From American Affairs Journal, Winter 2022 edition, Volume VI, Number 4:

In the mid-1860s, things were looking up for Karl Marx. After years laboring in poverty and obscurity in a small apartment in London, his fortunes seemed to be turning around. In 1864, his friend and benefactor Friedrich Engels became a partner in his father’s factory, gaining a generous income for himself and offering Marx a path out of poverty. That same year, Marx’s political isolation—which had been acute since his expulsion from Germany in 1849—came to an end with the founding of the International Workingmen’s Association. In 1867, the first volume of his masterpiece, Das Kapital, was published.

In developing the critique of political economy laid out in Das Kapital, Marx believed that he had discovered a fundamental problem in the nature of capitalism. What he called “the tendency of the rate of profit to fall” not only allowed him to make predictions about the economic system’s future but also guaranteed that communism was the inevitable outcome of capitalist development. In the end, Marx maintained, capitalism would eat itself.

The Tendency of the Rate of Profit to FallMarx’s insight about the tendency of the rate of profit to fall was an outgrowth of his theory of surplus value, which in turn grew out of the labor theory of value characteristic of the classical economics of the eighteenth and nineteenth centuries. The labor theory of value stated that the value of goods produced ultimately came from labor; human labor is the beginning of all economic activity and therefore the source of value. Surplus value, for Marx, is the profit that capitalists skim off the top of productive labor. Marx observed that as technological development progressed, the labor share of production fell and the capital share rose. This led him to the conclusion that, since labor was the ultimate source of value and thus also of surplus value or profit, the rate of profit in a capitalist economy would fall as the labor share of production fell.

In a letter to Engels in 1868, Marx wrote that what capitalism was “striving for is capitalist communism,” and that the tendency of the rate of profit to fall was “one of the greatest triumphs over the pons asini of all previous political economy.”1 Marx believed that he had come up with a logical proof that capitalism would self-destruct; that the forces of capitalist production would eventually drive profits to zero and necessitate the victory of the working classes, who would seize the means of production.

Yet history has proven Marx wrong. The rate of profit has not fallen inexorably toward zero, as any stock analyst could attest. Investors do not typically deploy Marxian language, but they discuss the return on invested capital (ROIC) and the weighted-average cost of capital (WACC). If the ROIC for a given company is higher than the WACC, that company is creating value for the investor—that is, the company is turning a profit for the investor. Outside of severe recessions, the ROIC of the stock market as a whole remains consistently higher than the WACC, which is why investors in the market make money.2

Marx’s logical error was simple enough: he confused what might be called an ontological question with an economic question. Ultimately—ontologically—it is true that all economic value emerges from human labor. But it does not therefore follow that you can infer economic truths from ontological ones. Economic value is not really a “thing” or a “substance.” Rather, it is a subjective assessment placed on a product by an end consumer. This consumer does not typically care how much labor went into the product, only that the product satisfies a particular need. One pair of shoes may be made entirely by robots, another may be made entirely by men, but an end consumer could still assess both as having the same value.

Still, there is something haunting about Marx’s vision. The machinery of the capitalist economy is enormously impressive, but it often seems to drive ahead blindly. And the capitalist system also seems to contain internal contradictions that destabilize it. I shall argue here that a clear-eyed assessment of empirical data suggests that Marx’s vision may not have been entirely mistaken, and that capitalism, if left unchecked, could destroy itself. Indeed, I believe that we now find ourselves feeling the early effects of such contradictions.The Tendency of the Rate of People to FallMarx was no doubt correct that a capitalist economy requires a positive rate of profit in order to continue functioning in the long term. If profits were forever zero, there would be no incentive for investment and the economic engine would sputter and break down. Since Marx’s time, however, it has become clear to economists that capitalism needs more than just profits to survive.

Today, we think of prosperity in terms of economic growth, typically measured in terms of inflation-adjusted or “real” gross domestic product (GDP). The idea behind this metric is straightforward: measure how many transactions are made in the economy, adjust for inflation—that is, for the effects of price increases—and thus gain a sense of the total value of goods and services exchanged. An increase in the rate of real GDP growth thus reflects an increase in total economic output and gives us a sense of how much overall material wealth has increased.

In the short term, this rate of growth is most directly dependent on immediate economic conditions, including the rate of employment, the balance of trade, and the stage of the business cycle. But when we abstract away from these short-term effects, the rate of growth in real GDP in the long run is driven mostly by two factors: the pace of technological change (which includes efficiency gains from better resource management) and the rate of growth in the labor force....

....MUCH MORE

That's it, productivity and population.

And I haven't heard anyone come up with a way to increase productivity fast enough to overcome the GDP-lowering effect of population decline.

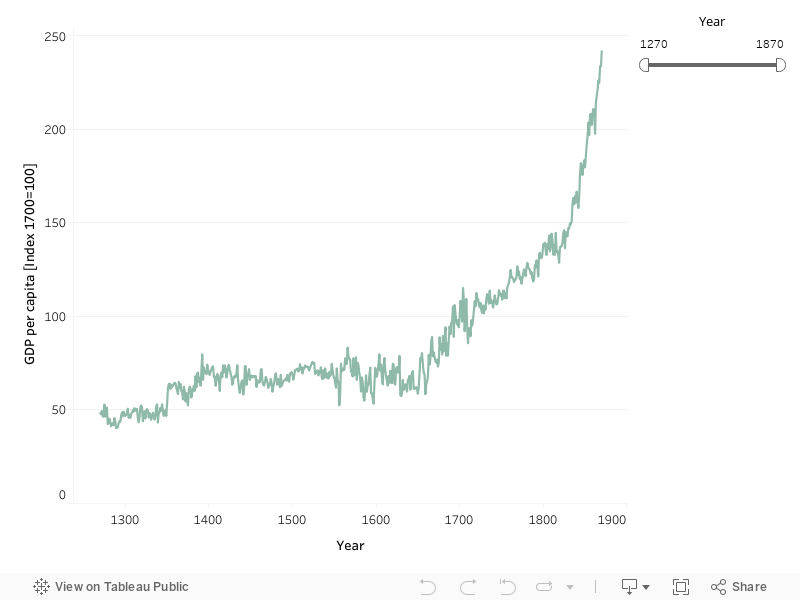

It actually appears that the world is headed for a version of the long stagnation. Here's GDP per capita in England, 1270 to 1700 and Great Britain, 1700-1870: