From ZeroHedge:

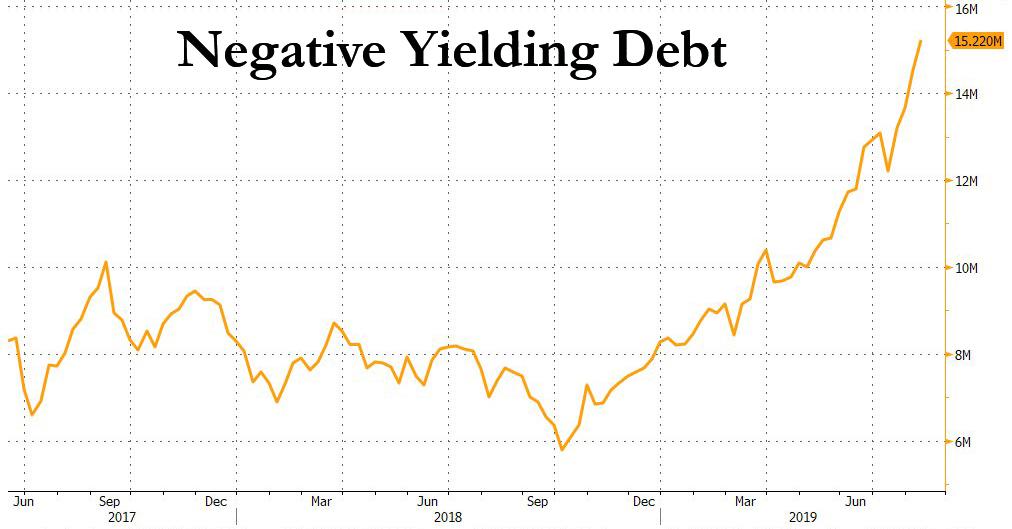

Having repeatedly praised Albert Edwards in the past month for correctly predicting the creeping ice age that has now sent $15.2 trillion in global debt, or almost 30% of total, into negative yield territory...

... we were certainly expecting some much deserved gloating at the expense of all those who said the 30 year bond bull market was over, in his latest letter. However, we were surprised when instead, Edwards - clearly aware what was expected of him - said that he "resisted the obvious temptation to write about the incredible bond market rally that has unfolded before our eyes" although even he couldn't help himself to note "that more high profile names are now seriously contemplating a negative US 10y bond yield, with the folks at PIMCO also now seeing it as a plausible outcome in the next recession."

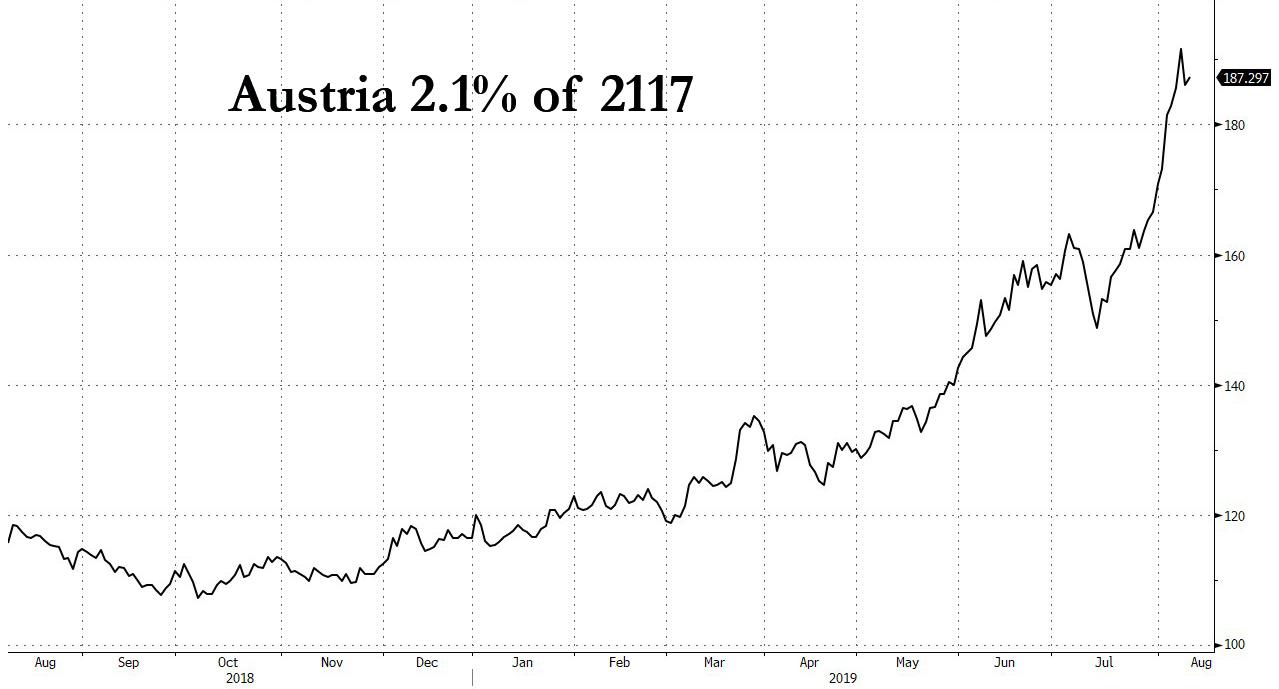

So instead of pointing out charts such as this one, which shows the parabolic price increase in ultra high duration bonds such as Austrian 100Ys...

