America’s growth has a slowed a lot in the past two years. Why?

The latest estimates from the Bureau of Economic Analysis show the US economy grew by 1.9 per cent in the past four quarters* — the same pace as in 2015 and significantly slower than 2013 (2.7 per cent) or 2014 (2.5 per cent).

Delineating things by calendar years is arbitrary, however. What’s more relevant is America’s four-quarter growth rate had been steadily accelerating since the low point in mid-2013, peaked at 3.3 per cent in the beginning of 2015, slowed by a little more than 2 percentage points by the middle of last year, and began turning around in the second half of 2016:

So what explains the 1.4 percentage point deceleration in growth? At a mechanical level you can say GDP is just hours worked multiplied by productivity. Since the growth rate in jobs has slowed by about a percentage point since the beginning of 2015, you’d expect overall output growth to slow by about that much.

This is not a particularly interesting insight, however, so instead let’s look at the detailed sectoral breakdowns provided by the BEA in table 1.5.2 of the National Income and Product Accounts.

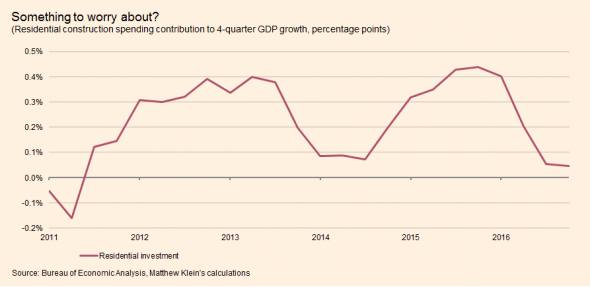

About half of the 1.4 percentage point slowdown in the growth rate since the beginning of 2015 can be explained by restrained business investment (0.42 percentage points slower) and residential construction (0.27 percentage points slower). Both categories of spending grew in the past four quarters, but only barely, together contributing just 9 basis points to the total GDP growth rate. It will be hard to improve output per hour if capital investment continues to be so small.

Homebuilding grew at its slowest 4-quarter rate since 2011. The last time construction spending slowed this much it coincided with the “taper tantrum”. On the bright side, the quarterly data suggest the recent deceleration seems to have been driven more by events in the middle of the year than at the end, so it’s possible the increase in mortgage rates may not have much negative impact for next year. Alternatively, it could mean the housing market was in trouble even before rates began rising, in which case the outlook for next year could be quite poor:

It’s tough to blame the weak performance of business investment on the change in commodity prices, as tempting as that may be. Investment in structures, which includes spending on wells and drilling, was collapsing then and is now recovering in line with the big growth (from a much lower base) in the number of active oil rigs....MUCH MORE

Almost all (37 out of 42 bps) of the slowdown in overall business fixed investment since the beginning of 2015 can be explained by the decline in spending on transportation equipment — traditionally one of the most important cyclical components in the entire economy. The good news is that spending on transportation equipment may have hit bottom if the initial estimates for the last three months of 2016 aren’t revised down....