From Narrow Road Capital, May 30:

The US high yield market has grown larger and riskier since the

financial crisis. Issuers of debt have the whip hand as buyers compete

to gain an allocation in the face of surging demand from CLOs and retail

funds. Companies are emboldened to seek ever weaker covenants and are

taking advantage of the current conditions to borrow more at lower

margins. It’s as if the financial crisis never happened and the lessons

from it are ancient history.

Whilst the timing of a downturn in high yield debt isn’t predictable,

the outcomes when it does happen are. More debt, of lower quality, with

weaker covenants means the coming downturn will be bigger, longer and

uglier. A quick review of some key data makes this clear.

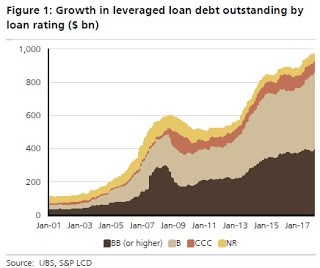

Firstly, the size of the US high yield bond market and leveraged loan market are both close to double what they were in 2007.

Not only is the debt outstanding larger, but the credit ratings have

shifted downwards on leveraged loans. Lower credit ratings mean a higher

percentage of the outstanding debt will default when liquidity dries

up.

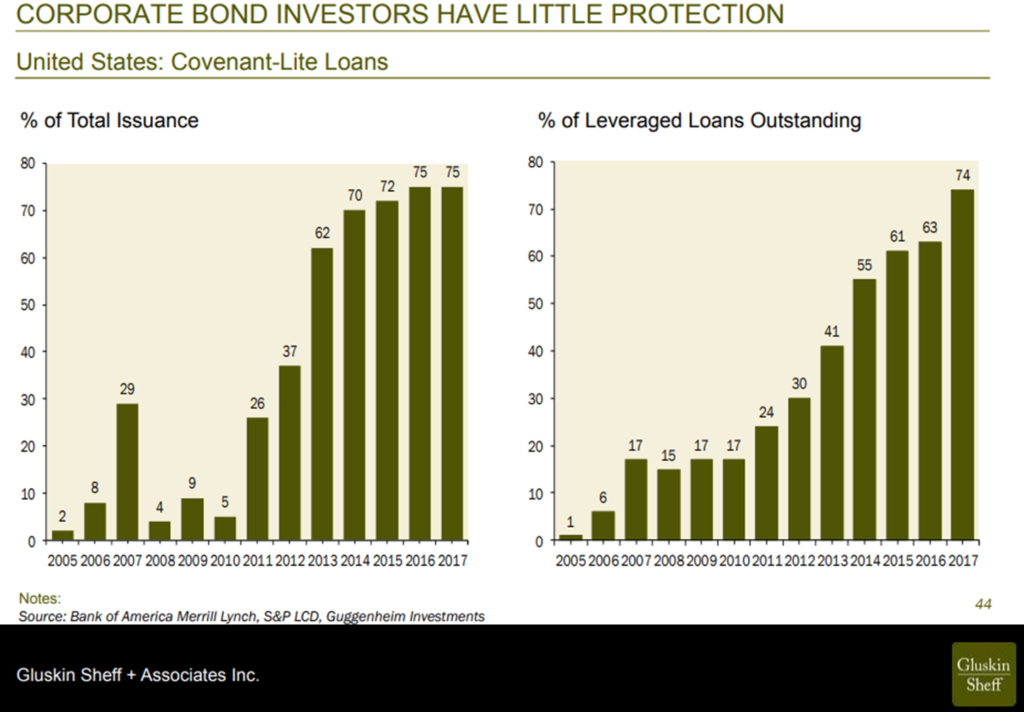

The other key indicator to watch is the share of the loan market that

has weak covenants. In 2007, 17% of outstanding loans were

covenant-lite. Today it’s over 75% with over 80% of new issuance

lacking decent covenant protections. Weak covenants delay the

occurrence of an event of default, which allows zombie companies to

continue operating until they either exhaust their cash reserves or

cannot refinance maturing debt.

High yield bulls are likely to cite the substantial equity

contributions from sponsors and healthy interest coverage ratios as

reasons not to be overly concerned. These are definitely much better

than 2007, but these indicators do have some inbuilt weaknesses. Equity

contributions are only as good as the market valuations they are based

on. As US equities are arguably overpriced, sponsors are having to pay

more than they historically would have to purchase a company. If

price/earnings ratios revert to lower levels, company valuations will

fall wiping out some of the equity cushion and making the debt a higher

proportion of the enterprise value....MUCH MORE

HT:

ZeroHedge