She doesn't have time to get into it in the present post but the role of the central banks in inflating the net worth of the 200* richest people on the planet is really quite amazing.

*# 200 gets you down to about $6.5 billion, give or take.

From FT Alphaville:

Interest rate hikes are bad news for cultural rent seekers

A funny thing happened this decade.

The fairly logical-minded world of computer science stumbled into the world ofalchemical cult value by way of the cryptocurrency phenomenon, and didn’t even realise they’d taken leave of their senses. And still don’t.

For some, the discovery has been something akin to a religious experience. Question ‘Satoshi’ and the kingdom of the eternal blockchain, and well, just see this.

Artists, of course, have been at this game for a whole lot longer. And been way more efficient about it.

No fancy computer servers needed for their money-printing operations, just some palette knives, some canvases and some oils. Even talent — which used to be the difficulty factor that kept their store-of-value unit scarce — has long been abandoned.

Today it’s an informal Artist FOMC committee which both controls supply and stimulates demand via the sanctioned dealer and auction network.

So what’s the outlook for cartel art in the lead up to a lift-off in interest rates and a contraction of in the flow of international eurodollars, especially from China?

According to Citi’s latest deep dive into the art market by way of its Global Perspectives and Solutions report, not as good as it was just a few years ago.

From the report:

Will the robust growth of the 2000s continue? We argue that it likely won’t, or at least that a different adjective is in order: ‘solid’ instead of ‘stellar’ growth, ‘balanced’ not ‘burgeoning,’ and so on. The reason for the downgrade is that the sources of growth in the market since 2000 may not prove as durable as many observers believe.Rather, the narrative that emerges from the performance of the market since 2000 is one of structural one-offs that have given rise to considerable – though ultimately temporary – support for the market’s trajectory.

You won’t be surprised to find out that one of those structural one-offs has of course been China, which has muscled its way into the artist FOMC system:

As Citi notes, it’s the US/UK/China triad (nice choice of wording) which now dominates the auction market:

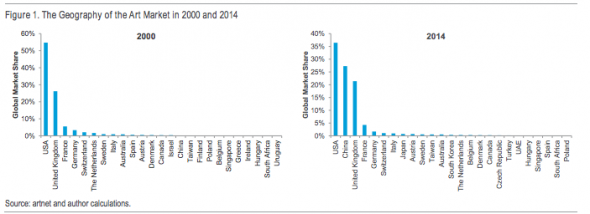

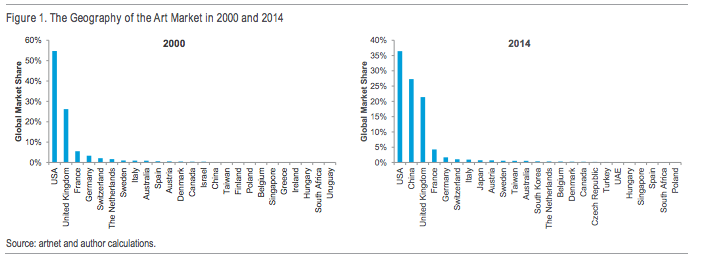

The first structural change is the forceful entry of China into the global market. As is plain to see in Figure 1, the geography of the global auction market is highly concentrated in a few locations. In 2000, over half of auction sales by dollar value took place in the US, with an additional quarter in the UK. France, the third largest market, accounted for just over 5 percent, and so forth. Back in 2000, auction sales in China were essentially a rounding error in the global auction market statistics.

Fast forward to 2014. Seven of the incumbent sales locations from 2000 still appear among the top 10 markets by size, with one stark difference. China now accounts for a third of global growth and, at $4.4 billion, now claims over a quarter of global sales and the number two spot behind the United States. Compared to the US/UK duopoly in 2000 which presided over 80 percent of auction sales, the US/UK/China triad now accounts for 85 percent. Moreover, the ascent of China has radiated widely throughout the global market. Seventeen of twenty nine countries where auction sales took place in 2000 experienced a decline in market share in the wake of China’s rapid ascent.

This has been the equivalent of a coup for China, hence why Citi notes that the upshot to China’s dominant contribution to global sales growth is that the performance is unlikely to be repeated in the coming years....MORE