"... Warns of 'Unpredictable Consequences' to Banks"

From Wall Street on Parade, May 31:

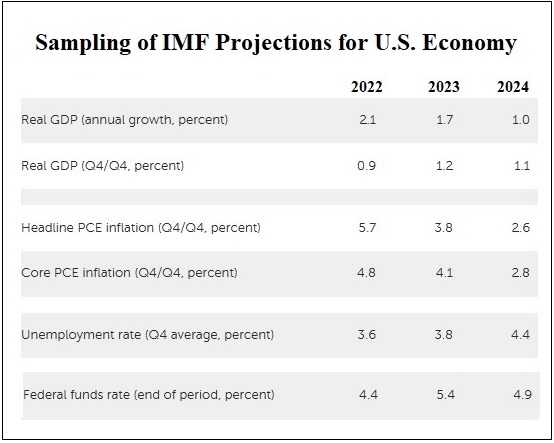

Last Friday, at the start of Memorial Day weekend, researchers at the International Monetary Fund (IMF) released an analysis of where they think the U.S. economy is headed and the headwinds (read gale force winds) that can, potentially, be expected along the way.

Folks on Wall Street who were hoping that the Fed was at the end of its rate-hiking cycle, with a more dovish Fed juicing stock market returns later this year, likely had their holiday weekend ruined with this projection from the IMF:

“Achieving a sustained disinflation will necessitate a loosening of labor market conditions that, so far, has not been evident in the data. To bring inflation firmly back to target will require an extended period of tight monetary policy, with the federal funds rate remaining at 5¼–5½ percent until late in 2024.”

The Fed’s inflation target is 2 percent. As of its last report on May 10, the U.S. Bureau of Labor Statistics reported that the Consumer Price Index rose 0.4 percent in April on a seasonally-adjusted basis while the all-items index increased 4.9 percent over the last 12 months before seasonal adjustment.

The Fed’s inflation target of 2 percent remains elusive despite the fact that the Fed began its rate hikes more than a year ago on March 17, 2022 and has hiked rates 10 times – the fastest pace in 40 years. The Fed Funds rate has moved from 0-0.25 percent on March 16, 2022 to the current 5.0-5.25 percent, the highest level for Fed Funds in more than 15 years.

While the Fed has not cracked the tight labor market or inflation conundrums with its rapid rate increases, it has produced serious cracks in the banking system. Between March 10 and May 1 of this year, the second, third and fourth largest bank failures in U.S. history occurred: First Republic Bank, Silicon Valley Bank, and Signature Bank, respectively. (Washington Mutual was the largest bank failure in 2008.)

Thus, it is no surprise that the condition of the balance sheets of banks in the U.S. received a significant amount of attention in the recent IMF report – as did the timidity of federal regulators to do anything more than destroy a forest of trees interminably writing warnings to troubled banks while taking no concrete action. The IMF researchers write:

“First, a higher path for interest rates could reveal larger, more systemic balance sheet problems in banks, nonbanks, or corporates than we have seen to-date. Unrealized losses from holdings of long duration securities would increase in both banks and nonbanks and the cost of new financing for both households and corporates could become unmanageable.”....