As we've said over the years, we like journalists. We've gotten some of our best ideas from journalists. So, as partial recompense (in addition to subscriptions and the event fees etc.) here is reassurance that the scribing and scribbling has value long past the expiration date of the scribes and scribblers.

The headline is the title of the paper, here's the story at Knowledge@Wharton, May 9:

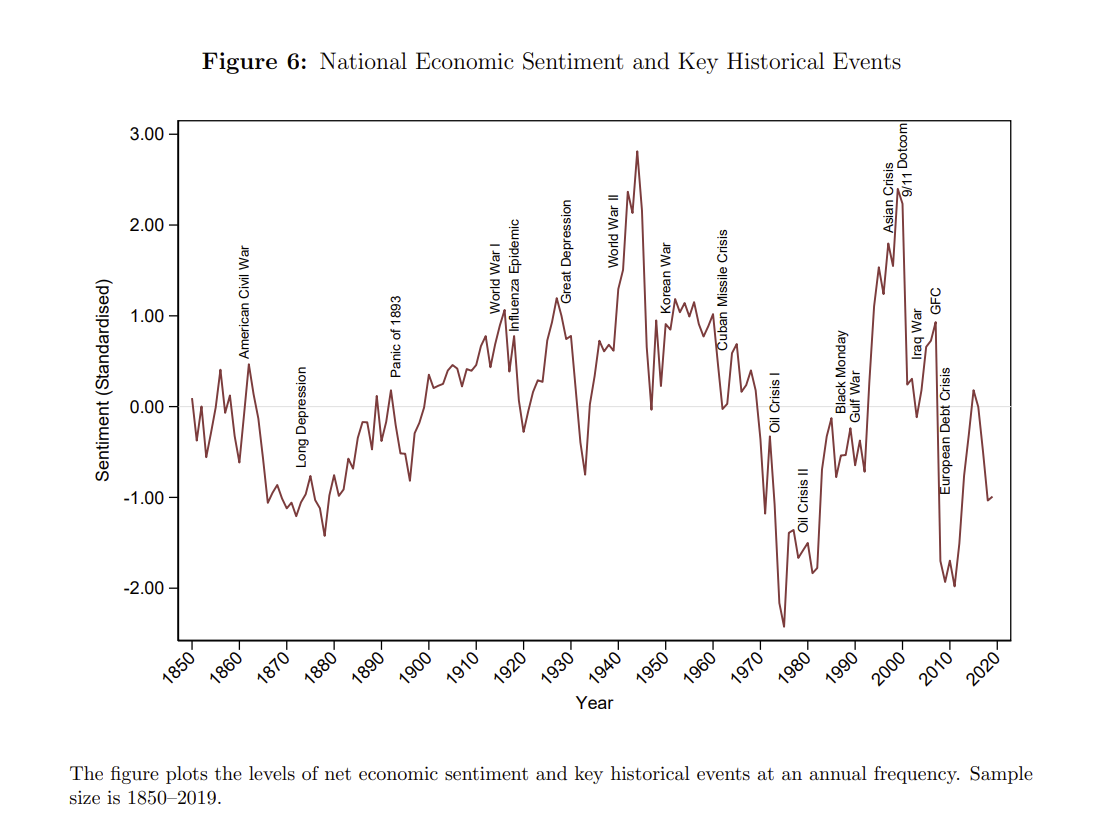

A study by experts at Wharton and elsewhere captures changing economic sentiment over 170 years to predict fundamentals such as GDP growth, employment, and monetary policy decisions. The study leads conventional forecasting models on several counts: in time series by more than a century; in capturing important information existing models fail to capture; in granularity that tracks nationwide and state-level variations; and in cross-sectional variations.

The study’s findings are published in a paper titled “(Almost) 200 Years of News-Based Economic Sentiment,” authored by Wharton finance professor Jules H. van Binsbergen, London Business School finance professor Svetlana Bryzgalova, London Business School doctoral student Mayukh Mukhopadhyay, and Nanyang Business School finance professor Varun Sharma.

The study customized a machine learning technique to create an algorithm that analyzed more than a billion articles across 200 million pages of 13,000 U.S. local newspapers from 1850 to 2017; the authors claimed that dataset is 95 times larger than the total amount of all of the English-language Wikipedia entries combined. The inclusion of local newspapers enabled them to measure sentiment on a granular basis at the city, county, and state levels.

“If you want to better understand the role that sentiment has on economic activity, GDP growth, labor market decisions, and other fundamentals, it’s always better to have more granular and longer time series data,” Binsbergen said. “We show this sentiment has predictive power for economic activity over and above the standard predictors such as the so-called yield spread, or the difference between long-term and short-term interest rates as well as lagged GDP data (or economic growth after it occurred).”

Leading Conventional Forecasts

Significantly, the study’s model leads the Philadelphia Fed’s Survey of Professional Forecasters in predicting the next quarter’s consensus value of macroeconomic fundamentals, and it betters the Michigan Survey of Consumer Sentiment in the length of time (the Michigan Survey is available from 1966) and in providing state-level variations; the common component of national news and local news is only 35%, and the remainder is made of local news....

....MUCH MORE