Following on the earlier "Inflation: BEA personal Consumption Expenditures Price Index, July 2024".

From Wold Street, August 30:

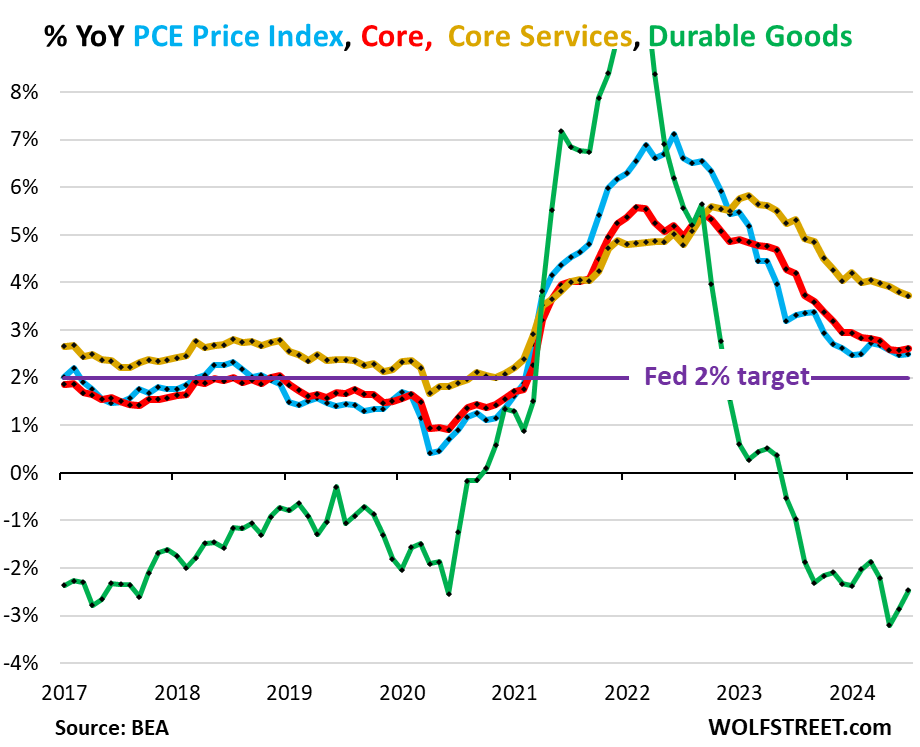

Month-to-month, core services inflation jumped while durable goods deflation deepened, and so core PCE price index hits Fed’s target.

The “Core” PCE price index, the Fed’s primary yardstick for its 2% inflation target, rose by 2.62% from a year ago in July, a hair up from the June reading of 2.58% (red in the chart below). This “core” index attempts to show underlying inflation by excluding the components of food and energy as they can be very volatile, spiking and plunging with commodity prices (red in the chart below).

The overall PCE price index, which includes the food and energy components, rose by 2.50% year-over-year in July, also a hair up from June’s 2.47% (blue). Within it, energy prices edged up year-over-year by 0.2%, and food prices rose 1.4%.

The “core services” PCE price index rose by 3.72% in July, down a hair from June’s 3.81% increase (yellow). But the durable goods PCE price index fell less than in the prior two months, in July by -2.5% year-over-year. May’s drop of -3.2% had been the biggest drop since 2004 (green):

The month-to-month moves.

The “core” PCE price index rose by 2.0% annualized in July from June (not annualized, +0.16%), same as in June. Both months were right on the Fed’s target (blue in the chart below).

Within it, core services inflation accelerated sharply in July from June (+3.3% annualized), while the durable goods index dropped deeper into the negative (-3.7% annualized). Those two forces combined, pulling in opposite directions, caused the index to rise by 2.0% annualized. And that has also been the dynamic we’ve seen so far this year: Durable goods prices are deflating sharply from the pandemic spike while services inflation is still uncomfortably high.

The six-month annualized core PCE price index, which irons out the month-to-month squiggles and revisions, and which Powell cites a lot, decelerated to 3.3%, as the January spike fell out of the index (red):....

....MUCH MORE

We are looking for a re-ignition of both CPI and PCE in 2025. More on that as we get closer to year-end.