First up Izabella:

Dollar strength exposures are not what you think

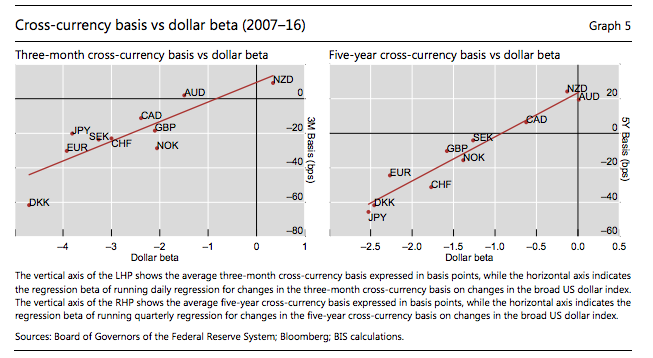

Earlier on Tuesday we highlighted the latest research from the Bank for International Settlements on the impact of the worldwide dollar shortage on cross-border banking and capital markets.

We showed you a number of charts, but we held two very specific ones back because we didn’t want their significance to be buried in the weight of an 1800-word piece.

Below is what really matters:

As the BIS economists explain:And coming in off the top rope David adds:

The left-hand panel plots the CIP deviation for a currency at the three-month horizon against the dollar beta for that currency using daily price changes. The right-hand panel shows the five-year CIP deviation using quarterly price changes. In both cases, there is a striking positive, linear relationship. In effect, the dollar is a risk factor which “prices” the CIP deviation. The correlation is 85% for the three-month basis and 97% for the five-year basis.Insofar as deviations from covered interest parity (the y-axis) can be explained by the inability of banks to take risk and fund currency swaps, the charts essentially show the sensitivity of countries’ currencies in the rest of the G10 to changes in the value of the dollar....MORE

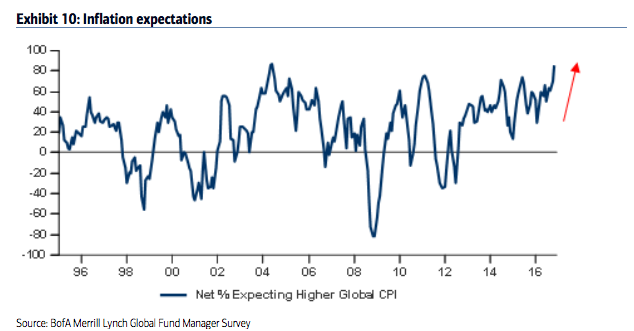

Inflating inflation expectations

It’s coming…

“Global inflation expectations soar to highest % since Jun’04 (net 85% from net 70% last month),” says BofA’s monthly fund manager survey.

While the “highest % of investors since Aug’13 think yield curves will steepen over the next 12 months (net 65% from net 31% last month).” Apparently the biggest MoM jump on record....MORESee also the post immediately preceding:

US Dollar Index: To Infinity and Beyond! (DXY)