A reasonably good account of the impact of the Black Scholes equation. Despite the rather dramatic title of the article, the equation did not cause the market crash.

For my MBA 523 students - you need to read this. We're talking about the derivation of the Black Scholes model this week!

From The Guardian:

The Black-Scholes equation was the mathematical justification for the trading that plunged the world's banks into catastrophe

The Black-Scholes equation was the mathematical justification for the trading that plunged the world's banks into catastrophe

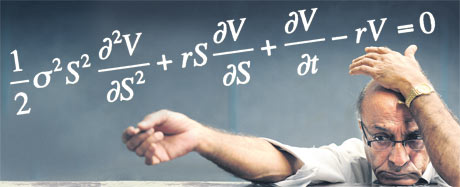

In the Black-Scholes equation, the symbols represent these variables: σ = volatility of returns of the underlying asset/commodity; S = its spot (current) price; δ = rate of change; V = price of financial derivative; r = risk-free interest rate; t = time. Photograph: Asif Hassan/AFP/Getty ImagesIt was the holy grail of investors. The Black-Scholes equation, brainchild of economists Fischer Black and Myron Scholes, provided a rational way to price a financial contract when it still had time to run. It was like buying or selling a bet on a horse, halfway through the race. It opened up a new world of ever more complex investments, blossoming into a gigantic global industry. But when the sub-prime mortgage market turned sour, the darling of the financial markets became the Black Hole equation, sucking money out of the universe in an unending stream.Anyone who has followed the crisis will understand that the real economy of businesses and commodities is being upstaged by complicated financial instruments known as derivatives. These are not money or goods. They are investments in investments, bets about bets. Derivatives created a booming global economy, but they also led to turbulent markets, the credit crunch, the near collapse of the banking system and the economic slump. And it was the Black-Scholes equation that opened up the world of derivatives.The equation itself wasn't the real problem. It was useful, it was precise, and its limitations were clearly stated. It provided an industry-standard method to assess the likely value of a financial derivative. So derivatives could be traded before they matured. The formula was fine if you used it sensibly and abandoned it when market conditions weren't appropriate....MORE

Fischer Black died in 1995 and so wasn't around in 1997 when Myron Scholes and Robert Merton were awarded the Nobel Memorial Prize in economics.

Scholes and Merton had gone from success to success including the foundiing, in 1994, of Long Term Capital Management.

The subsequent disaster pointed up the importance of risk management and inadvertantly supplied evidence to support the Peter Principle.