More on that after the OPEC production freeze meeting.

WTI $38.55 down $1.24; Brent $39.39 down $1.08.

From RBN Energy:

Are We There Yet? - What $40/Bbl Means To Crude Oil Markets

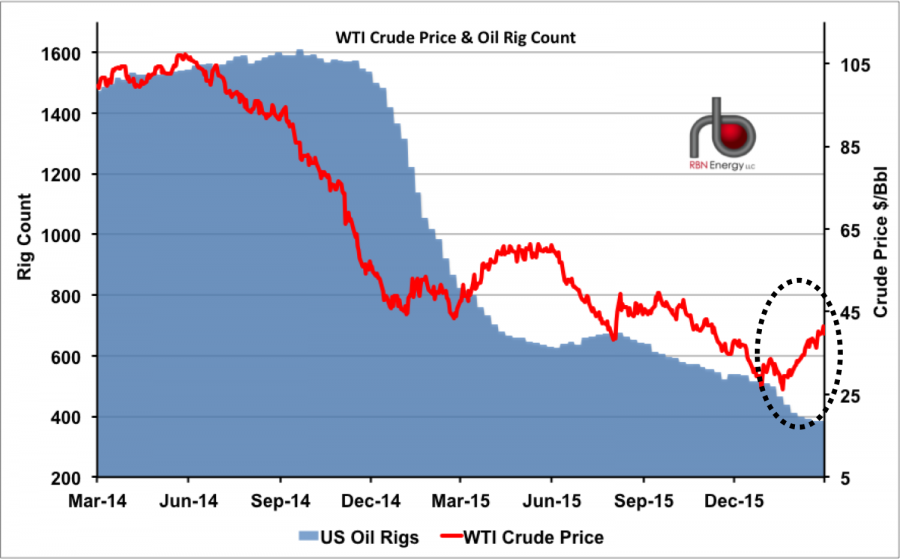

In the five weeks since February 11, the price of WTI crude oil on the CME/NYMEX spiked 50%, up from $26/bbl to $40/bbl (see black dashed circle in Figure #1). For hedge funds that took long positions in February, it was an awesome trade. And for beleaguered producers, it was certainly a bit of good news. But there are no celebrations in the streets of Houston and Oklahoma City. The fact that $40/bbl should be considered “good news” is sobering: Eighteen months ago, that price level would have been seen as a catastrophe for the producing community. In fact, it still is. In today’s blog we examine the factors that help push prices above $40/bbl and what it will take to really get US production growing again.

Yes, $40/bbl crude oil will help the balance sheets of most oil and gas producers. A handful of rigs might be put back to work. But let’s put things in perspective. Since October 2014, the price of crude is down 60%, over 1,200 rigs drilling for crude (75%) have been idled (see Figure #1), and thousands of oil industry workers are looking for jobs. Producer CAPEX budgets have been slashed, and the reality is that a price of $40/bbl will do little to change the meager investment plans that most producers laid out in their Q1 earnings calls. At $40/bbl, producer returns for drilling most shale wells are under water. Consequently, new drilling has slowed to a crawl. A few companies have declared bankruptcy, and more are on the way.

Figure #1; Source: Baker Hughes and CME Data from Morningstar, RBN Energy (Click to Enlarge)

In the midst of this carnage, the market has started – ever so slowly – to correct itself. Production volumes are declining. Even though the US Energy Information Administration reports that US crude oil production remains above 9 million barrels per day, it is down about 600 thousand barrels per day from its peak this time last year, and will likely drop at least another 750 thousand barrels per day by year end.

The big question, of course, is whether this decline in production, and all the other factors that impact global crude oil supply and demand, have already started to balance the market. Could that explain the 50% spike in crude oil prices over the past five weeks? Is the bottom of the crude oil price crash in the rearview mirror? And are we looking at a meaningful price recovery over the next few months?

Well, it is possible. But it depends on what we consider meaningful. And it also depends on what we deem to be a recovery.

First, let’s consider why prices have spiked up to $40/bbl. While it is possible that supply and demand have moved into balance, it is more likely that technical factors and market psychology have been responsible for much of the increase. There were few fundamental factors pushing the price of oil down to $26/bbl in the first place. Instead, it was the combination of a preponderance of bearish news (Iran production increases post-sanctions, lower demand from a weak Chinese economy, high U.S. oil inventories) accelerated by financial players piling on short trades, driving the market lower. When the news cycle shifted to a glimmer of hope (OPEC/Russia meetings on some kind of production freeze, the promise of higher demand as the U.S. shifts to driving season and summer gasoline blends), the shorts cashed out, and the crude oil price responded accordingly. Whether these factors have solely been responsible for the recent price increases, or whether real changes in the supply/demand balance have also been at work, won’t be known for weeks to come.

But if this is truly the start of an upward trend in crude oil prices, what should we consider meaningful? A price of $40/bbl is not it. At $40/bbl and with today’s drilling and completion costs, there are only a few spots in the major shale plays where it makes economic sense to drill and produce more oil. Those companies smart (or lucky) enough to have potential drilling locations in the sweet spots (locations where the most prolific wells can be drilled) can still drill and still make money. But across all the shale plays in the U.S., there are only about a dozen oil-dominant counties where those economics work. Everywhere else, producer returns for drilling and completing an oil well are in the red.

Thus to be meaningful, the price for crude oil must increase to a level where the economics for a larger number of potential wells are in the black. Furthermore, that price must be confirmed by the forward price of crude (the futures curve) and producers must believe that it will stay at that level for some time and, hopefully, continue to increase. If those conditions are met, it is likely we will see a meaningful response from many producers at a price above $55/bbl. Even though this is far below the $100/bbl price of the shale heydays, many producers can make this number work now because their service providers (drilling crews, frack crews, etc.) have reduced costs by 25-40%, the producers have become much more efficient in their operations, and many more drilling locations are economic at a price level of $55/bbl. Of course, for producers to jump back into the oil patch at that price requires bringing back a lot of workers no longer employed in the industry. And capital must be available to finance the drilling of wells. Determining how these two factors (hiring and finance) will impact the oil patch is a big question for the industry today. Particularly for the hiring issue, the longer prices stay down, the greater the problem becomes.

The other question we need to consider is – what do we deem to be a recovery? Certainly, the producing community would like prices to get back to the good ole days of eighteen months ago - $100/bbl, and then stay at that level for the next few decades. That is pretty unlikely. In fact, what is much more likely is that shale has fundamentally changed the oil market such that the word recovery is no longer relevant to the conversation. That is because oil prices are now range bound, locked into a bracket which is capped at the high end, and with a floor at the low end....MORE