S&P 500 close August 17: 4,274.04

The writer, Michael Lebowitz, knows this stuff but he or whoever wrote their headline errs in the "...If QT Continues" bit. As we've been chronicling since the alleged June 1 start date, it hasn't even begun. $35 billion from an $8.9 trillion balance sheet is literally a rounding error.

Otherwise he is right on the money with the interplay of reverse repo (remember our repo/reverse repo fixation from a couple months ago?) the Fed's balance sheet and the Treasury General Account which we were going to cover if the Fed ever got going.

From Real Investment Advice, August 17:

S&P 3500 By Year End If QT Continues

“Don’t Fight the Fed” echoes through the financial media, Wall Street, and in the minds of retail and institutional investors. The phrasing pertaining to Fed-generated liquidity is often the sole basis for investors to chase bull markets when the Fed employs easy monetary policy. Unfortunately, some investors forget the phrase is equally meaningful when the Fed is not friendly to markets. As we share in this article, we have developed a model to track Fed liquidity, allowing us to quantify the Fed’s influence on the S&P 500.

Before unveiling our liquidity formula and its forecast for the S&P 500, it’s essential to discuss the three primary drivers by which the Fed is influencing liquidity: Reverse Repurchase (RRP), Treasury General Account (TGA), and the Fed’s balance sheet.

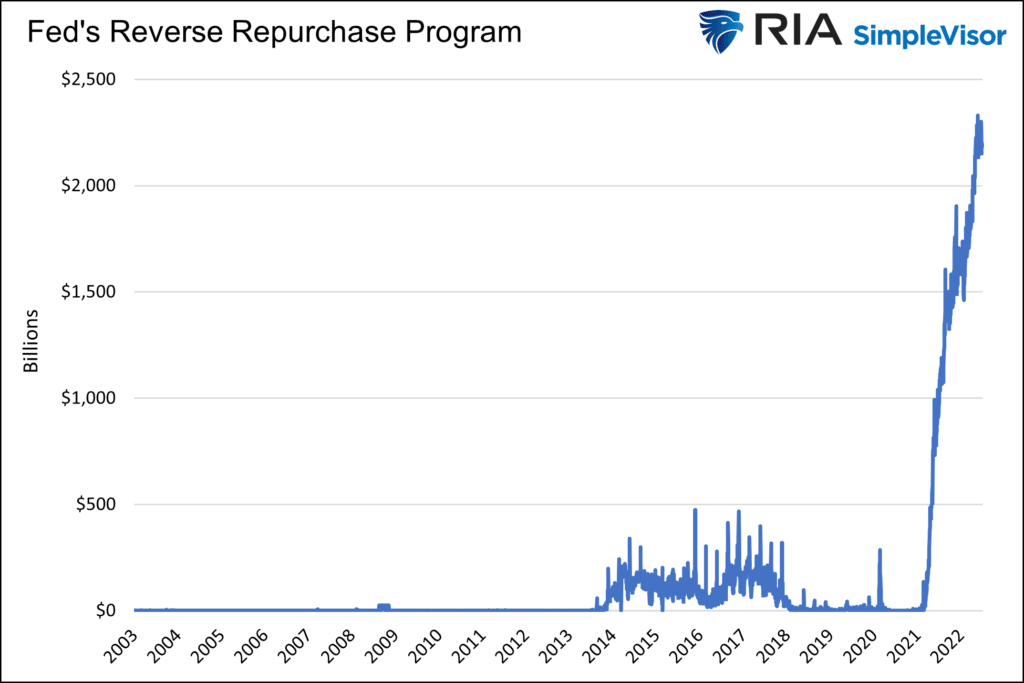

Reverse Repurchase Agreements (RRP)The New York Fed uses numerous repo programs to manage the supply of cash in the banking system, thereby maintaining the Fed Funds rates within the FOMC’s target range. Currently, they are employing its RRP program to accomplish this task. In an RRP transaction, the Fed sells securities to a counterparty and simultaneously agrees to repurchase them at a future date. The duration is often overnight. The transaction temporarily reduces the supply of money from the banking system. Increasing daily RRP balances results in less system liquidity, and a declining balance reduces liquidity.As shown below, RRP has been around for 20 years but was scarcely used until early 2021. The various pandemic-related rounds of fiscal stimulus and massive Fed liquidity efforts left banks and money market funds with excessive levels of cash. The excess liquidity would have pushed the Fed Funds rate lower than the target rate without the RRP program. As such, RRP sucks up liquidity, making Fed Funds easier for the Fed to manage.

The Fed has other repo tools, such as repurchase agreements and the standing repo facility, which can dampen money market rates by providing the banking system with liquidity.

The RRP facility has been increasing rapidly and now sits at over $2 trillion daily. Rising RRP balances are a drain on liquidity.

As money market yields rise with Fed Funds and asset markets perform poorly, investors tend to prefer higher cash balances. Such should keep RRP levels elevated for the time being.

Treasury General Account (TGA)....

....MUCH MORE

Yesterday's release of the July 26 - 27 FOMC minutes contained this paragraph (emphasis ours):

Participants concurred that, in expeditiously raising the policy rate, the Committee was acting with resolve to lower inflation to 2 percent and anchor inflation expectations at levels consistent with that longer-run goal. Participants noted that the Committee's credibility with regard to bringing inflation back to the 2 percent objective, together with its forceful policy actions and communications, had already contributed to a notable tightening of financial conditions that would likely help reduce inflation pressures by restraining aggregate demand. Participants pointed to some evidence suggesting that policy actions and communications about the future path of the federal funds rate were starting to affect the economy, most visibly in interest-sensitive sectors. Participants generally judged that the bulk of the effects on real activity had yet to be felt because of lags associated with the transmission of monetary policy, and that while a moderation in economic growth should support a return of inflation to 2 percent, the effects of policy firming on consumer prices were not yet apparent in the data. A number of participants posited that some of the effects of policy actions and communications were showing up more rapidly than had historically been the case, because the expeditious removal of policy accommodation and supporting communications already had led to a significant tightening of financial conditions....

I'll have to go back and check the veracity of the "...significant tightening" line but do know for the weeks ending August 5 and August 12 financial conditions have loosened.

The reason for doubting that line is you don't get stock market rallies of the magnitude we've just seen in the face of "significant tightening."