Today however I'm on board with Bill and am of the opinion that going forward we'll have to take Dante as our guide through investment Hades:

Abandon All Hope Ye Who Enter HereHere's the Janus Monthly Investment Outlook from Bill Gross:

June 2, 2016

Bon Appetit!

The economist Joseph Schumpeter once remarked that the “top-dollar rooms in capitalism’s grand hotel are always occupied, but not by the same occupants”. There are no franchises, he intoned — you are king for a figurative day, and then — well — you move to another room in the castle; hopefully not the dungeon, which is often the case. While Schumpeter’s observation has obvious implications for one and all, including yours truly, I think it also applies to markets, various asset classes, and what investors recognize as “carry”. That shall be my topic of the day, as I observe the Pacific Ocean from Janus’ fourteenth floor — not exactly the penthouse but there is space available on the higher floors, and I have always loved a good view.Anyway, my basic thrust in this Outlook will be to observe that all forms of “carry” in financial markets are compressed, resulting in artificially high asset prices and a distortion of future risk relative to potential return that an investor must confront.

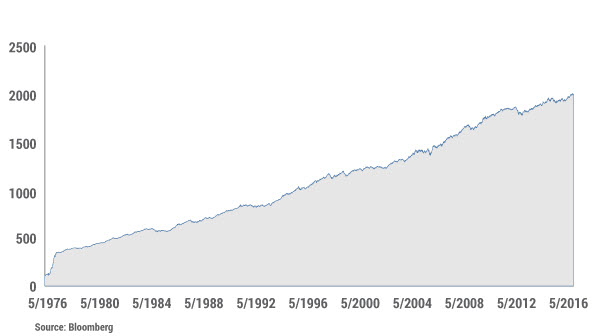

Experienced managers that have treaded markets for several decades or more recognize that their “era” has been a magnificent one despite many “close calls” characterized by Lehman, the collapse of NASDAQ 5000, the Savings + Loan crisis in the early 90’s, and so on. Chart 1 proves the point for bonds. Since the inception of the Barclays Capital U.S. Aggregate or Lehman Bond index in 1976, investment grade bond markets have provided conservative investors with a 7.47% compound return with remarkably little volatility. An observer of the graph would be amazed, as was I, at the steady climb of wealth, even during significant bear markets when 30-year Treasury yields reached 15% in the early 80’s and were tagged with the designation of “certificates of confiscation”. The graph proves otherwise, because as bond prices were going down, the higher and higher annual yields smoothed the damage and even led to positive returns during “headline” bear market periods such as 1979-84, or more recently the “taper tantrum” of 2013. Quite remarkable, isn’t it? A Sherlock Holmes sleuth interested in disproving this thesis would find few 12-month periods of time where the investment grade bond market produced negative returns.

Chart I: Barclays Capital U.S. Agg Total Return Value Unhedged

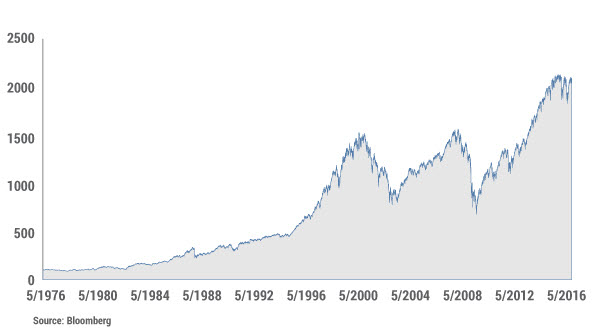

The path of stocks has not been so smooth but the annual returns (with dividends) have been over 3% higher than investment grade bonds as Chart 2 shows. That is how it should be: stocks displaying higher historical volatility but more return.

But my take from these observations is that this

40-year period of time has been quite remarkable – a grey if not black swan event that cannot be repeated.

But my take from these observations is that this 40-year period of time has been quite remarkable – a grey if not black swan event that cannot be repeated. With interest rates near zero and now negative in many developed economies, near double digit annual returns for stocks and 7%+ for bonds approach a 5 or 6 Sigma event, as nerdish market technocrats might describe it. You have a better chance of observing another era like the previous 40-year one on the planet Mars than you do here on good old Earth. The “top dollar rooms in the financial market’s grand hotel” may still be occupied by attractive relative asset classes, but the room rate is extremely high and the view from the penthouse is shrouded in fog, which is my meteorological metaphor for high risk.

Let me borrow some excellent work from another investment firm that has occupied the upper floors of the market’s grand hotel for many years now. GMO’s Ben Inker in his first quarter 2016 client letter makes the point that while it is obvious that a 10-year Treasury at 1.85% held for 10 years will return pretty close to 1.85%, it is not widely observed that the

Chart 2: S&P 500 Index - Dividend Adjusted Value

rate of return of a dynamic “constant maturity strategy” maintaining a fixed duration on a Barclays Capital U.S. Aggregate portfolio now yielding 2.17%, will almost assuredly return between 1.5% and 2.9% over the next 10 years, even if yields double or drop to 0% at period’s end. The bond market’s 7.5% 40-year historical return is just that – history. In order to duplicate that number, yields would have to drop to -17%! Tickets to Mars, anyone?

The case for stocks is more complicated of course with different possibilities for growth, P/E ratios and potential government support in the form of “Hail Mary” QE’s now employed in Japan, China, and elsewhere. Equities though, reside on the same planet Earth and are correlated significantly to the return on bonds. Add a historical 3% “equity premium” to GMO’s hypothesis on bonds if you dare, and you get to a range of 4.5% to 5.9% over the next 10 years, and believe me, those forecasts require a foghorn warning given current market and economic distortions. Capitalism has entered a new era in this post-Lehman period due to unimaginable monetary policies and negative structural transitions that pose risk to growth forecasts and the historical linear upward slope of productivity.

For over 40 years, asset returns and alpha generation from penthouse investment managers have been materially added by declines in interest rates, trade globalization, and an enormous expansion of credit – that is debt.

Here’s my thesis in more compact form: For over 40 years, asset returns and alpha generation from penthouse investment managers have been materially aided by declines in interest rates, trade globalization, and an enormous expansion of credit – that is debt. Those trends are coming to an end if only because in some cases they can go no further. Those historic returns have been a function of leverage and the capture of “carry”, producing attractive income and capital gains. A repeat performance is not only unlikely, it is impossible unless you are a friend of Elon Musk and you’ve got the gumption to blast off for Mars. Planet Earth does not offer such opportunities.

“Carry” in almost all forms is compressed and offers more risk than potential return. I will be specific:...MORE

*See for example ""The Time PIMCO's Bill Gross Acted Like A Cheap Prick To A Waitress""