CORRECTION—Adding the meat of the matter which was inadvertently left out.

Since we are doing five-year anniversaries, here's another, though belated because with over 300,000 items in the link-vault the importance of proper filing becomes critical. Ahem.

A repost with a couple links upfront. The links to the 2019 BlackRock blog entry and the more substantial white paper have either rotted or been removed from the internet. Fortunately they were captured by the Internet Archive:

August 20, 2019: How central banks might deal with the next downturn and August 2019:

Dealing with the next downturn:

From unconventional monetary policy to

unprecedented policy coordination

And the repost, October 15, 2022 (added):

We first posted this on August 21, 2019. That was three months before Covid-19 started filtering into the world's consciousness.*

Three years later it reads like the blueprint for what actually happened.

BlackRock: "How central banks might deal with the next downturn"

When did recessions become equivalent to the bubonic plague?

Reading the news opinions of the last couple weeks you would think the entire world has been sentenced to death or something.

Get a grip.

Everyone over the age of 25 has survived three quite serious recessions.

Those with more ahhh... experience have lived through five of the beasties if over age 40 and seven if age 50.

With that mini-rant out of the way here is Elga Bartsch, the head of

economic and markets research at BlackRock Investment Institute. Her mini-bio says "Dr. Bartsch was Global Co-Head of Economics and Chief European Economist at Morgan Stanley in London"

I have heard of this Morgan and Stanley.

[note, October 15, 2022: not sure why I was comparing recession to "bubonic plague" and "sentenced to death". It must have been something in the air as I was clueless about covid til weeks later.]From the BlackRock blog:

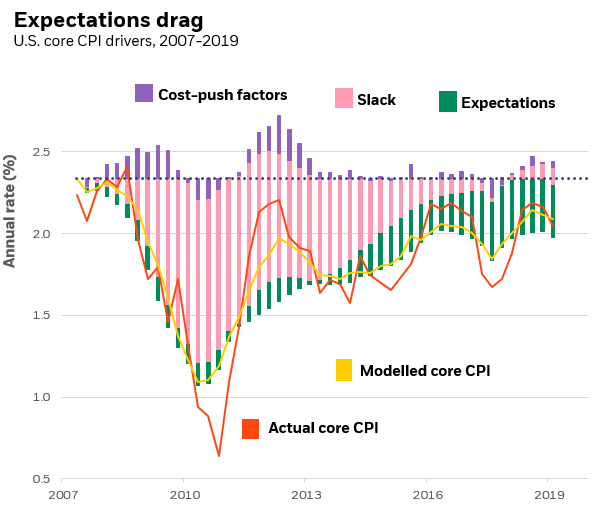

Unprecedented policies will be needed to respond to the next economic downturn. Monetary policy is almost exhausted as global interest rates plunge toward zero or below. Inflation expectations are dragging on actual inflation. See the chart below.

Fiscal policy on its own will struggle to provide major stimulus in a timely fashion given high debt levels and the typical lags with implementation. Without a clear framework in place, policymakers will inevitably find themselves blurring the boundaries between fiscal and monetary policies. This threatens the hard-won credibility of policy institutions and could open the door to uncontrolled fiscal spending.

Sources: BlackRock Investment Institute, with data from Refinitiv Datastream, August 2019. Notes: This chart shows the actual change in the annual rate of U.S. core inflation and estimates of the contributions of various economic drivers. The factors are broken down by percentage point of contribution to the overall implied Phillips curve inflation from the starting point in 2007. The implied Phillips curve estimates are partly based off the August 2013 paper The Phillips Curve is Alive and Well. Instead of modelling inflation expectations via lags we use the measure of inflation expectations similar to the 2010 paper Modeling Inflation after the Crisis.

In our new paper, “Dealing with the next downturn,” we outline the contours of a framework to mitigate this risk so as to enable an unprecedented coordination through a monetary-financed fiscal facility. Activated, funded and closed by the central bank to achieve an explicit inflation objective, the facility would be deployed by the fiscal authority.

Below are the main highlights from the paper. Further blogs will go into more detail on the crucial points.

- There is not enough monetary policy space to deal with the next downturn: The current policy space for global central banks is limited and will not be enough to respond to a significant, let alone a dramatic, downturn. Conventional and unconventional monetary policy works primarily through the stimulative impact of lower short-term and long-term interest rates. This channel is almost tapped out: One-third of the developed market government bond and investment grade universe now has negative yields, and global bond yields are closing in on their potential floor. Further support cannot rely on interest rates falling.

- Fiscal policy should play a greater role but is unlikely to be effective on its own: Fiscal policy can stimulate activity without relying on interest rates going lower – and globally there is a strong case for spending on infrastructure, education and renewable energy with the objective of elevating potential growth. The current low-rate environment also creates greater fiscal space. But fiscal policy is typically not nimble enough, and there are limits to what it can achieve on its own. With global debt at record levels, major fiscal stimulus could raise interest rates or stoke expectations of future fiscal consolidation, undercutting and perhaps even eliminating its stimulative boost....

....MORE

The link in the original post has rotted, as has the link to the graph.

https://www.blackrock.com/us/individual/insights/how-central-banks-might-deal-with-the-next-downturnAnd here is the much more complete 16 page PDF

https://www.blackrock.com/corporate/literature/whitepaper/bii-macro-perspectives-august-2019.pdf

May you live in interesting times.

The key points from the 2019 White Paper:

•An unprecedented response is needed when monetary policy is exhausted and fiscal policy alone is not enough. That response will likely involve “going direct”: Going direct means the central bank finding ways to get central bank money directly in the hands of public and private sector spenders. Going direct, which can be organised in a variety of different ways, works by: 1) bypassing the interest rate channel when this traditional central bank toolkit is exhausted, and; 2) enforcing policy coordination so that the fiscal expansion does not lead to an offsetting increase in interest rates.

• An extreme form of “going direct” would be an explicit and permanent monetary financing of a fiscal expansion, or so-called helicopter money. Explicit monetary financing in sufficient size will push up inflation. Without explicit boundaries, however, it would undermine institutional credibility and could lead to uncontrolled fiscal spending.*I think the story that grabbed my attention was from China's Global Times, January 1, 2020:

Police in Central China's Wuhan arrested 8 people spreading rumors about local outbreak of unidentifiable #pneumonia. Previous online posts said it was SARS

http://web.archive.org/web/20200107195600/https://twitter.com/globaltimesnews/status/1212409846684884995

But credit where credit is due, recognition that the story was important was probably kindled by some of ZeroHedge's posts in December 2019 that had filtered into the subconscious.

If interested see also: