From FT Alphaville:

In just two weeks time, President Trump and Chinese leader Xi Jinping are set to meet in sunny Buenos Aires, Argentina for the G20 summit. Whether the two heads of state can leave with a deal in hand to tame the trade war is anyone's guess, but soyabean farmers are holding out hope.

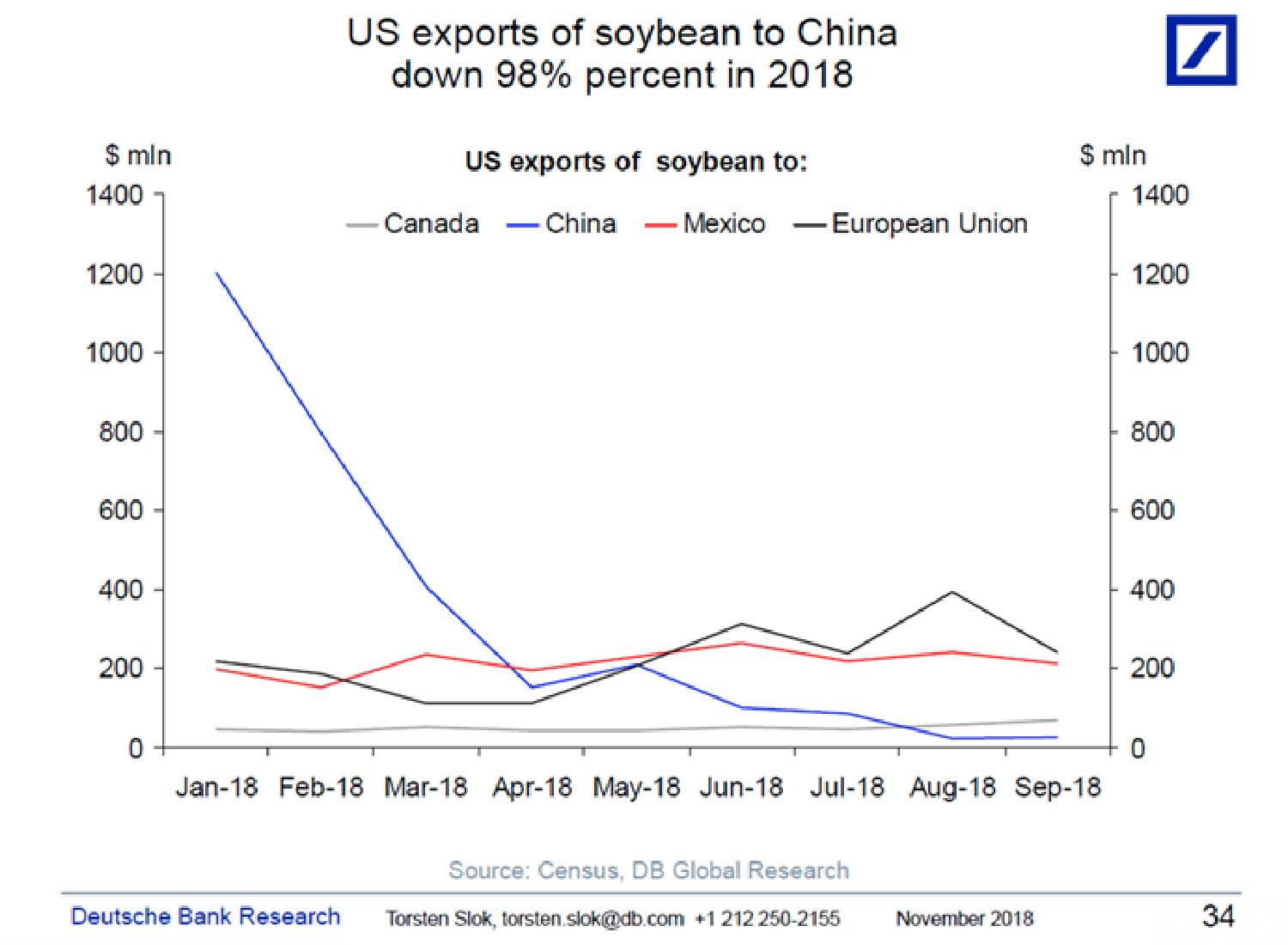

Deutsche Bank's Torsten Slok put out an alarming chart Friday, showing the absolute cratering of US soyabean exports to China this year. Since January, US shipments of the legume have fallen 98 per cent:

For the farmers who harvest the crop, their livelihoods were more or less destroyed as the trade war racheted up.If a business/finance writer can get a grounding in the boring bits, the nuts and bolts of the matrix of connections, they can bring more and more value-added to the keyboard if and when they switch gears and pursue a flight of fancy.

The US has imposed tariffs on $250bn worth of Chinese imports and has threatened to jack up the rate, from 10 per cent to 25 per cent, on $200bn of that total in January, should China retailitate further. Already, China has levied duties on $110bn worth of US imports, or roughly 85 per cent of what comes into the country from the States.

For Citi's Aakash Doshi, the worst may in fact be over. At least that's what soyabean price differentials tell him. China purchases two out of every three soyabean bushels available for foreign trade, and the US and Brazil sell about 85-90 per cent of the soyabeans that China imports, says Doshi. So the price of US Gulf Coast soybeans for export, compared to the FX-adjusted soyabean export price at major Brazilian ports, can tell us a lot about the status of the ongoing trade negotiations....MORE

Below is the introduction to a 2016 link that touched on a related point, mastery:

Global Macro: There Are Many Ways To Approach It, Here's A Good One

A couple weeks ago I emailed a friend:Re: posts on moneyYears ago one of the mentors said you can approach macro from a lot of starting points, for him it was bonds, he had internalized the price/interest rate teeter-totter to the point that if the other parts of the matrix, currencies or metals or equities, whatever, didn't fit the paradigm he'd know he was looking at either danger or opportunity.

So if someone who is doing the grunt work says en passant "beans may have bottomed" it may behoove the consumer of data/information/knowledge/wisdom to take note and be aware something might have changed and the game may be afoot:I can't go so far as to say they are all fungible but along with empirically derived lead/lag times, grit in the gears/slippage inefficiencies and leverage it's a close enough first approximation to use as a mental model.The key is to have enough exposure to your subject that your understanding is innate, that you don't have to consciously think "Now when interest rates go down, bonds go up". When you've achieved this level of mastery you immediately sense when the presented facts aren't conforming to the mental model and may be worth further scrutiny.

Another way in to global macro is commodities and if this is your choice it helps to internalize curves to the point the dangers/opportunities pop when you look at them.

Permit me to present Izabella Kaminska, writing at FT Alphaville:...

Huh.