Following on July 17's "Yield Curve Control Means The Party Can Continue, What's Not To Love?", a related concept from Real Investment Advice, July 10:

As quoted below from an executive summary of a joint report by the Department of Treasury and the Office of Management and Budget (OMB), the current deficit policy is deemed unsustainable. However, they fail to mention how long the Fed, via fiscal dominance, can sustain the unsustainable.

“The debt-to-GDP ratio was approximately 97 percent at the end of FY 2023. Under current policy and based on this report’s assumptions, it is projected to reach 531 percent by 2098. The projected continuous rise of the debt-to-GDP ratio indicates that current policy is unsustainable.” – Financial Report of the United States Government -February 2024.

Fed speakers will deny any notion that its monetary policy aims in part to help the government fund her debts. Regardless of what they say, we are already in an age of fiscal dominance. Monetary policy must consider the nation’s debt situation.

Fiscal Dominance

Fiscal dominance is a condition whereby the amount of debt in an economy reaches a point where monetary policy actions must allow Federal debts and deficits to be serviced and funded cost-effectively. By default, such monetary policy decisions will often come at the expense of traditional employment and price goals. As a result, the Fed must further distort the price of money and ultimately lessen the wealth of the nation’s citizens.The age of fiscal dominance is here. Consider the following paragraphs and graph from our article Stimulus Today Costs Dearly Tomorrow.

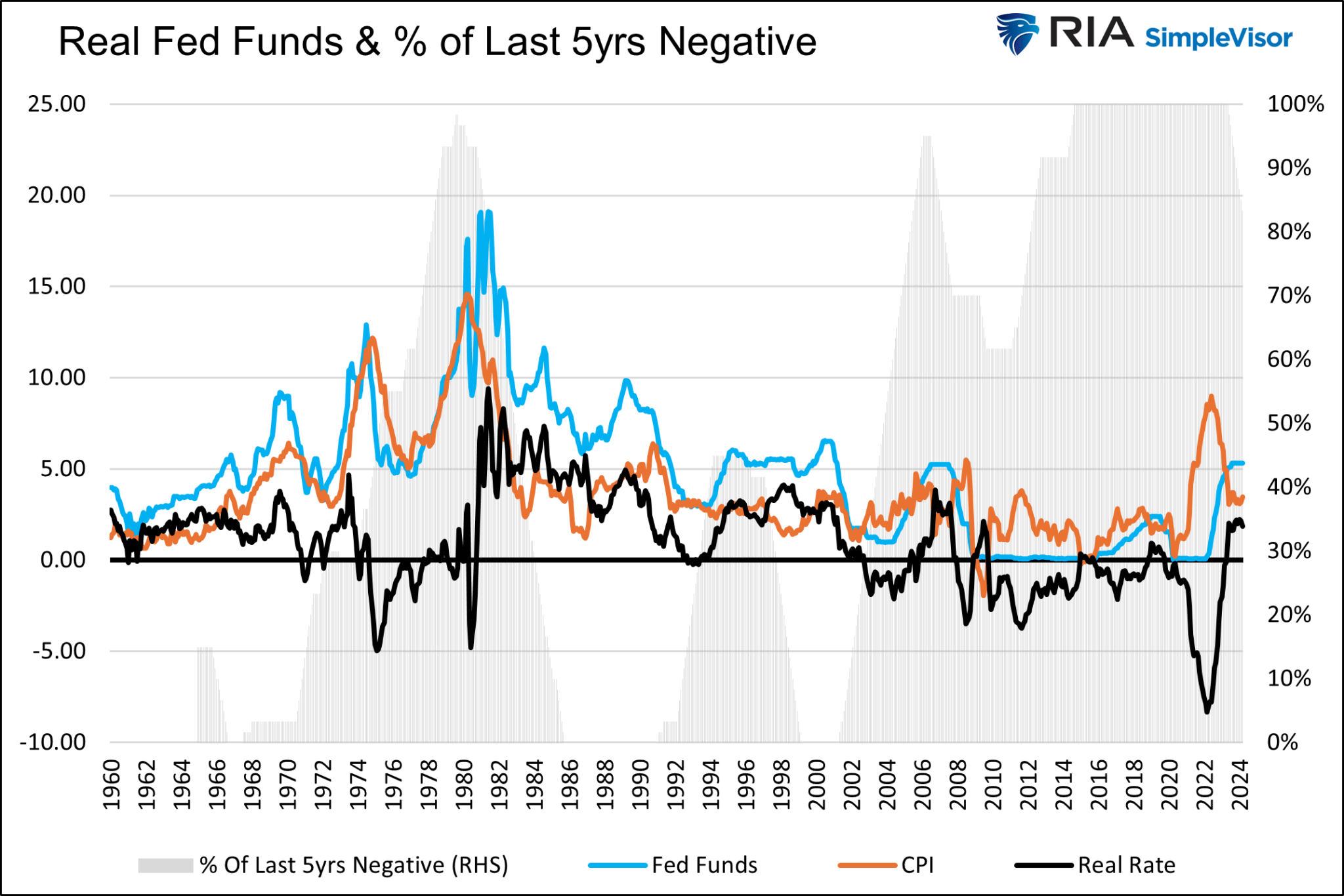

A lender or investor should never accept a yield below the inflation rate. If they do, the loan or investment will reduce their purchasing power.

Regardless of what should happen in an economics classroom, the Fed has forced a negative real rate regime upon lenders and investors for the better part of the last 20+ years. The graph below shows the real Fed Funds rate (black). This is Fed Funds less CPI. The gray area shows the percentage of time over running five-year periods that real Fed Funds were negative. Negative real Fed Funds have become the rule, not the exception.

Soaring Debt Outstanding and Rising Rates

The government has added $2.5 trillion in debt over the last four quarters. Of that, over $1 trillion was to pay its interest expenses on the entire debt stock. Despite recent high interest rates, the average interest rate on the debt is still relatively low at 3.06%.The two graphs below show why a relatively minimal uptick in the average interest rate on the debt is so troublesome. The federal debt (blue) has grown by 8.5% annually over the last ten years. Despite the amount of debt more than doubling over the period, the interest expense on the debt until very recently has remained very low. The first graph shows that the average interest rate increase is barely visible. However, the second graph shows that the rise in the government’s interest expenses is substantial.

As debt issued years ago with low interest rates matures and new debt with higher interest rates replaces it, the interest expense will keep rising. For context, if we assume the government’s average interest rate is 4.75%, likely close to their weighted average rate on recent debt issuance, the interest expense will rise to $1.65 trillion, not including new debt.

$1.65 trillion is over $300 billion above the government’s next largest expenditure, Social Security. Furthermore, it is double defense spending for 2023. The annual federal deficit has only been above $1.65 trillion twice (2020 and 2021) since its founding in 1776.

While the situation may sound gloomy, lower interest rates solve the problem. If interest rates return to the levels existing before 2022, the interest expense could easily fall below $700 billion, about half of the cost than if rates remain at current levels.

Therefore, interest rates will have to be kept in check by the Fed.

The Fed Understands Their Role....

....MUCH MORE

This is what Albert Edwards was referring to in the tweet linked in "Société Générale's Albert Edwards On The Endgame".

Related, April 2024:

Since Yield Curve Control Is Coming Back We Should Probably Brush Up On How It Worked In The U.S.Sticking with the Fed for another post and working on the assumption that at some point, maybe a couple years out, buyers of U.S. Treasury paper will begin to demand more interest than the Treasury can afford to pay (forcing the Fed back into the market on a net basis) here are a couple articles that may be of interest, so to speak....