... what Edwards focused on in his latest periodic report was China in the wake of the intensification of the trade/currency war and the recent historic breach of the 7.00 Yuan floor, and in typical style, Edwards cautioned that "investors may be underestimating the turmoil that is now stirring under the surface in China. All may not be as stable as investors suppose."

One of Edwards' key argument is, as we said earlier today, that contrary to popular opinion, it is not China that is winning the trade war - after all it has the benefit of time, while Trump has to win (or lose) the war ahead of the 2020 presidential election - but rather it is Trump who has the upper hand (today's news of a 3rd major Chinese bank failure/bailout in as months certainly underscores Edwards' claim). In this context, he asks the following rhetorical question:

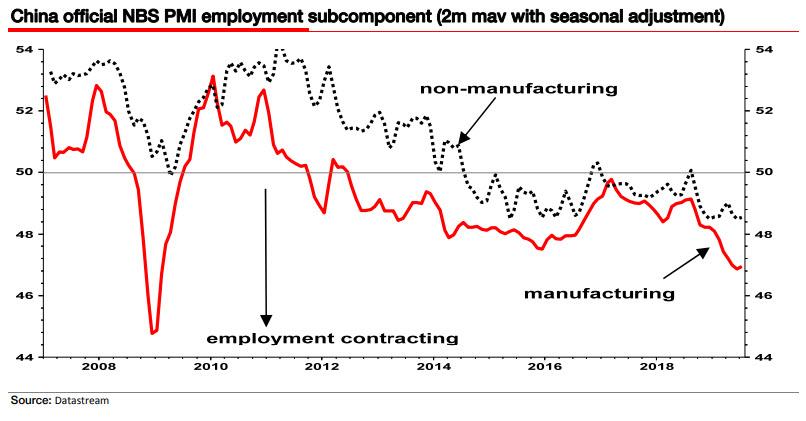

... what happens if this consensus is wrong? What if China is in a far more vulnerable situation than investors realise? US economic data has been poor of late but it hasn’t been great in China either. I think the chart below showing a rapidly contracting jobs market will be a key concern to the Chinese authorities. Indeed, our own China economist, Wei Yao, described the economy being on “shaky ground” in a recent note.

Next, since we already bored readers with our take on the 3rd consecutive bank failure in China earlier this morning, we will only touch on Edwards' next point, which not surprisingly, refers to China's growing bank instability, and which notes that "more concerning are the ructions in the banking sector after the recent bailout of Baoshang Bank. Wei writes “It would not be an overstatement to say that Baoshang’s fallout is a milestone in China’s deleveraging reform and financial liberalisation. The deleveraging process is bound to expose weak institutions along the way, and it is only a matter of time before counter-party risk reaches the interbank market. …When the deleveraging process enters the very core of the financial system, the risk of things going terribly wrong rises [ZH: just as we said earlier today]. We still think China has a chance to pull through without a financial crisis, given the Chinese government’s control over many things…but we will be keeping a close eye on interbank developments, as this may be the source of under-appreciated risk for the global economy. We are not yet convinced of a clear recovery trend. Against a backdrop of continued trade uncertainties and deterioration in the liquidity conditions of small financial institutions after the PBoC’s takeover of Baoshang Bank, the economy remains on shaky ground."....MUCH MORE

The Baoshang bailout (seizure?) has been followed by yet another banking intervention. This has certainly caused far more tremors in the interbank market than anyone appeared to be expecting, and has led to a credit crunch for Chinese small and medium sized companies which is likely to exacerbate the economic slowdown. To be honest, understanding the mechanics of all these issues is slightly beyond me, but even a generalist like myself can see that all does not seem to be well under China’s financial hood (Zero Hedge is worth reading link).Which brings us to the core of the paper, which is Edwards' rhetorical allegation that "what if - take a deep breath - the Chinese authorities are not as in control of events as investors assume? One reason why Edwards believes that is the case is due to his confidence in their economic management plunging from pretty high levels in the aftermath of the Shanghai Stock exchange bubble bursting in mid-2015, to wit:

It seemed odd back in H1 2015 that the normally cautious Chinese authorities acted as vocal cheer leaders for the equity market's vertiginous rise back then. But it sort of made sense in the context of ravenous foreign appetite for Chinese stocks in expectation that MSCI was about to allow mainland China shares into its Emerging Market Index. One reasonable interpretation of the Chinese authorities allowing (encouraging) that horrendous bubble to develop is that it served the purpose off allowing overleveraged companies to convert excess balance sheet debt into equity that would be bought by over-enthusiastic foreigners who failed to realize a renminbi devaluation was just around the corner (better for Chinese companies to have eliminated their dollar debt and convert it to renminbi equity liabilities)Everyone knows what happened next: MSCI failed to play ball. On 9 June 2015 it announced against expectations that it would not include Chinese stocks in its EM index.....