"There has got to be a way to short this"Reiterated in 2016

"It has been a long cherished dream to figure out a way to bet against this one, links below...."And now it seems everyone is a junior analyst, snarking and poking fun, in an oh-so-superior-style, but you know what I haven't seen from all the drive-by raconteurs?

A plan to answer that 2015 question.

From ZeroHedge:

With the WeWork IPO roadshow expected to start as soon as next week as the company's bankers feel a sense of growing urgency to take the company public asap in the aftermath of such recent bombs as Uber, Lyft, Chewy and most recently, Slack, which crashed yesterday wiping out all post-IPO gains, there was one big piece of the puzzle that was still missing: at what valuation would WeWork go public?

Now, according to Bloomberg, we know, with Bloomberg reporting that the New York-based office-rental startup whose lofty mission statement is to "elevate the world's consciousness", is seeking a valuation of about $20 billion to $30 billion in its U.S. initial public offering.

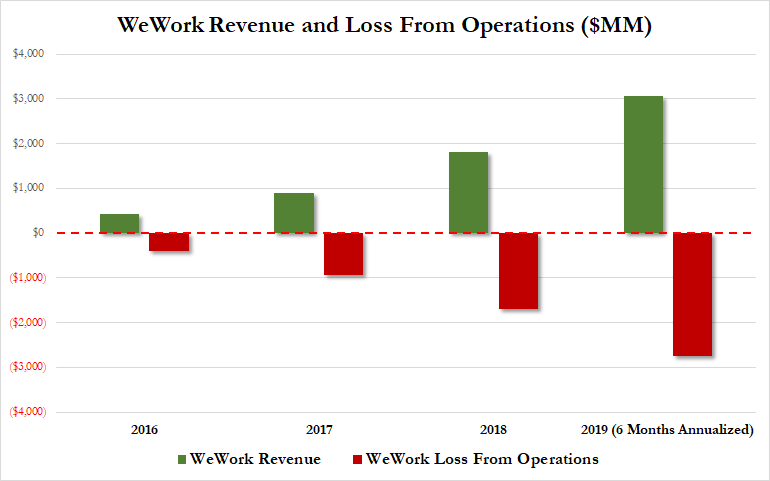

Considering that WeWork generated $1.54 billion in revenue in the first six months of 2019 and posted a net loss of $904 million, while losing an insane $1.4 trillion from operations, that would make the upper end of the range roughly 10x on sales and idiotic on a cash flow, EBITDA, or profit basis.

What is even more remarkable about this valuation is that it represents a massive haircut to the company's latest private founding round: as a reminder, WeWork It started at a $97 million valuation with its Series A in 2009, and by its Series C in 2011, investors had valued the co-working behemoth at $4.8 billion, according to Craft, a website that tracks corporate financial data.....MORE

By 2015, WeWork’s valuation had reached $16 billion. Four billion dollars from Softbank last year boosted WeWork into $40 billion territory, and the funding round in January brought it to $47 billion.

In other words, at the $20 billion, low-end valuation, WeWork would be taking an almost 60% discount to the latest idiotic valuation round led by, who else, venture capital's equivalent of "throw shit at the wall and see what sticks while revaluing the shit higher with every toss", SoftBank....

We'll have more after the IPO.

For now, love and understanding for our analyst brethren, because who among us is without the sin of snark, casting the first stone, in glass houses, etc,

A post from 2017:

WeWork:“Our valuation and size today are much more based on our energy and spirituality than it is on a multiple of revenue."We too have succumbed to the siren song of of imagined superiority.

Roger that, energy and spirituality. Over....