“Leading up to the financial crisis, investors displayed an incorrect assessment of systemic risk and significantly increased their leverage and risk-taking activities. Barnett documents that better Federal Reserve data could have signaled the error in that view. This error led to the credit-driven, asset-price bubble in the U.S. housing market. He also has shown that as a result of measurement errors, monetary policy was damaged, with tragic consequences. He is the world’s foremost authority in the study of monetary and financial aggregation using index number and aggregation theory.”Martin Wolf in his February 12 Financial Times column made an oblique reference to what I think may have been the basis of many misplaced inflation fears dating to the 2009 Stimulus and the extraordinary measures of the Federal Reserve:

-James J. Heckman, University of Chicago and University College Dublin, Nobel Laureate in Economics on William A. Barnett's book Getting it Wrong.

The case for helicopter money

...Measures of broad money have stagnated since the crisis began, despite ultra-low interest rates and rapid growth in the balance sheets of central banks. Data on “divisia money” (a well-known way of aggregating the components of broad money), computed by the Center for Financial Stability in New York, show that broad money (M4) was 17 per cent below its 1967-2008 trend in December 2012. The US has suffered from famine, not surfeit.Wolf wears his erudition so lightly that he puts into a throw-away line one of the more important things I've read in quite a while. Money growth was below trend, and by quite a bit, as recently as last month!

As Claudio Borio of the Bank for International Settlements puts it in a recent paper, “The financial cycle and macroeconomics: what have we learnt?”, “deposits are not endowments that precede loan formation; it is loans that create deposits”. Thus, when banks cease to lend, deposits stagnate. In the UK, the lending counterpart of M4 was 17 per cent lower at the end of 2012 than in March 2009. (See charts.).

Those convinced hyperinflation is around the corner believe that banks expand their lending in direct response to their holdings of reserves at the central bank. Under a gold standard, reserves are indeed limited. Banks need to look at them rather carefully....MORE

Here are the FT charts he is referencing:

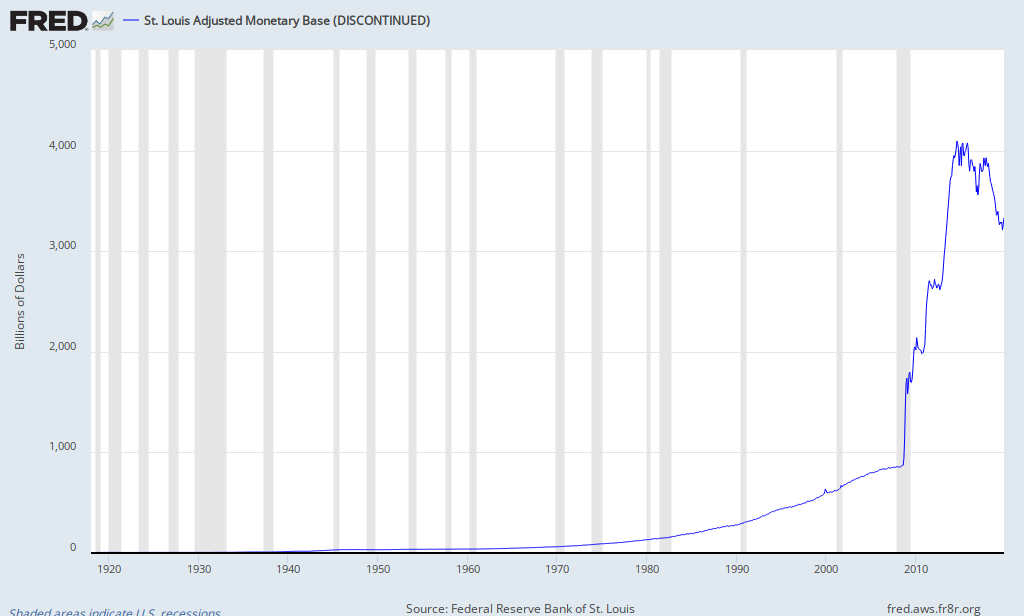

If you look only at the monetary base* the inflationistas were beshatting themselves over:

you will note what chartmeisters call a "discontinuity" in 2009 which was the source of much concern. But the concern was not reflected in the inflation numbers. Why?

We've probably been been measuring the wrong thing.

Here's Steve Hanke from the Center for Financial Stability at Energy Tribune three weeks ago:

Rethinking Conventional Wisdom: A Monetary Tour d'Horizon for 2013

By Steve H. HankeThe year 2012 has come and gone, and so have many things that were once accepted as conventional wisdom. Let’s take a tour d’horizon and examine three ideas that bear rethinking in 2013.

Rethinking the Money Supply

I begin with the nonsensical way that most central banks, including the U.S. Federal Reserve, measure the money supply. Conventional wisdom holds that the best way to measure the money supply is to define the components that make up a particular measure of money (from M0 to broad M4) and then simply add up the components to obtain a total.

