A topic we've looked at so often I bore myself, links after the jump.

Our boilerplate mini-bio::

...The author of this piece, David Goldman, is Deputy Editor (Business) at Asia Times.

Prior to taking that position he was:

- Global head of credit strategy at Credit Suisse

- Global Head of Fixed Income Research for Bank of America

- Global Head of Fixed Income Research at Cantor Fitzgerald

In addition to apparently not being able to hold onto a job I think one of his requirements for moving on was a "Global Head" title. (JK, young Master. G.)

From the Asia Times, October 13 (I believe the was published prior to the U.S. CPI print):

At some point the Fed will have to do what it has done so many times: tighten monetary policy and reduce demand

The 1980s called. They want their economy back.

The S&P 500 has lost about 4% since its September 2 peak and the Nasdaq 100 has lost about 6%. It probably will get a lot worse. Every survey of inflation shows that price pressures on businesses have jumped to levels last seen in 1980, at the tail end of the great stagflation. Today it was the National Federation of Independent Business, which reported that price pressures on businesses as well as plans to raise prices had reached levels not seen in more than forty years.

It’s going to get worse fast. Two-fifths of the US Consumer Price Index reflects the cost of shelter, and rents are rising at the fastest rate in history – by 15% during the year through September, according to the Internet broker Apartmentlist.com.

The United States has never seen numbers like this. They stem from a national shortage of apartments and the lowest vacancy rate on record, at around 6%. Because leases take time to expire, the huge increases in rents reported by private surveys haven’t turned up in the government data yet. Over the next two years, though, a 15% jump in rents will work its way through the official data. That means an additional 3 percentage points of inflation is built into the numbers for the next two years, ensuring that the inflation rate will be well in excess of 5%....

....MUCH MORE

In the just released CPI report the shelter component - weighted at 32.55% of the index only showed a 3.2% increase while the monthly figure, 0.3% annualizes out to a 3.7% rate. Neither figure seems to reflect reported rents.Rent of Primary Residence was reported at 2.4% YoY and 0.4% MoM while Owner's Equivalent Rent printed at 2.9% and 0.4% respectively. Either something is amiss in the BLS methodology resulting in failure to capture actual real-world price increases for shelter or there is an awful lot of increase building up for the next 24 -36 months of reports.

As to pricing equities under various inflation regimes here is a repost from May 2018.

note: although it may require a couple seconds to take in the scatter plot that Crestmont uses, it really does convey a lot of information on the relationship between P/E's and inflation rates.

Our next excursion into all of this will be after the New Year to discuss inflation's impact on reported earning (TL;dr it raises them while unit volumes show a very different picture) and the accounting treatment thereof, including the problem of paying real taxes on phantom earnings,

Fascinating stuff, I can hardly wait. Here's the repost:

"No, stocks aren’t a good inflation hedge. Try bonds (really)."

A major caveat for investors trying to hedge inflation with equities: they aren't that correlated once inflation goes above 4% or so. 0-to-4% is the sweet spot. Above 4% you don't want services companies, manufacturers with tangible assets are the place to be.

This is one reason the Berlin market was able to approximate (with a 3-6 month lag) the Weimar hyper-inflation (the other being survivorship bias). The companies the historians track, the big brewers, metalworkers, miners had real assets.

Stocks of service companies without near-monopoly pricing power got crushed like any other long dated asset.

This is a point you won't see anywhere else, at least until the information contained in those dusty old german-language records gets translated....More after today's headline story from FT Alphaville:

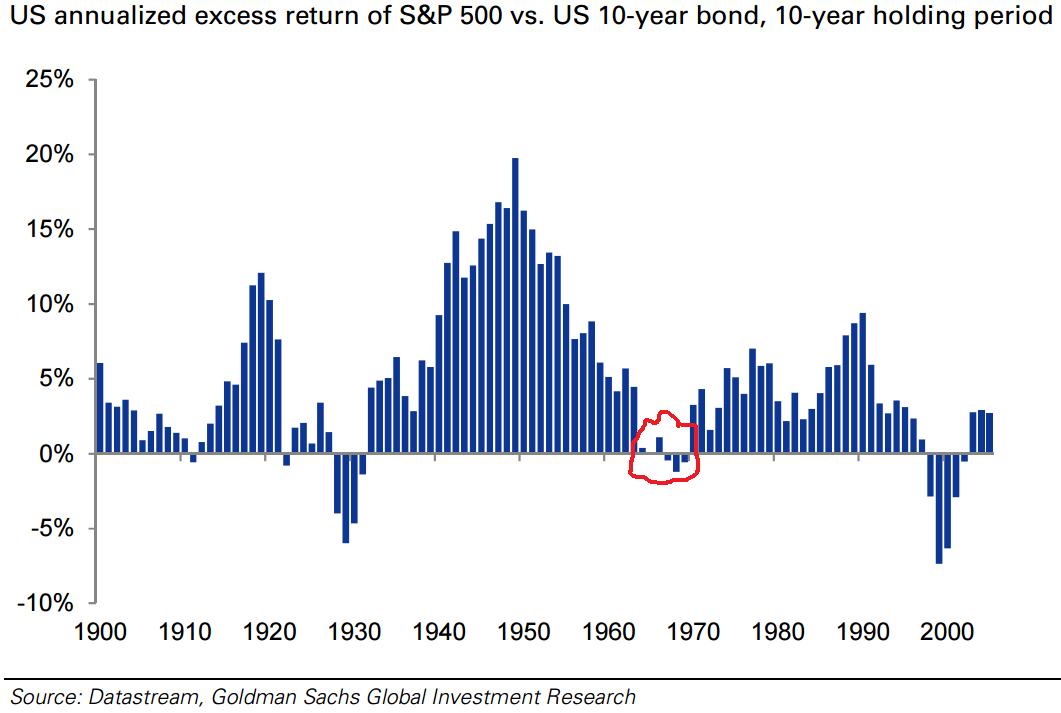

Stocks are basically bonds where the coupons tend to grow faster than the level of consumer prices. That makes equities sound like a great thing to own if you’re worried about inflation, and, in fact, Mr Stocks-for-the-Long-Run made this case a few years ago. While the actual article is more nuanced than the headline and opening paragraph would suggest — he admits that stocks only become immune to inflation over multi-decade periods — it’s still a bit misleading. The last time the rich world had to deal with meaningful inflation, it was bonds that beat stocks.

We’re reminded of all this because of two striking charts from a new report from Goldman Sachs on the implications of negative, long-term real interest rates. Consider the following chart, which compares the returns you would have gotten from buying and holding US stocks versus US 10-year bonds over decade-long periods:From "Crestmont Research on Inflation, P/E's and Market Returns":

If you had known that the US was about to experience a long period of accelerating inflation, would you have bet on US Treasury bonds over US corporate equities? It certainly doesn’t seem like the right plan, and yet it would have made you money for a surprisingly long time. Stocks were so expensive in the late 1960s that bonds ended up doing okay, at least until Volcker, despite the significant upward drift in interest rates....MUCH MORE

Here's another way to look at the relationship between inflation and P/E's. Note that both the highest inflation and deflation rates correspond with the lowest multiples accorded the earnings:

...MORE

Finally, to reiterate:

A subject near and dear. The sweet spot for P/E ratios is 1.00- 2.00% annual CPI inflation. As you move away from that in either direction multiples drop off pretty fast, to the point that equities are not an optimal investment. You won't believe what the best investments for inflation in the 8-12% and greater than 100% ranges are. I'll write about them if we ever go Weimar....