Back in the dimly remembered past (1973 - 1986) the rule of thumb was that a 10% move in oil resulted in a 1% move in inflation i.e. if price doubles you get 10% 'flation before anything else kicks in.

Although the economy has changed dramatically, with GDP not being nearly as dependent on oil & gas inputs, and is much more efficient for those sectors that still have energy as a primary/secondary/tertiary input, joules and watts and BTUs still matter a lot, regardless of the unit you use to express it.

Additionally, although the current round of price increases were at-first related to bottlenecks and supply disruptions in non-energy tradables the next go-round will be fueled by the shelter price increases we've already seen and will be sustained by the effects of energy costs diffusing throughout the economy.

And as a final note for this overly long introduction, it is good to keep top-of-mind the mantra that inflation may be transitory but the price increases for the consumer tend to be permanent: shrinkflation doesn't get reversed in the grocery aisle if wheat futures decline.

From ZeroHedge:

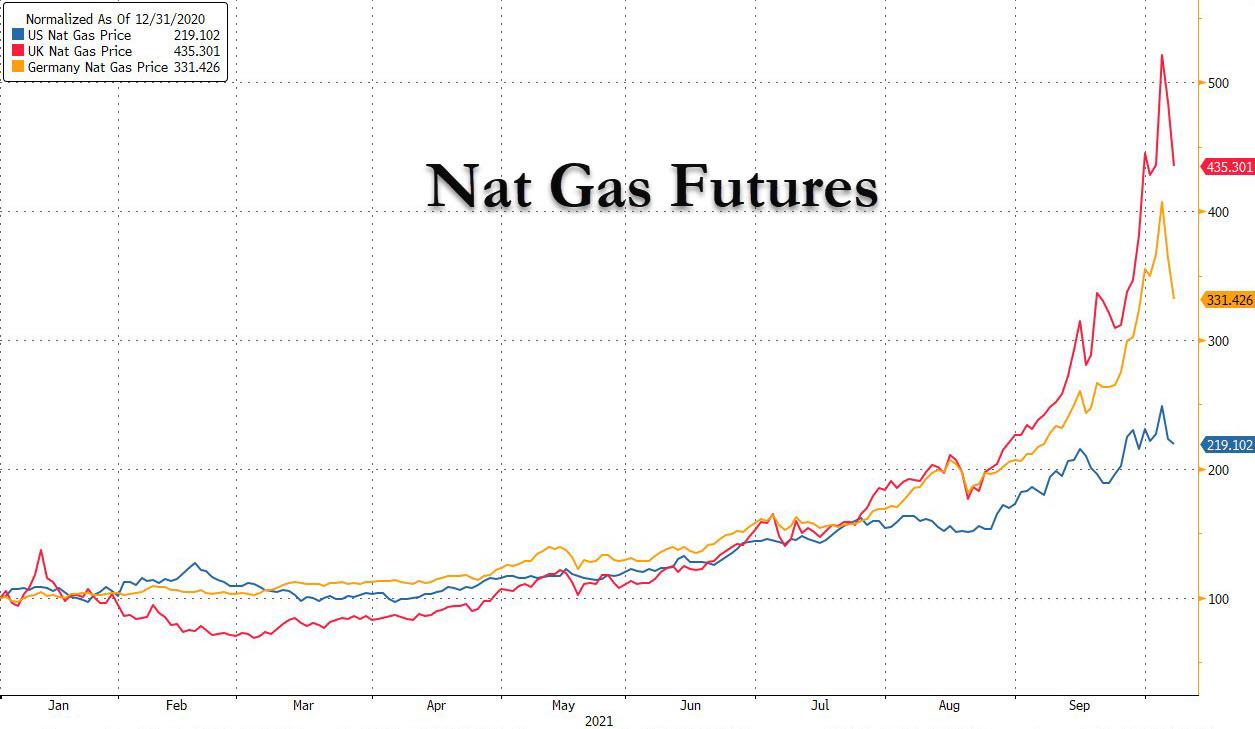

The surge in natural gas prices in 2021 has put even crytpocurrencies to shame: US Henry Hub spot prices have been averaging around $6/mmbtu, up about 40% from early in August and a surge of around 200% relative to prices at the start of the year; prices in German and the UK are orders of magnitude higher.

The dramatic price increase has prompted questions how it will impact inflation prints in the near-term, both headline and core, and indeed as JPM economist Daniel Silver writes today, "this recent jump is notable and should boost consumer prices."

As Silver explaions, while consumer prices for related services don’t fluctuate by nearly as much as spot prices and related products only account for a small share of the goods and services included in the main consumer price aggregates, even keeping all of that in mind, the massive surge in natural gas prices over the past year probably will add about a half of a percentage point to the change in the headline CPI over the same period.

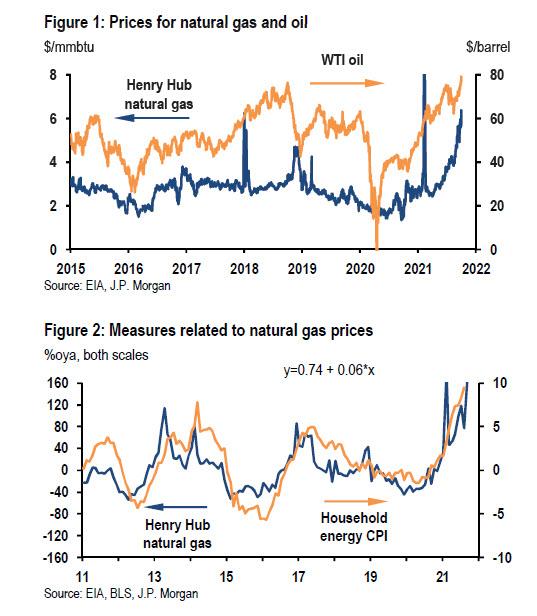

Meanwhile, oil prices have also spiked - in the case of WTI to the highest since 2014 - and while the percentage increase has not been nearly as large as the increase in nattie, the impact of the oil price increase on the CPI could be about four times as large as the effect of the surge in natural gas prices

Naturally, changes in nat gas prices impact the prices that consumers pay for household energy, which includes gas services, electricity, and various fuels, but there are also fixed costs and other factors that influence these consumer prices. According to JPM, over the past decade or so, the changes in consumer prices for household energy generally have been about 1/16 the size of natural gas spot price changes. Based on this rough relationship, a 250% increase in natural gas prices would generate about a 15% jump in the related CPI measure, which itself accounts for about 3.3% of the goods and services included in the CPI basket. Therefore, the massive 250% increase in natural gas prices could boost annual headline CPI inflation by about 0.5% (3.3%*15%).

By contrast, the prices for some other types of energy goods are much more responsive to changes in nat gas spot pricing. Motor fuel prices in the CPI, for example, move almost one-to- one with WTI oil prices....

....MUCH MORE

Going forward we'll be talking about wage-price inflation as workers attempt to regain some purchasing power and as we get closer to the big climate get-together in Glasgow a look at one cause of decreasing natural gas supplies in the West that I haven't seen mentioned anywhere. One hint for those readers unable to stand the frisson of the tease, we were posting on it in 2012 if you've been with us that long.