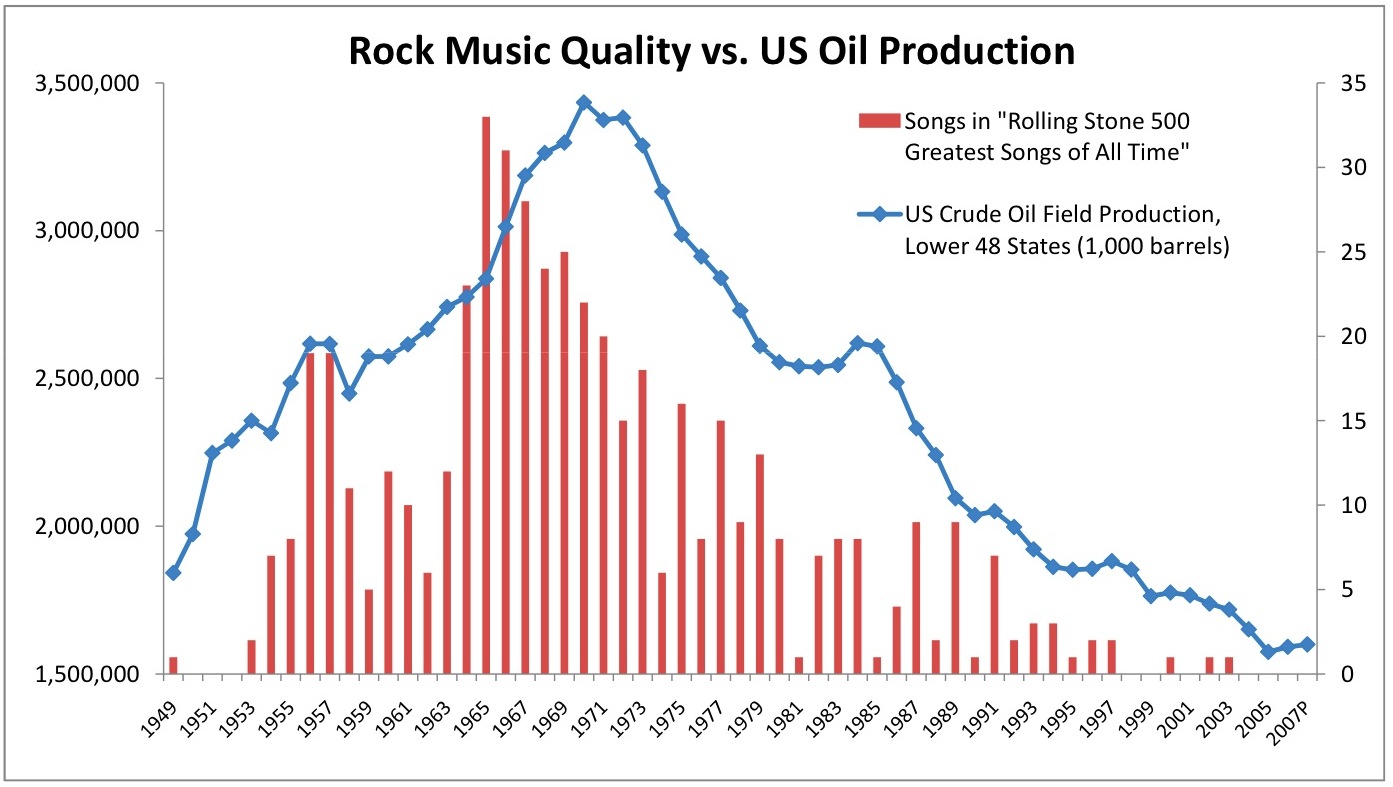

And finally, something else to be aware of from Overthinking It via the Houston Chronicle and our 2009 post "Natural Gas: 'The Hubbert's Peak theory of rock n' roll' and 'Do these LNG export slowdowns change the balance?'":

(Sources: Rolling Stone Magazine, US Department of Energy)