This is positively chipper compared to some of Albert's year-end missives.

Last year it was: "Société Générale's Albert Edwards' 2022 Outlook: Four Big Surprises... And Lots Of Pain" and nine years prior:

"Season's Greetings From Société Générale's Albert Edwards (Nov. 14, 2012)

Expect the New Year to bring nothing but disappointment...."

So lets us see why Albert is off suicide watch, shall we?

Via MacroBusiness, Australia, December 21:

By Albert Edwards at Societe Generale:

And the big surprise in 2023 will be…

… a return to deflation fears as headline CPI inflation drops close to, or likely below zero. Investors are already anticipating recession and have an unusually strong preference for bonds. But how low will yields fall in 2023 as headline inflation evaporates? Any decline will be purely a cyclical phenomenon rather than a full-blown return to the Ice Age theme. Investors have not yet discounted a second secular wave of inflation as we eventually exit this unfolding recession – ie the Great Melt.

Last week saw investors briefly indulge in a frenzy of excitement in the wake of lower-than expected US CPI data. After months of data releases consistently exceeding expectations, the hope that inflation might actually be retreating at a brisker rate sent almost all financial assets into Christmas party mode.

Unfortunately, resident Fed Grinch Jay Powell was at hand to dampen the euphoria of a market hoping for an early rate pivot. But in any case, as Gerard Minack has pointed out, equity investors eagerly anticipating the precise timing of a peak in the interest rate cycle (pivot) is akin to passengers on the Titanic eagerly anticipating what tune the band is about to play. The peak of a rate cycle is more often than not associated with the Fed having overdone the tightening cycle and the economy sliding into recession, resulting in pitiful equity returns. On the rare occasions when a Fed pivot does precede a soft landing, equity investors do indeed have something to celebrate. “You pays your money and takes your choice”. But history shows that equity investors cheering on a Fed pivot is akin to turkeys voting for Christmas.

There was one key piece of ‘good’ news for equity investors in Powell’s post-FOMC comments. The most important exchange was when someone asked him if the Fed’s 2% inflation target would be raised. Powell could have quickly quashed mounting speculation, but as ZeroHedge notes, “instead he hemmed and hewed, and did say that we are not going to consider that under any circumstances now… but then quietly added that ‘it may be a longer-run project at some point.’”

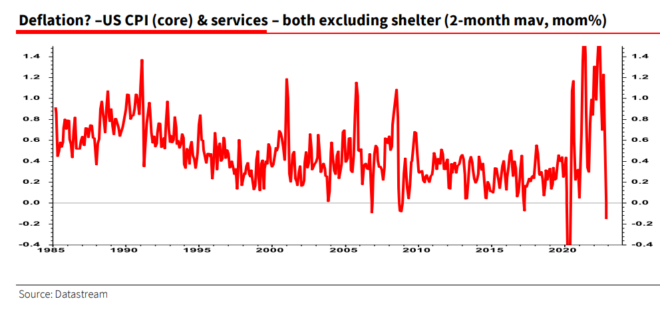

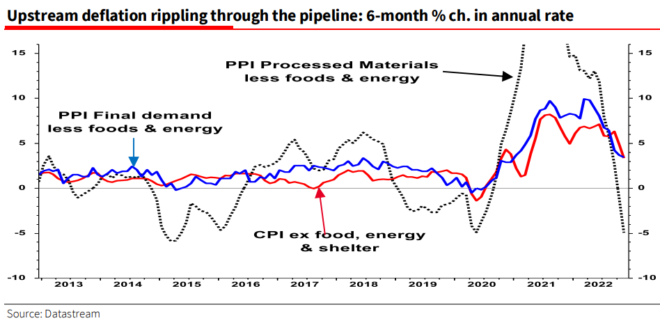

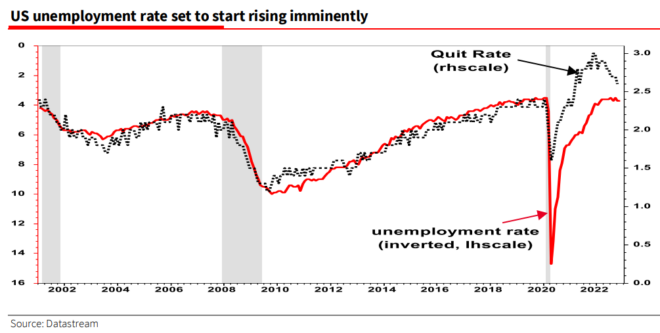

I’ve been doing this job long enough to know that a “a longer-run project” can quickly become a “must do project” if circumstances change. Hence, while nobody would expect Powell to signal that an increase in the Fed’s inflation target is imminent when inflation is at 7% and unemployment is near record lows, let’s see what happens when the unemployment rate starts to surge and headline inflation falls below zero (as the chart below indicates is in the pipeline).

The chart below also signals that the 2021 pipeline cost pressures are now in full reverse. The last two times that upstream PPI cost pressures saw this much deflation, core PPI and CPI inflation fell to zero on both occasions. Wage inflation may be higher now, but a rapid decline is still likely.

And momentum also appears to be reversing fast in the labour market; the fall in the Quit Rate indicates that the unemployment rate will likely soon start rising (red line = inverted scale).

As headline inflation falls below zero (and core inflation also abates), we expect investors to go ‘deflation doolally’....

....MUCH MORE

Hmmm...he must have new meds or electroshock or something because just reading this far I'm borderline despondent.