I don't exactly know what to think of Mr. Verleger, link below.

Most active June WTI $60.57, up 7 cents; front month Brent up $0.39 at $67.20.

From FT Alphaville:

The curious incident of the missing super contango in the night-time

A quick post to update readers on an interesting debacle that occurred in the world of oil stock data analysis this week.

Philip Verleger, veteran independent oil analyst, launched a scathing attack on the quality of the EIA’s data on Monday, claiming the agency had been overestimating US output by some 1.6m barrels a day.

The accusations in his note were brutal to say the least:

“The explanation for the mistake indicates a gross dereliction of responsibility on the EIA’s part. Rarely if ever has a US agency charged with collecting data made a miscue of this magnitude. The EIA administrator should be dismissed immediately for gross incompetence.”In Verleger’s opinion, the EIA’s mistake misled analysts about the path of future oil prices, and even potential central banks as well. Verleger himself, for example, had predicted in February that unless production levels decreased substantially, US oil storage capacity would be reached by April-June, making all sorts of alternative storage profitable. (In the US floating storage is not an easy option because of the restrictions of the Jones Act.)

But this never happened. The stock surge instead began to ease off in April, registering drawdowns by May. The contango oil structure, meanwhile — which determines the profitability of storing oil — also began to abate. Most notably, oil prices began to rise not fall.

Verleger, accordingly, set his sights on the fallibility of the EIA data to explain his poor assessment. Soon enough, as luck would have it, he came up with a formula that proved the EIA’s production numbers must indeed be wrong. With evidence in hand he dished out the following conclusion on Monday:

Its failure to report correctly the decline in US oil production has enormous consequences. The rise in oil price, for example, has baffled many who believed global stocks were surging. Global stocks would have done so had DOE’s numbers been correct. Macroeconomists in the US and across the world have been surprised at the strength in prices. It is even possible that central bank policies have been influenced by the error. This is not a trivial mistake. It should not be brushed off lightly. Action needs to be taken immediately.Problem is, as a few quick calls to industry professionals revealed, it was not the EIA but Verleger who had got his sums wrong.

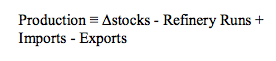

To extrapolate the “true” US production rate, you see, Verleger had used the following equation:

Something he had arrived at by adjusting this original:

Vergeler’s concluding formula can loosely be summarised as production equals stocks MINUS consumption PLUS net imports. Except, as was quickly pointed out by the market, the actual algebra should say that production equals stocks MINUS net imports PLUS consumption.

Good on Verleger though. By Tuesday he had humbly fessed up to the error:

Economists at the Federal Reserve found a flaw in our calculations (see the PDF posted here). To be blunt, we screwed up.But our intention is not to embarrass or draw attention to Verleger’s mea culpa. What we find interesting is that despite all of the above Verleger is still adamant that something remains awry in the oil system.

As his most recent note explained...MUCH MORE (the good stuff)From my introduction and update to a 2013 post, again by Ms Kaminska, this time at her personal blog Dizzynomics:

I have very mixed feeling about Mr. Verleger.

I am naturally suspicious of anyone who spends as much time on self-promotion as he does. On the other hand Craig Pirrong seems to respect him and, although I don't have much interest in Pirrong's snark, the Prof. probably knows as much about commodity storage as anyone.

Storage, being the nexus between physical and financial, is the aspect of the commodity biz that matters most so anyone who can instruct me is jake in my book.

From Dizzynomics:

From the WSJ, a view based on the recent writings of Philip Verleger...MORE...

...Update: A very sharp physical oil trader points out that the above timeframe is rather wide enough to drive a tanker through without touching either side of the bracket and sends along a couple of Mr. Verleger's public predictions:So who knows?

From Bloomberg:

Verleger Sees $20 Oil This Year on ‘Devastating’ Glut (Update1)That's dated July 16, 2009 with the front futures at $61.18. Oil had bottomed the previous December at $32.40. and besides not going to $20 it never traded lower than the day of the prediction, closing the year at $79.36....MORE

See also September 2009

Oil market "teetering on the edge," warns Verleger (44% Drop?!)