From MacroBusiness (Australia):

Deutsche has an interesting note weighing up whether or not BHP and

Rio should pull back or continue to invest in new production today. It

concludes:

The big miners are now focused on maximising cash flow

through cost cutting and delivering brownfield expansions. This strategy

should deliver benefits near term however over the long run additional

projects will need to be approved in order to meet growing demand.

Beyond what has been approved, BHPB and Rio have a number of high

returning growth projects that should create value and increase cash

flow over the long run. For Rio these include Pilbara 360 and the Oyu

Tolgoi underground and for BHPB Spence hypogene, and further growth in

the Pilbara, the GoM and US Onshore (see pages 9-15 for the full list).

Despite the markets concerns over further production growth we think

that the diversified miners can continue to invest and grow dividends at

the same time. However in order to add substance to the debate we have

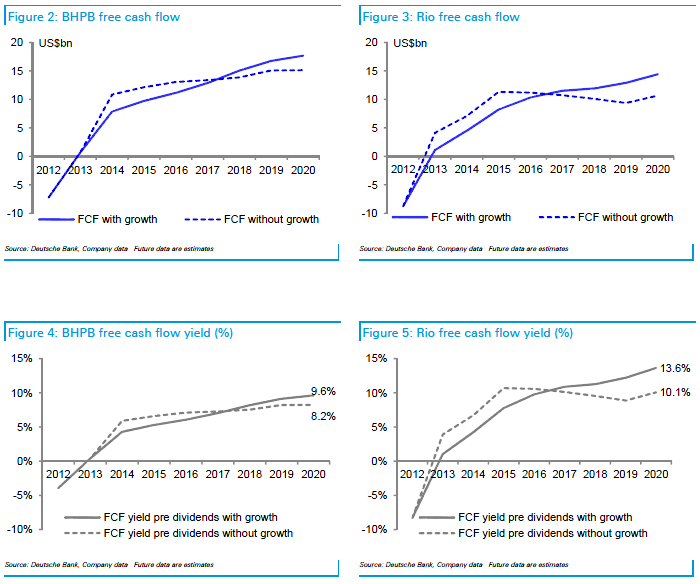

run a scenario where we look at BHPB and Rio Tinto without future

production growth beyond those projects already approved (see Figure 1).

The delta is significant. Removing high returning growth reduces

valuations by c. 15% to around where the stocks are currently trading.

Free cash flow yields (post capex and before dividends) would increase

over the next three years by around 2% points or US$3b per annum if

growth is delayed, however BHPB’s free cash flow and earnings would

decline by 10-15% beyond 2016 and Rio’s by 25- 30%. In our view, the key

question is whether management should delay high returning growth in

order to maximise near term free cash flow and potentially dividends,

however at the expense of value and future cash flow.

So that’s pretty clear then. Let’s face it, we are largely talking about iron ore here, especially for Rio...MORE