Market Structure Matters: The Dislocation in the Treasury Markets

A quick hit from ZeroHedge:

....Yet, while the above charts clearly demonstrate the symptoms of the

collapse in fixed income liquidity, the question traders are grappling

with is what precipitated this historic dislocation, and why.

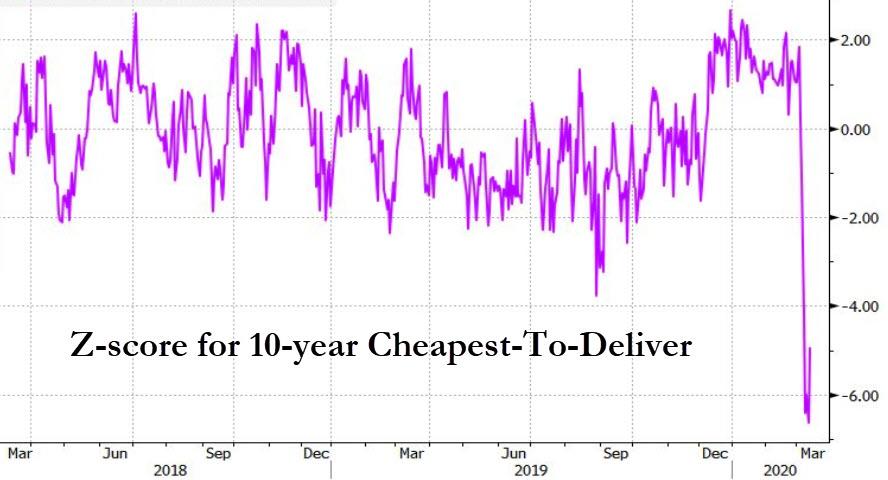

One answer comes this morning from Bloomberg's Stephen Spratt who

brings attention to "the cheapest-to-deliver bonds for Treasury futures

which mounted a blistering performance on Wednesday", noting - as we did

- that there was a huge position unwind in basis... "although the reason why is a mystery." Spratt shows the z-score for 10-year cheapest-to-deliver, a clear indication of how wild Wednesday’s move really was:

To all those who read the above as nothing more than gibberish, here is some background on how basis trades work.

As Spratt explains, "suppose 3-month general collateral is around

0.60%, you borrow the cash bonds and sell the futures at implied repo

0.70%. You roughly pocket 10bps. If you end up having to pay more to

fund the cash bond, this trade can quickly become uneconomical. When this happens, funds hit eject -- that appears to have happened on Wednesday."

Incidentally, the funds that put on these massively levered basis

trades are the same funds that found themselves locked out of the repo

market back in September, and prompted the Fed to launch repo

injections. Recall what the BIS' Claudio Borio said back then:

"High demand for secured (repo) funding from non-financial institutions, such as hedge funds heavily engaged in leveraging up relative value trades," was a key factor behind the chaos, said Claudio Borio, head of the monetary and economic department at the BIS.

Spratt confirmed as much, noting that that the thin margins and big

size in relative value trades makes them popular with leveraged hedge

funds (similar to the trades LTCM was putting on, and which resulted in

its eventual collapse). So when overnight repo general collateral on the

10-year was being quoted near -3%, according to sources, it starts to

make sense. It also makes some sense why the Fed announced pumped up

repo operations on Tuesday, a day early of its Wednesday announcement

when it again hiked the maximum size of the repo facilities and also

added the 1-month term repo.

As Spratt further explains, a part of the reason why repo has been

elevated in specific issues "is that recent volatility has seen

VaR/balance sheet limits being adjusted, which has resulted in a pull

back of the more balance-sheet intensive activities, including repo and basis trades."

Finally, this morning none other than JPMorgan chimed in on this

critical topic, with the following explainer why "we should care about

the Treasury futures basis"... and its historic dislocation:...