Release date: 05/04/2018

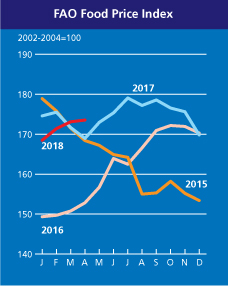

...MUCH MORE» The FAO Food Price Index* (FFPI) averaged 172.8 points in March 2018, up 1.1 percent (1.8 points) from February, marking the second month of consecutive increase. At this level, the FFPI stood at 0.7 percent above its value of the corresponding month last year. As in February, the month-on-month increase in March was driven primarily by stronger international prices of cereals and dairy; whereas the prices of sugar and vegetable oils fell further and those of meat rose slightly.» The FAO Cereal Price Index averaged 165.6 points in March, 2.7 percent (4.3 points) higher than in February and as much as 12.1 percent above its value in March 2017. The Index has been climbing continuously in recent months, reflecting firmer international prices of nearly all major cereals. In recent weeks, weather concerns, in particular prolonged dryness in the United States and cold wet conditions in parts of Europe, lifted wheat price quotations. However, the increase in maize prices proved even more pronounced, supported by deteriorating crop prospects, especially in Argentina, as well as continued robust world demand. Asian purchases kept international rice prices also generally firm.

******» The FAO Dairy Price Index averaged 197.4 points in March, up 6.2 points (3.3 percent) from February and slightly above its level in the corresponding period last year. During the month, international price quotations for butter, Whole Milk Powder (WMP) and cheese rose, while those of SMP declined, reversing the gains recorded in the two preceding months. Lower than anticipated milk production in New Zealand and continued strong global import demand led to higher butter, cheese and WMP prices, while continued pressure from global stocks and higher production pushed down SMP prices.

» The FAO Meat Price Index averaged 169.8 points in March, almost unchanged from February. At this level, the index is 3 percent above the corresponding month last year but still almost 20 percent below the peak reached in August 2014. Across the various meat categories that constitute the index, price quotations for ovine meat increased, pig meat gained slightly, poultry meat remained stable, while those for bovine meat eased. Strong import demand, especially by China, strengthened ovine meat prices. Somewhat tight supplies in Europe underpinned a small increase in pigmeat prices, while subdued demand and expectations for supplies from New Zealand to increase in the coming months weighed on bovine meat values....

As can be seen on the accompanying graphic the index could be headline-making in a couple months (over on the left, in red):