If ever there was a case of “recession fatigue” it was Europe in the summer of 2013. There has been nothing but optimism from the Continent throughout, and sunshine purportedly reflected a burgeoning recovery that was far more broadly situated than the vagaries of Germany’s export economy. Spain and Italy were to be among those that could proudly proclaim, as Bernanke once did in 2008, that the worst was behind. France, it has been suggested, will avoid going the full PIIGS route after all.

To some varying extent, last week’s rate cut by the ECB ran counter to those sunny narratives. As has been the case since 2007, it is perfectly clear that mainstream commentary understands very little of the mechanics of European monetary systems, so it was no surprise that very little insight was provided into the rate decision itself. It’s not just simply case where the ECB is cutting rates to “stimulate”, or even guard against economic retrenchment. That is the American version of central banking and it is not really portable.

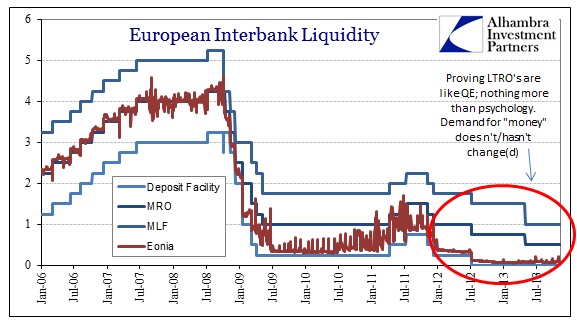

The complex ECB/NCB system involves a rate “corridor.” The ECB left the deposit rate, the floor, at 0%, where it has been stuck since the middle of 2012. Instead, the ECB “narrowed” the monetary policy rate corridor for the second time this year. Part of this relates to the unending fragmentation of the liquidity system across the geographic divide. For all the talk of recovery, the monetary system is still very much divided by PIIGS v. Core.

We will know that there is an actual recovery in Europe once Eonia starts “behaving” properly (for a primer in ECB/NCB mechanics, including to what Eonia, MRO/MLF rates pertain, go here). Since the major crisis in late 2011, after all the LTRO’s and monetary distortions, Eonia still shows a liquidity system very much in doubt about prospects for the peripheral financials. In other words, the fact that Eonia continues to trade below its “normal” place attached and around the MRO midpoint shows that financial firms are very much still in the pessimistic camp....MUCH MORECompare/contrast with Huh "The Fed's objective is to destroy the demand for cash".

See also Coppola Comment: "About that ECB interest rate cut"