Goodbye Stranger? – Brent and WTI Take Separate Paths Again

The Brent premium to West Texas Intermediate (WTI) on Friday (October 18, 2013) was $9.14/Bbl – indicating a new disconnect between US crude prices and international levels. Unlike last time a big Brent premium to WTI opened up in 2010 the price of Light Louisiana Sweet at the Gulf Coast is still tracking with WTI rather than following Brent. This suggests that the US Gulf Coats is long crude at the moment and that imports of Brent priced crude are not required. Today we discuss the current Gulf Coast crude market....

... New Brent Disconnect?

This month’s big spread theme is that Brent prices have taken off on their own track since the end of September even as WTI prices retreated. That has caused the Brent premium to WTI to widen to more than $9/Bbl. Our story today is concentrated on the Gulf Coast so we introduce LLS to the picture as well.

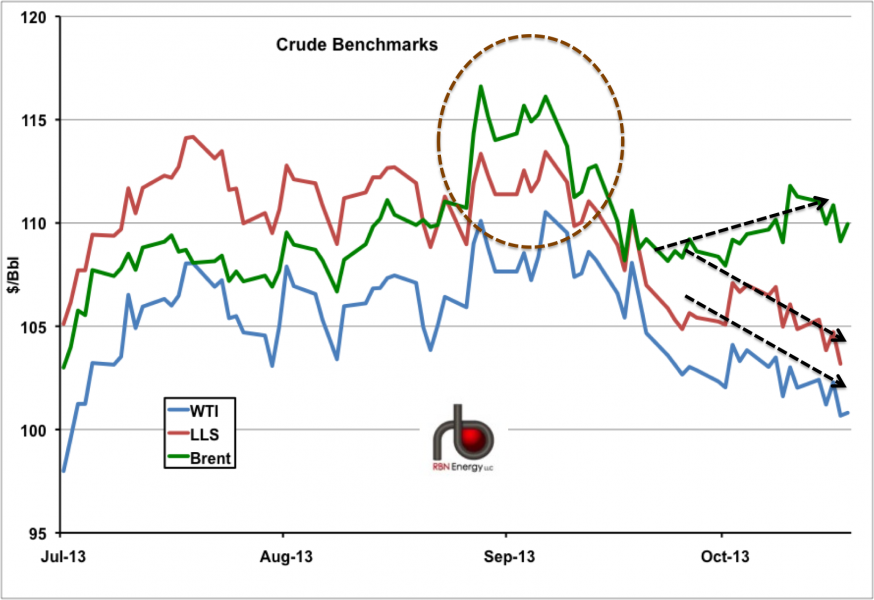

During the three-year long Brent/WTI disconnect, LLS pretty much tracked Brent prices because, as a coastal crude its price was set by the international market. Since the WTI/Brent spread narrowed this year LLS has tracked closer to WTI. The chart below shows prices for the three crudes in this equation since July 2013 - Brent (green line), WTI (blue line) and LLS (red line). Up until the 20th of August, all three crudes traded together in a narrow range with Brent in the middle at a discount to LLS and a premium to WTI.

Then Brent prices took off higher on their own – rising past LLS. This initial strength in Brent prices was primarily due to the Syria crisis and supply problems in West Africa that supported higher Brent prices for a few weeks until they fell back towards LLS during the second week in September (brown dashed circle on the chart). However a couple of weeks later Brent was back on its own track again – this time moving higher as both LLS and WTI fell (black dotted arrows on the chart).

Source: CME data from Morningstar (Click to Enlarge)This sudden divergence in the Brent price runs counter to the thinking of many analysts. That is because it signals that US Gulf refineries currently have adequate crude supplies and do not need imported barrels – certainly of light crude but also of medium grades as well - i.e. any crudes with prices linked to Brent. If there were demand for these imported barrels then theoretically the price of LLS would be tracking closer to Brent because those imports would compete with LLS for the attention of Gulf Coast refiners. With LLS at a near $6/Bbl discount to Brent the Gulf Coast is not attracting imports.Why is that such a shock? After all, US production has been increasing in leaps and bounds and we know that a lot of shale crude has been arriving at Gulf Coast refineries from North Dakota, the Permian Basin and the Eagle Ford. The reason for the surprise is that Gulf Coast refineries were (up until early October) running at over 90 percent of capacity and although more domestic crude is making its way to the region, most believed that refiners still need plenty of imported supplies to make up their feedstock requirements.

But this week, prices seem to be telling us that the Gulf Coast is awash with crude supplies. LLS crude is trading at a $3/Bbl premium to WTI – less than the cost of transport from Cushing to the Louisiana Gulf Coast (where LLS is delivered at St. James). The Houston price for WTI (the Platts Light Houston Sweet assessment see Houston We Have An Assessment) is tracking neck and neck with LLS. So Louisiana refiners are getting adequate supplies from local offshore production, barges from Corpus Christi or rail from North Dakota and have no need for Cushing barrels. In any case the current work to reverse the Ho-Ho pipeline means there is no pipeline link from Houston to St James. Even heavy crudes look to be over supplied at the Gulf Coast at the moment. The price of two heavy sour grades – West Texas Sour and Southern Green Canyon - were discounted last week by more than $7/Bbl to WTI due to low demand for these crudes by Houston refineries. In short – Houston and Louisiana Gulf Coast refineries appear to have plenty of crude....MUCH MORE