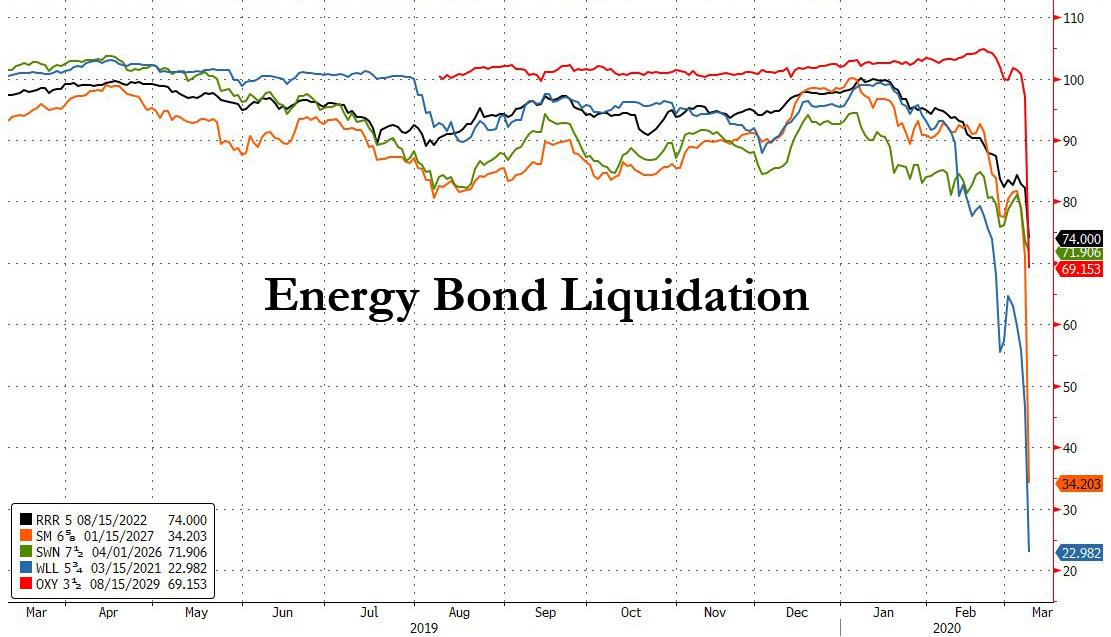

... amid a (long-overdue) investor revulsion to the highly levered

energy sector, much of which is funded in the high yield market, as

crashing oil prices bring front and center a doomsday scenario of mass

defaults as shale companies are unable to meet their debt and interest

payment obligations, investor focus is shifting up the funding chain,

and after assessing which shale names are likely to be hit the hardest,

with many filing for bankruptcy if oil remains at or below $30, the next

question is which banks have the most exposure to the energy loans

funding these same E&P companies.

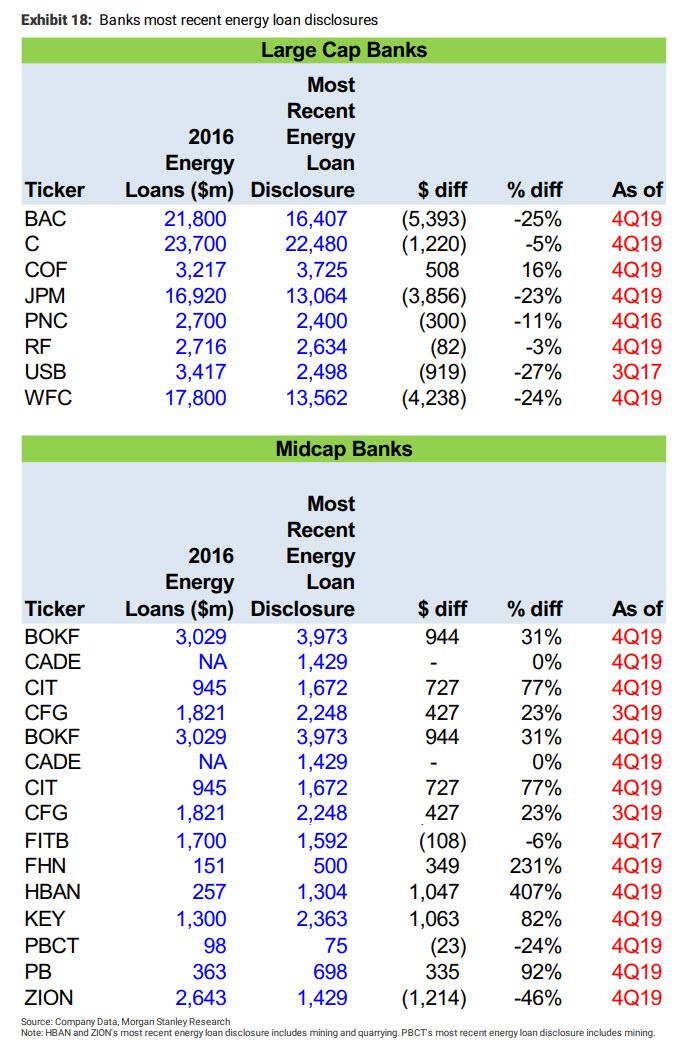

Conveniently, in a note this morning looking at the impact of

plunging interest rates on bank profitability, Morgan Stanley also lays

out the US banks that have the highest exposure to energy in their Q4

loan books.

So without further ado, here are the US banks that stand to suffer the most if a wave of defaults his the shale patch:

Morgan Stanley was diplomatic enough to frame these banks only in the

context of their loan exposure, suggesting (strongly) they would have

to significantly boost their loan loss reserves, adversely impacting the

bottom line:

Crude Oil collapsed 25% to ~$30 per barrel from Friday’s close post

Friday’s OPEC+ meeting which ended without the anticipated production

cut. This puts oil prices at much closer if not below breakeven for many

US shale producers. Regions Financial, for example, underwrites to a stressed barrel of oil of $39.20. We assume that under the new accounting rule for CECL that banks will need to boost reserves for their oil and gas exposures during 1Q20 and 2Q20.

We assume that the banks will increase their loan loss reserves against

their energy portfolios to the levels reached in 1Q16 when oil prices

were running at about $30. This lowers EPS in 1Q and 2Q 20, shown in

Exhibit 19.

Assuming the shale situation is salvageable, Morgan Stanley then lays

out the large and mid-cap banks that have the most loan exposure and

will likely have to boost their reserves to the levels seen during the

Q1 2016 energy crisis:

We pulled energy exposures for the Large Cap and Midcap banks to assess how much the lower oil prices could drive up provisions.

We are using each bank's most recent energy loan disclosure listed

below. We assume that the banks today are holding a 1% reserve ratio

against these exposures. We then looked at how much loan loss reserves

banks held against energy loans in 1Q16,a time when oil prices were

around $30 per barrel. We assume that the banks will need to

increase their loan loss reserves against energy loans back to those

1Q16 levels in 1Q and 2Q this year,assuming oil holds at ~$30.

This increase in loan loss reserves is a bit quicker than prior cycles,

but since we are operating under the new Current Expected Credit Loss

accounting model (CECL), banks will need to reflect life time

losses for their oil exposures at an oil price today that is roughly

half of what it was on December 31,2019 when it ended the year at ~$66

For the largest banks this means billions in incremental energy reserves, subtracting directly from the bottom line....