Benchmarking Multi-Asset Portfolios: The Global Capital Stock

Multi-asset investing is nothing new.

William Sharpe first postulated that the market portfolio was the natural starting point in portfolio construction in 1964. The balanced portfolio, which held fixed proportions of bonds and equities, was another antecedent to today’s multi-asset portfolio.

With increased global access to various asset classes, multi-asset investing has entered the mainstream for certain second generation asset allocation methods — for multi-factor/multi-period models.

Constructing optimally diversified multi-asset portfolios is all the more critical for investors who follow the principles of such third generation asset allocation methods as adaptive asset allocation or adaptive risk management techniques.

Multi-asset investing’s growing popularity reflects these preferences: More than 14,000 multi-asset funds are offered in Europe alone.

Yet after all these years, the core question remains: How do you know whether a multi-asset portfolio is worth the investment?

Observation vs. Opinion

Many institutions have policy guidelines based on their investment managers’ preferences and expectations about the risks and returns associated with each asset class.

Other institutional investors run peer-group comparisons with similar multi-asset managers or measure their portfolios against broadly defined total return indices.

But these are only work-arounds. No policy portfolio benchmark exists against which investors can measure their multi-asset investment strategy.

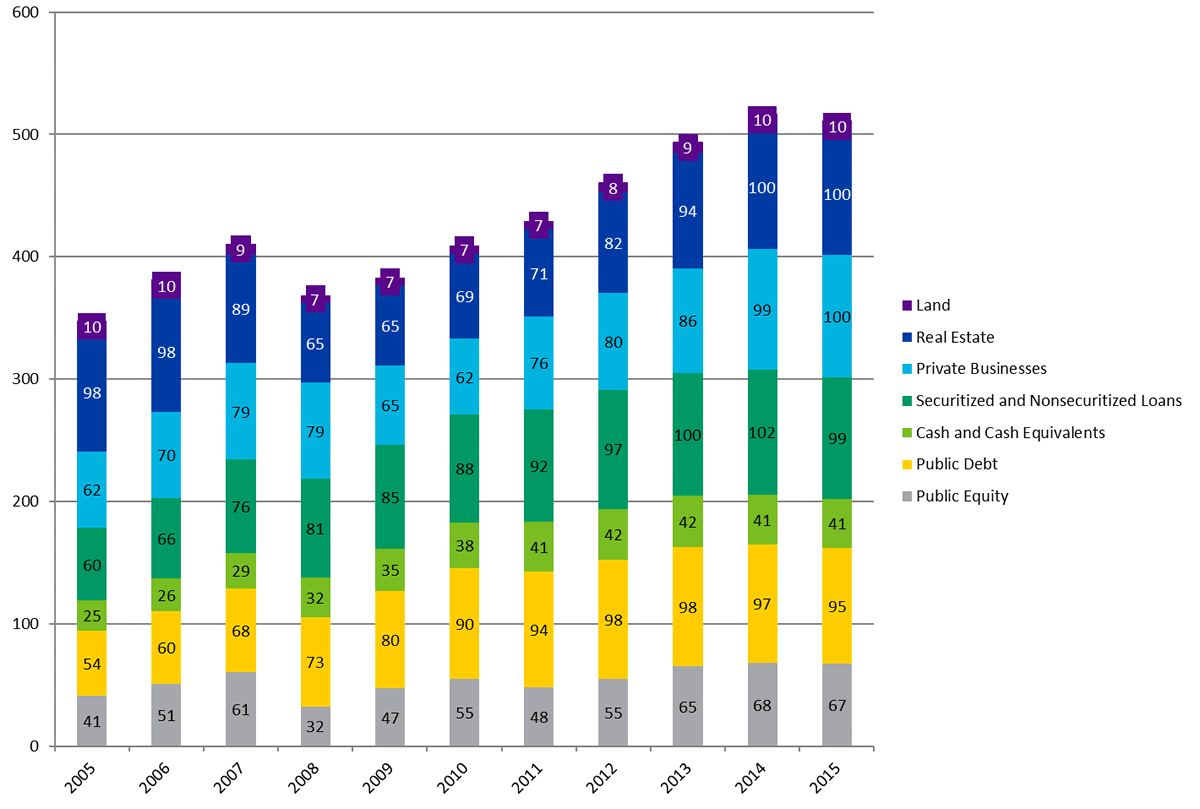

A hypothetical global index purist could simply buy all of the outstanding assets in the world. The resulting global market portfolio would include all risky assets in proportion to their market capitalization. The purist could then use this as a benchmark to compare strategies.

While this approach has an appeal, not all risky assets are investable or measurable. With publicly available financial databases, we can now compute a global investable market portfolio. Researchers at McKinsey Global Institute report built a “map” of global financial assets. However, their data incorporated only traditional financial assets, omitting alternative assets.

So other researchers went a step further and added real estate and private equity to their broader asset universe. But they only included investable assets, with their portfolio weights based on their assets under management (AUM).

One Step Beyond

Our calculations are the next logical stage in this evolution. Our springboard is the definition of “capital.”

Capital is “non-financial assets having a dual role in an economy, being both a source of capital services in production and a storage of wealth,” according to the United Nations System of National Accounts (UNSNA)....MUCH MORE

Here's "The Global Capital Stock. A Proxy for the Unobservable Global Market Portfolio" at the SSRN:

Abstract:

This article summarizes our attempt to measure the current economic stock of a broad universe of risky assets worldwide. Therefore, by measuring the global capital stock of assets, financial and non-financial ones, we intend to provide a proxy for the global market portfolio. We compute the market value of global assets included in 11 asset classes for the period 2005-2015. Despite the lack of data for non-financial assets, we consider our methodologies sound and feel strongly optimistic about future development, which will further reduce the margin of error and then provide a more accurate benchmark for multi-asset portfolios.