The Federal Reserve's Explanation Of What Happened In The Money Markets In September 2019

For now this is just a personal bookmark but we may be referring back to it. What was going on in Q3 and Q4 2019 was a big enough deal that the Fed felt compelled to publish this little bit of narrative.

What seems to have happened was that somebody's derivative book got upside down to the tune of a few trillion dollars (notional, always say notional) and in addition the contagion through the counterparty daisy chain was also in the trillions and well, here's the Fed with their version.

From the Board of Governors of the Federal Reserve System:

In mid-September 2019, overnight money market

rates spiked and exhibited significant volatility, amid a large drop in

reserves due to the corporate tax date and increases in net Treasury

issuance. Although some upward pressure on money market rates due to

these seasonal factors was expected, the extent of the increase in both

the level and volatility of rates in secured and unsecured markets was

surprising. In this note, we review the money market events of September

2019 and discuss the factors that may have contributed to the sharp

rate movements in the repo market and the associated pressures in the

fed funds market.

What happened?

The moves in both secured and unsecured rates on September 16 and 17

were much larger than any of those observed over the past few years.

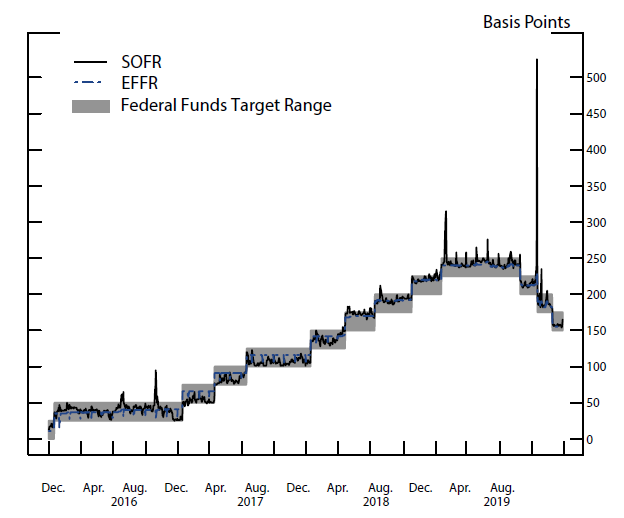

Figure 1 shows the effective federal funds rate (EFFR) and the secured

overnight financing rate (SOFR), a broad measure of the cost of

borrowing cash overnight collateralized by Treasury securities, since

December 2015. The EFFR has been quite stable and only printed outside

the FOMC's target range on one day before September 17. While SOFR has

been more volatile compared to the EFFR and exhibited some quarter-end

seasonality, it rarely moves more than 20 basis points on a day.

Figure 1: SOFR and EFFR

Source: Data available on FRBNY public website. Note: Daily prints of SOFR and EFFR from December 1, 2015 to September 30, 2019. Accessible version

On Monday, September 16, SOFR printed at 2.43 percent, 13 basis

points higher than the previous business day. With pressures in the repo

market spilling over into the fed funds market, the EFFR printed at

2.25 percent, 11 basis points above the Friday print and at the top of

the FOMC's target range. On September 17, the EFFR moved above the top

of the target range to 2.3 percent and the SOFR increased to above 5

percent.

Figures 2 and 3 show the shift in the distribution of trades in the

repo market and the fed funds market, respectively. On September 16 and

17, the range of trades in both markets expanded significantly and rates

shifted higher. Following the repo operations by the Federal Reserve

Bank of New York (FRBNY), announced on September 17, the distribution of

rates in both markets reverted closer to the average distributions

observed over the year the next day....

I have a feeling that lands somewhere in "the nebulous region between mere suspicion and probable cause"

(LaFave & Israel on U.S. v. Ramsey, 431 U.S. 606 [1977])

that there is some sort of misdirection going on that I'm not understanding.

If

so, any attempt at analysis of Fed policy and market moves by

traditional means, global macro, central bank policy and practice,

market internals such as options gamma etc., etc. is just so much

blather.

And I keep coming back to the 3rd and 4th quarters of 2019 as the period when things were getting very weird.