First up, Jan. 25, "Russian Sovereign Funds: Down, but Not Out, Yet…":

In the context of 2016 Budget, Russian sovereign reserves dynamics are clearly an important consideration. For example, in his recent statement, former Russian Finance Minister, Kudrin, has suggested that if Budget deficit reaches above 5% of GDP in 2016, the entire cushion of liquid foreign reserves held by the Government will be exhausted by the end of the year, leaving Russia exposed to big cuts in the budget for 2017. This is similar to the positions of Russia's Economy Minister Alexei Ulyukayev and the current Finance Minister Anton Siluanov.

The expectations are based on three considerations:

1) 2015 dynamics of Russian sovereign wealth funds;

2) Funds outflows expected under the external debt repayment schedules; and

3) A potentially massive call on Russian reserves from the VEB capital requirements.

I covered the last point earlier here. So let’s take a look at the first point.

Russia’s main and more liquid Reserve Fund shrank substantially last year as it carried out its explicit mandate to provide support for fiscal balance. Set up in 2008, the fund holds only liquid foreign assets and 2015 became the first year since the Great Recession and the Global Financial Crisis (2009-2010 in Russia’s case) when it experienced net withdrawals. The value of the fund fell from roughly USD90 billion to ca USD50 billion by the end of December 2015.

However, the key to these holdings is their Ruble equivalent, as Russian budgetary expenditures are in domestic currency. By this metric, the Fund has been doing somewhat better. By end of December 2015, the Reserve Fund held assets valued at RUB3.6 trillion, amounting to almost 5 percent of Russian GDP or roughly 1.7 times Budget 2016 requirement for deficit coverage. Budget 2016 is based on expectation that the Reserve Fund will supply some RUB2.1 trillion to cover the deficit.

The sticking point is that Budget 2016 - in its current reincarnation - is based on oil price of USD50pb. The Ministry of Finance is currently preparing amended Budget based on USD30-35pb price of Brent, but we are yet to see the resulting deficits projections. What we do know is that the Government has requested up to 10 percent cuts across public expenditure for 2016. Absent such cuts, and if oil prices remain around USD30pb mark, the deficit is likely to balloon to the levels where 2016 deficit will end up fully depleting the Reserve Fund.

Added safety cushion, of course, will be provided by devaluation of the Ruble. This worked pretty well in 2015, but the problem going into 2016 is that required further devaluations will likely bring Ruble into USDRUB 90+ range, inducing severe redistribution of losses onto the shoulders of consumers and cutting hard into companies investment in new equipment and technologies.

Bofit provided a handy chart showing the dynamics of Fund resources and a breakdown of these dynamics by key factors...

And today:

26/1/16: Russian External Debt: Deleveraging Goes On

In previous post, I covered the drawdowns on Russian SWFs over 2015. As promised, here is the capital outflows / debt redemptions part of the equation.

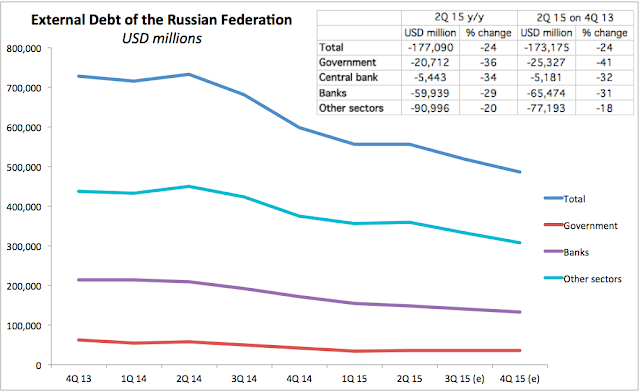

The latest data for changes in the composition of External Debt of the Russian Federation that we have dates back to the end of 2Q 2015. We also have projections of maturities of debt forward, allowing us to estimate - based on schedule - debt redemptions through 4Q 2015. Chart below illustrates the trend.

As shown in the chart above, based on estimated schedule of repayments, by the end of 2015, Russia total external debt has declined by some USD177.1 billion or 24 percent. Some of this was converted into equity and domestic debt, and some (3Q-4Q maturities) would have been rolled over. Still, that is a sizeable chunk of external debt gone - a very rapid rate of economy’s deleveraging.

Compositionally, a bulk of this came from the ‘Other Sectors’, but in percentage terms, the largest decline has been in the General Government category, where the decline y/y was 36 percent.

Looking at forward schedule of maturities, the following chart highlights the overall trend decline in debt redemptions coming forward in 2016 and into 2Q 2017....

...MORE

HT: Mike Norman Economics