But, this convention contains a fatal economic flaw. The components (assets) that make up the money supply contain varying degrees of “moneyness” – defined as the ease of, and the opportunity costs associated with, exchanging assets into money that can be readily used in transactions for goods and services. Accordingly, the components should not receive the same weights when added together to yield a money supply measure. Those components with the most moneyness should be weighted more heavily than assets with less moneyness.

Thanks to Prof. William A. Barnett and the Center for Financial Stability (CFS) in New York, the superior measure of the money supply for the U.S. is available. The components are given weights, depending on objective market prices, before they are summed to yield a “Divisia” metric (after its inventor, the famous French engineer-economist François Divisia, 1889-1964).

To illustrate just how dangerous the conventional wisdom about the money supply can be, let’s revisit former Fed Chairman Paul Volcker’s highly praised inflation squeeze, which was ably profiled by Prof. William Silber, in his recent book Volcker: The Triumph of Persistence (Bloomsbury: 2012).

In the late summer of 1979, when Paul Volcker took the reins of the Federal Reserve System, the state of the U.S. economy’s health was “bad.” Indeed, 1979 ended with a double-digit inflation rate of 13.3%.

Chairman Volcker realized that money matters, and it didn’t take him long to make his move. On Saturday, 6 October 1979, he stunned the world with an unanticipated announcement. He proclaimed that he was going to put measures of the money supply on the Fed’s dashboard. For him, it was obvious that, to restore the U.S. economy to good health, inflation would have to be wrung out of the economy. And to kill inflation, the money supply would have to be controlled.Here's the last release from the CFS:

Chairman Volcker achieved his goal. By 1982, the annual rate of inflation had dropped to 3.8% – a great accomplishment. The problem was that the Volcker inflation squeeze brought with it a relatively short recession (less than a year) that started in January 1980, and another much larger slump that began shortly thereafter and ended in November 1982.

Chairman Volcker’s problem was that the monetary speedometer installed on his dashboard was defective – he was only looking at the conventional, simple-sum measures of the money supply. The Fed thought that the double-digit Fed funds rates it was serving up were allowing it to tap on the money-supply brakes with just the right amount of pressure. In fact, if the money supply would have been measured correctly by a Divisia metric, Chairman Volcker would have realized that the Fed was slamming on the brakes from 1978 until early 1982, imposing a monetary policy that was much tighter than it thought (see the accompanying chart).

Why the huge divergences between the conventional simple-sum measures of M2 that Chairman Volcker was observing and the true M2 Divisia measure? As the Fed pushed the Fed funds rate up, the opportunity cost of holding cash increased. In consequence, savings accounts, for example, became relatively more attractive and received a lower weight when measured by a Divisia metric. Faced with a higher interest rate, people had a much stronger incentive to avoid “large” cash and checking account balances. As the Fed funds rate went up, the divergence between the simple-sum and Divisia M2 measures became greater and greater.

When available, Divisia measures are the “best” measures of the money supply. But, how many classes of financial assets that possess moneyness should be added together to determine the money supply? This is a case in which “the more the merrier” applies. When it comes to money, the broadest measure of money, Divisia M4, is the best. In the U.S., we are fortunate to have this available from the CFS.

If we discard conventional wisdom and employ a broad Divisia M4 measure for the U.S., it appears that some green shoots are springing up. As the accompanying chart shows, Divisia M4 has recently moved up at a brisk pace and is growing at a relatively healthy rate (6.9% in December 2012).

If the U.S. money supply keeps growing at this rate, I expect the U.S. economy to exit its growth recession and enter a period of trend-rate growth in 2013. With that more normal growth, unemployment will fall from its current elevated level of 7.8%

Rethinking Basel III

Another bit of conventional wisdom has it that tightening regulations on bank capital and liquidity – the Bank for International Settlements’ so-called Basel rules – will make banks safer. Well, things haven’t worked out according to plan. As history has shown, more stringent Basel Rules place a damper on what I call “bank money” – the all-important portion of the money supply produced by banks, through deposit creation. If this squeeze is big enough, it can throw an economy into a slump....MUCH MORE

HIGHLIGHTS

BASED ON DATA RELEASED AT 9:00 A.M. EST, JANUARY 16, 2013

NEW FED TARGETS AND MONEY:

CFS MONEY SUPPLY STATISTICS

Today, CFS monetary data decisively demonstrate that the US economy is gaining momentum. This presents a contrast to our last three consecutive months that clearly signaled the economy bottomed. Despite worries surrounding the fiscal cliff, the broadest measure of money (CFS Divisia M4) gained 6.9% in December 2012 on a year-over-year basis. This represents the most rapid expansion in broad money in the economy since 2008. CFS Divisia M4 gained 5.1% on a year-over-year basis in the previous month and a scant 0.9% in December 2011. So, the financial system and the economy are on the mend....MUCH MORE (3 page PDF)And more Barnett via the Kansas City Star.

*You get the same sort of step changes with the M's, although not as dramatic when shown on a shorter time-line, here's M1: