In the meantime Alphaville's David Keohane directs us to Macquarie's discussion of the current state of inflation.

From FT Alphaville:

You show me your inflationary impulse and I’ll show you mine

You may consider the below as a series of questions that need answering in the face of recent hopes (that’s the right word, yeah?) for a return of inflation.

You can see why hopes are being raised that this isn’t another false dawn:

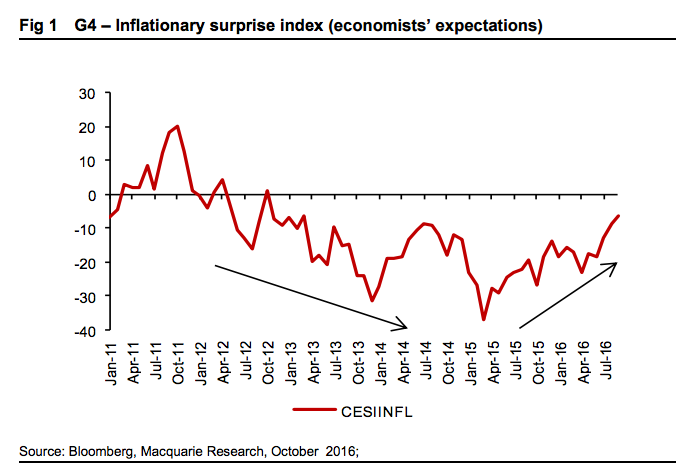

But, as Macquarie say echoing others, “at this stage, almost the entire inflationary impulse was caused by rapid recovery in commodity prices and the onset of the base effect.”What with the helpful arrows, Macquarie's charts must be especially handy for the directionally challenged community.

So…. the question becomes are there drivers for inflation outside of commods?Macquarie’s Victor Shvets, head of Asia strategy, and Chetan Seth say no:

Whether we examine core CPI, core PCE or core PPI, there are few (if any) signs of any significant inflationary pressures.And their argument is that there are good reasons for that since most of the real drivers here are structural: Secular stagnation and a “declining return on humans’ manifesting in a fall in the pricing power of labour, more of which below — making it “hard to see where pricing and inflationary pressure would come from.”...MORE

For example, in the US, core CPI remains broadly flat at around 2.2%-2.3% vs. the historic average of 3.8% over the 1960-2015 period or 2.8% average between 1985 and 2015. Similarly, PPI final demand remains stuck between 0% and 1% whilst the PPI final demand ex Food & Energy remains broadly flat at ~1.1%-1.2%. The same applies to trimmed PCE (1.6%-1.7%) as well as core PCE. Thus, even though headline CPI levels are very likely to exceed the Fed’s target of 2% in 1Q2017, it seems unlikely that core inflation gauges will reflect much pressure.

The same applies to Eurozone and Japan, although in a much more forceful and extreme manner. Eurozone core CPI continues to stagnate at ~0.8%-0.9% (even as headline CPI has moved into positive territory). The same largely applies to PPI, with core PPI (ex Construction & Energy) remaining negative 0.5%-1%. The situation is even more extreme in Japan, with CPI ex taxation, food & energy, barely budging (0.2%-0.3%) whilst the PPI remains negative (down 3%-3.5%). Headline CPI is also deeply in deflationary terrain.

Recently:

That Time the FT's Kaminska Beat the Telegraph's Evans-Pritchard To the Big Macro Story

If You've Noticed A Perma-Bid In Commodities, You're Not Imagining It

"The Fed's Game Changer?"

San Francisco Fed: "What Is the New Normal for U.S. Growth?"

...And A Quick Look At The Interplay Between Currencies and Inflation

That's the last couple weeks. If interested in more see the search blog box, upper left or the Google search of the site which shows 25,900 results. That can't be right:

site:climateerinvest.blogspot.com