Ever since the financial crisis, James Owen Weatherall writes in his new book, “The Physics of Wall Street,” “words like ‘quant,’ ‘derivative’ and ‘model’ have taken on some nasty connotations.” He is out to change that.

What finance and economics need, he says, is more physics, not less. So what if the quantitative models that underlay such products as mortgage-backed securities blew up, nearly bringing down the world financial system in the process? Models always have assumptions; it is up to the users to pay attention to whether those assumptions hold.Did some so-called quants — investors who use sophisticated mathematical models in deciding what and when to buy and sell — lose their shirts? Indeed they did. But others did not. Weatherall points to Renaissance Technologies, a hedge fund founded by James Simons, who was an esteemed mathematician before he became an esteemed investor. Simons’s success, Weatherall argues, “shows that mathematical sophistication is the remedy, not the disease.”Weatherall, an assistant professor of logic and philosophy of science at the University of California, Irvine, has two Ph.D.’s — one in physics and mathematics, and one in philosophy — and he has really written two books. The first, which takes up much of the volume, is an entertaining and enlightening tale of the history of finance and gambling. Along the way we meet a neglected Frenchman named Louis Bachelier, who, Weatherall says, invented mathematical finance in 1900 with a thesis proposing that probability theory could be used to understand financial markets. This notion may seem obvious now — people who don’t like Wall Street often refer to it as a casino — but at the time Bachelier’s findings didn’t impress much of anyone. He had trouble getting academic jobs, and his work was forgotten until the 1950s, when it was rediscovered by the M.I.T. economist and Nobel laureate Paul Samuelson....MORE, including the future of finance.

We've had a couple posts on Bachelier:

"Pricing the Future: Finance, Physics, and the 300-Year Journey to the Black-Scholes Equation "

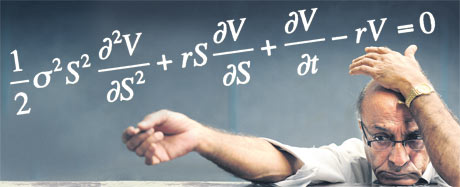

Variables: σ = volatility of returns of the underlying asset/commodity; S = its spot (current) price; δ = rate of change; V = price of financial derivative; r = risk-free interest rate; t = time.