In the U.S. we have devolved to perma-stimulus, every dollar of deficit spending being stimulus, and have no plans to ever stop. Anyone who argues that stimulus isn't stimulus unless it is labeled stimulus is being sillier than I felt when I typed this sentence.

Deficit spending is stimulus whether you call it ARRA,

From RealCleaMarkets:

The Marginal Economics of the Welfare State

The recent news that Fed Chairman Ben Bernanke is launching a second Operation Twist, yet another round of monetary stimulus, raises two related questions: Why do they keep trying this even though it doesn't work, and why doesn't it work?

I am not the first to note that we are living in an era of "permanent stimulus," and it's not just monetary. In fact, you can look at the whole welfare state as a permanent, standing "stimulus" program, since it borrows trillions of dollars that are continually pumped into the economy by increasing the consumption spending of those who otherwise could not afford it. The Supreme Court just removed a major obstacle to a new expansion of that permanent stimulus state-which makes the question of why stimulus fails all the more urgent.

A big clue to the answer is that stimulus fails because it always becomes permanent. The original Keynesian theory of stimulus was that the government would borrow and spend during an economic downturn in order to stimulate economic growth, and then once that growth took off, government would stop stimulating, cut its expenses, and pay down its loans. At least, that is how the idea is generally sold. The stimulators tell us that a recession is the wrong time to cut back spending, as if they ever thought that there might be a good time.

But they never do, and there is an inexorable logic to this. If economic growth is based on government stimulus, if that is what gets the economy going, then we would never dare to remove the stimulus, for fear of stopping the government's engine of growth. Keynes himself agonized that cutting back on the World War II defense buildup, which supposedly ended the Great Depression, would plunge the economy back into a decline. It did the opposite, of course, but our great economists never learned the lesson. And so we see the pattern of the current Stimulus Depression. Every time one round of stimulus begins to wear off, as is happening now, the Fed injects another.A couple days ago OfTwoMinds had a piece on how little bang for the buck we get for each dollar of debt versus the impact in prior decades, another point we've harped on:

It reminds me of an interview I saw once with a former methamphetamines addict who described how, as always happens, his body became accustomed to the drug. It became the "new normal," and he needed larger doses to have the same effect. By the end, the drug he once took to experience a high of superabundant energy he now took just to be able to get out of bed in the morning. That pretty much describes the function of Operation Twist, Part Two. The economy is hooked on stimulus, and it keeps needing just one more fix, not to thrive, but to keep from crashing.

Addicts are known for having their "lost decades," years that they spend searching for short-term highs instead of dealing with their deeper problems. So it should be no surprise that our addicted economy is halfway through a lost decade of its own.

And it's not just that stimulus is permanent. It also becomes all-encompassing. Consider the pattern of the growth of the welfare state-again, this is a permanent, standing form of stimulus spending-to encompass every economic need experience by everyone. James DeLong has a good summary of this process.

"[T]he concept of 'welfare' has become an open, bottomless vessel into which every desire can be poured: Government takeover of the entire health and retirement systems; detailed regulation of employment; manipulation of money; subsidies for housing, education, energy, food; or anything else that strikes the fancy of some segment of the public."The 'some segment' part is crucial, because today's welfare has ceased to be limited to that of the public generally, or to the welfare of any group that has a serious claim to special deserts. Instead, it is the welfare of some special interest that is able to capture the policy process."Hence the political resistance of public employees' unions against any attempt to make their own portion of the modern welfare state a little less comfortable....MORE

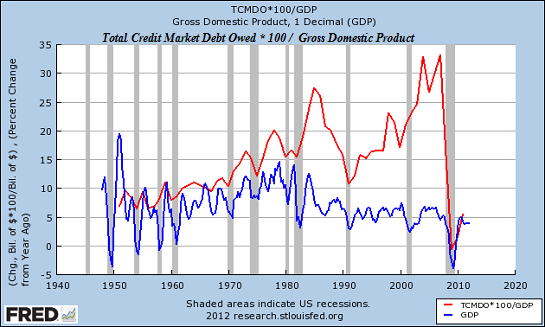

Why The Debt-Dependent Status Quo Is Doomed in One Chart

The global economy is now addicted to debt. Once debt stops expanding, the economy shrivels. But expanding debt forever is unsustainable. Welcome to the endgame. Regardless of whether you call it debt saturation or diminishing return on new debt, the notion that taking on more debt will magically enable us to "grow our way out of debt" is not supported by data. Correspondent David P. recently shared this chart of Total Credit Market Debt Owed and GDP and this explanation:

The purpose of this chart is to examine the relationship of total debt to GDP. Since Debt is not factored into GDP, just exactly how much debt is being used to create growth, and over what time periods. But absolute numbers don't work so well, since they don't let you examine particular years, seeing what the 1950s look like vs the 2000s, for example. Red Line: Annual Change in TCMDO (Total Credit Market Debt Owed) * 100/ That year's total GDP, showing that year's % increase in TCMDO/GDP.

Blue line: % change in GDP over last year.

Any gap between the red line and the blue line is what I would call the creation of debt in excess of income. And that gap is the ANNUAL gap, not a cumulative gap. As an example, in 2008 TCMDO grew by an average of 30% of that year's GDP, while GDP itself grew by around 5%. Ouch.

So projecting forward, how much debt growth do you think we'd need to get back to business as usual? 50s was 8%, 60s about 12%, 70s 15%, 80s maybe 20%, 90s back down to 15%, and 00s probably 25-30% per year. We'd probably need a surge of 35% or more, per year, to bring back those exciting bubble years. But who could possibly have the income to support that? To quote the parable of the Little Red Hen: "Not I", said the goose.Thank you, David. Note what happened to GDP the moment debt ceased expanding in 2008: it tanked. This is the chart of debt addiction: the moment the expansion of debt is withdrawn, the economy implodes....MORE