From Phenomenal World, May 30:

Perceptions are shifting regarding the US fixed-income market. In September 2019, interest rates on overnight repos unexpectedly spiked, leading the Federal Reserve Bank of New York to inject $75 billion in liquidity. In March 2020, the Covid-19 pandemic triggered a wave of securities selling, prompting the Fed to purchase over $1 trillion in securities. These events have raised concerns about market stability.

In response, regulators have mandated that Treasury and repo transactions be cleared through clearinghouses. However, many participants, such as hedge funds, lack direct access to central counterparties (CCPs) and rely on dealing banks to connect them. Dealers, citing potential costs, have begun to ditch such clients. An intentional yet indirect consequence of these regulatory policies is the reduced participation of hedge funds in this market.

The issue, however, stems from a misdiagnosis of the underlying problem. The prevailing understanding attributes this instability to the behavior of alternative investment funds like hedge funds engaging in “basis trades,” framing liquidity as the key issue in the Treasury market. However, drawing on insights from my interview with seasoned fixed-income portfolio manager Mohsen Fahmi, this piece argues that the market suffers from a different problem altogether: specifically, a chronic inefficiency in the hedging market that could potentially lead to a systemic failure of fixed-income risk management strategies.

Locating risks hidden in plain sight within pragmatic risk management practices involves broadening our perspective. We need to view investment funds’ business models, including traditional ones like bond funds and alternative ones like hedge funds, as responses to changes in market structures rather than in isolation. This perspective allows us to see these business models as vehicles that transfer inefficiencies and opportunities from one market, such as the derivatives market, to other markets, such as the Treasuries cash market.

Bond mutual funds are major players in the US Treasury market. The primary risk they encounter is the interest rate risk. Fund managers often use derivatives like options and interest rate swaps to hedge against this risk. These hedging tools have proven effective as their duration matches that of the underlying assets. For fixed-income fund managers with long-term investments, the Treasury options and interest rate swap markets used to offer contracts with durations matching their portfolios. However, the market for Treasury options is disappearing, affecting fixed-income fund managers with long-term investments. Additionally, as an earlier interview with Ralph Axel (the rate strategist at BofA, one of the largest swap dealers) demonstrated, the swap market is also shifting toward catering to different types of clients, particularly those with shorter-term investments.

The inability of options and interest rate swaps markets to offer the exact duration leaves an important gap in fixed-income risk management—“duration drift”—the unhedged portion of the portfolio due to the mismatch between the durations of the derivatives and the assets. Moreover, these risks are usually hidden through hedge accounting conventions that enable inefficient hedges to remain unreported.

To tackle inefficiencies in the options and swaps markets, there has been a shift in hedging demands towards the futures market. Shorter contracts in interest rate swaps and the disappearance of options force fixed-income asset managers to construct their hedging strategies based on futures. This shift generates extra demand for such contracts and increases basis points that hedge funds exploit. However, this behavior of hedge fund managers is just the tip of the iceberg. The larger hazard is shaped by the distortions in the fixed-income derivatives market. Consequently, the solution to stabilize the market lies not in the US Treasury cash market but in its hedging markets.

Instead of focusing on restricting the actions of hedge funds, regulators should learn from risk managers of mutual funds to develop a tool that measures the extent of hedging inefficiencies system-wide. Such a tool can become a new indicator of systemic risks in the fixed-income market. By developing and implementing tools to measure hidden hedging inefficiencies, regulators can gain better insights into creating a more stable and resilient financial system.

How regulators see hedge funds in the Treasury market

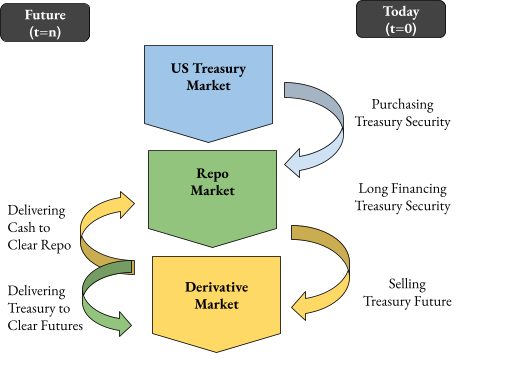

The shift in fixed-income fund managers’ portfolios toward US Treasury futures has caused prices to diverge from the related underlying asset, a Treasury security, leading to what is known as “basis.” Normally, policymakers and academics treat such deviations as short-lived phenomena, or sunspots, rather than structural issues. These deviations are expected to be resolved through arbitrage activities, which help the market correct itself, and the prices revert to their baseline and fundamental levels.However, regulators’ problem with hedge fund arbitrage strategies is that they are orchestrated in a way that siphons liquidity from the market. The key to understanding this hostility towards hedge funds compared to a theoretical arbitrager is “leverage.” Regulators’ adverse view of hedge funds as arbitrageurs stems from their reliance on leveraged funding. Alternative investment funds conduct the arbitrage through “basis trades”—borrowing from the repo market to buy US Treasury securities at a lower price and simultaneously selling US Treasury futures at a higher price....

....MUCH MORE

Also at Phenomenal World, May 30:The Structure of the US Treasury Market