From Wolf Street:

Nightmare scenario for the markets? They just shrugged. But homebuyers haven’t done the math yet.

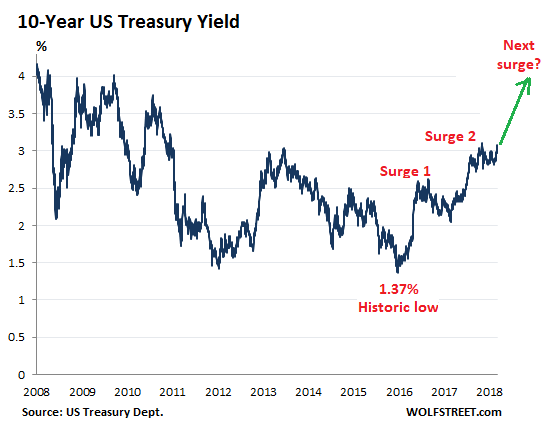

There’s an interesting thing that just happened, which shows that the US Treasury 10-year yield is ready for the next leg up, and that the yield curve might not invert just yet: the 10-year yield climbed over the 3% hurdle again, and there was none of the financial-media excitement about it as there was when that happened last time. It just dabbled with 3% on Monday, climbed over 3% yesterday, and closed at 3.08% today, and it was met with shrugs. In other words, this move is now accepted.

Note how the 10-year yield rose in two big surges since the historic low in June 2016, interspersed by some backtracking. This market might be setting up for the next surge:

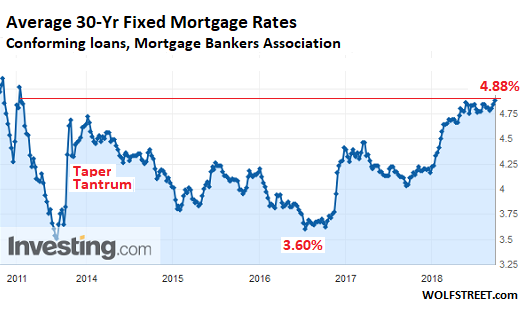

And it’s impacting mortgage rates – which move roughly in parallel with the 10-year Treasury yield. The Mortgage Bankers Association (MBA) reported this morning that the average interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) and a 20% down-payment rose to 4.88% for the week ending September 14, 2018, the highest since April 2011.

And this doesn’t even include the 9-basis-point uptick of the 10-year Treasury yield since the end of the reporting week on September 14, from 2.99% to 3.08% (chart via Investing.com; red marks added):

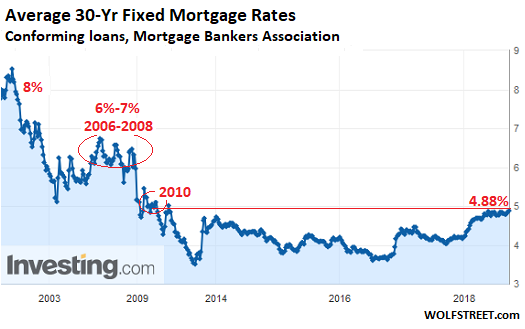

While 5% may sound high for the average 30-year fixed rate mortgage, given the inflated home prices that must be financed at this rate, and while 6% seems impossibly high under current home price conditions, these rates are low when looking back at rates during the Great Recession and before (chart via Investing.com):

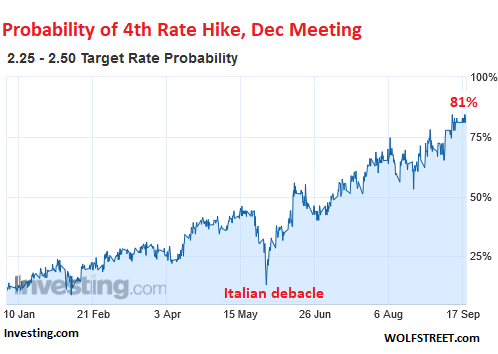

And more rate hikes will continue to drive short-term yields higher, even as long-term yields for now are having trouble keeping up. And these higher rates are getting baked in. Since the end of August, the market has been seeing a 100% chance that the Fed, at its September 25-26 meeting, will raise its target for the federal funds rate by a quarter point to a range between 2.0% and 2.25%, according to CME 30-day fed fund futures prices. It will be the 3rd rate hike in 2018.

And the market now sees an 81% chance that the Fed will announced a 4th rate hike for 2018 after the FOMC meeting in December (chart via Investing.com, red marks added):

...MORE

Our July post was "Signals From the Yield Curve: It's the Long End That Gets You" :

This forecast is so close to our thinking that I did a double-take when I first saw it.The combo of a rising long end combined with a slowdown due to tariff concerns has proven accurate only for the first half of the combo. We reiterated it in August's "10Y Treasury Yield Tops 3.00% After Surprise Supply Increase":

The only thing I can add is to point out that these are dynamic systems, that any changes to the trajectory have implications for where we end up so this scenario is not preordained.

But that's the way to bet. At the moment.

It's possible that the tariff-and-currency war of 2018 slows things down enough that the Fed pauses, stops bumping up the short end or that Treasury issuance is large enough to drive the long end higher but for right now, this is where we're at....

As foretold by the prophesy:If interested see also:

"..It's possible that the tariff-and-currency war of 2018 slows things down enough that the Fed pauses, stops bumping up the short end or that Treasury issuance is large enough to drive the long end higher but for right now, this is where we're at..."I know we've gotten a bit obsessive with the whole "the yield curve does not matter" but it is important. The recession chatter is early, if not flat wrong.

We'll have some ideas if and when the curve matters for equities and the economy but right now there are more pressing concerns.

June 29

"Who’s Afraid of a Flattening Yield Curve?"

March 11

San Francisco Fed: "Economic Forecasts with the Yield Curve"

And from last December:

Interpreting the Yield Curve: Counterintuitive Stimulative Effects of Rate Hikes

The writer, David Andolfatto is Vice President of the Federal Reserve Bank of St. Louis.

Views should in no way be attributed to the Federal Reserve Bank of St. Louis, or to the Federal Reserve System.

Neither should the blog be taken as an endorsement of the fashion sense of the Federal Reserve Economics Data clothing line:

The FRED Team

Posted in FRED Announcements