From Wolf Street, May 20:

This is the first time I’ve seen Wall Street banks clamor for the Fed to back off QE. The Fed is struggling to keep the liquidity it created from going haywire

In the fall of 2019, when the repo market blew out, the Fed stepped in and bought Treasury securities and MBS and handed out cash via repurchase agreements. When these repos matured, the Fed got its money back, and the counterparties got their securities back. The Fed also did this during the market rout in March 2020. But by July 2020, the last repos matured and were unwound.

Now the Fed is doing the opposite, with “reverse repos.” Repos are assets on the Fed’s balance sheet. Reverse repos are liabilities. With these reverse repos, the Fed is now massively selling Treasury securities to counterparties and taking their cash, thereby draining liquidity from the market – the opposite effect of QE.

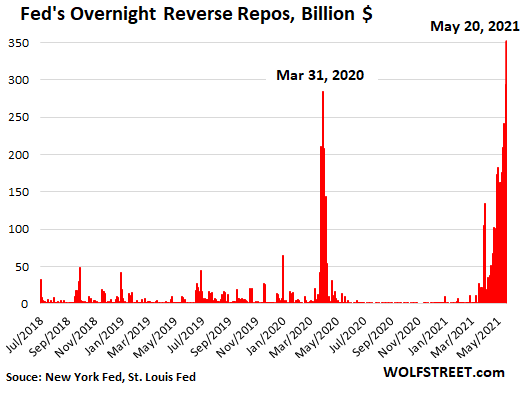

This morning, the Fed sold $351 billion in Treasury securities via overnight reverse repos to 48 counter parties, thereby blowing past the brief spike at the end of March 2020, and more than replacing yesterday’s $294 billion in Treasury securities that it has sold via reverse repos to 43 counterparties and that matured and unwound this morning.

These reverse repos are a sign that the banking system is struggling to deal with the liquidity that the Fed has been injecting via its QE. And that’s in part why there is now some clamoring on Wall Street for the Fed to taper its QE purchases because the banking system is now drowning in liquidity that banks have as reserves on their balance sheet. By buying Treasuries in the repo market, the banks lower their reserves and increase their Treasury holdings.

So with one hand, as part of QE, the Fed is buying $120 billion a month in Treasury securities and MBS. With the other hand, the Fed took back $351 billion via overnight reverse repos, undoing nearly three months of QE.

It’s the kind of crazy situation that you run into when you push something to the extreme, as the Fed has done with its asset purchases, and you get all kinds of side effects.

The Fed addressed these reverse repos and the mountain of reserves during the last FOMC meeting, and released a summary of the discussions in its minutes yesterday.

Reserves are cash that the banks deposit at the Federal Reserve and that the Fed owes the banks. They’re a liability on the Fed’s balance sheet. The Fed pays interest (currently 0.1%) on these reserves. The reserves on deposit at the Fed have now spiked to $3.92 trillion:....

....MUCH MORE

Trouble In Repo Land—The QE Endgame: A Big Problem Is Emerging For The Fed