Wow, I took my eyes off CalPERS and managed to miss them trying to pull a fast one about their long-term returns. Fortunately, blogger W.C Varones caught it and Michael Shedlock promoted his find. And in an admission that Varones and Shedlock were correct, CalPERS removed the claims they deemed to be misleading…and substituted a different on that is just as deceptive.

And what has CalPERS done? Quickly edited its site to try to maintain the pretense that its return targets are achievable, when in fact we are in a “new normal” that is punitive to long term investors, be they pension funds, insurers, or individuals.

CalPERS has been on the defensive since it reported preliminary returns for its fiscal year just ended of 0.6%, when its target is 7.5%. Even though the final return is certain to be a smidge higher thanks to private equity doing well in the quarter where the data is not yet in, it’s clearly not going to change the overall dismal picture. Moreover, this result is particularly disturbing that governor Jerry Brown pushed CalPERS, to no avail, to lower its target to a somewhat more realistic 6.5%. The giant pension fund responded by creating a Rube Goldberg formula that (in crude form) will lower the target in years where performance exceeds 7.5%. With central banks locked in super low, and tending to negative rates, and any exit from those rates leading inevitably to large losses on assets unless one is heavily in cash (which CalPERS will never do), pray tell where where does this outperformance fantasy come from? For instance, fiscal year 2015-16 looks to be a last hurrah for bonds, with CalPERS having earned 9.29% in fixed income. But none other than bond maven Bill Gross has since warned that record-low bond yields “aren’t worth the risk.”

Here is the misrepresentation that blogger W.C Varones called out. From his post on August 1:

You probably know that CalPERS recently reported yet another year of investment results that fell far short of its absurd promises.

But did you know that CalPERS is actively, deliberately deceiving the public about its investment promises and results?

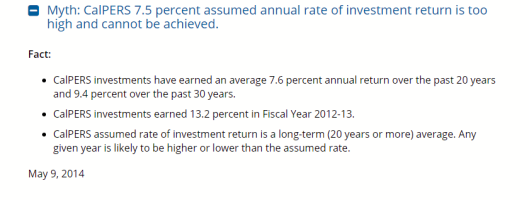

CalPERS has a section called “Myths vs. Facts” on its website where it tries to debunk critics of its rosy expected returns, which experts nearly universally believe are too high. Here’s what the site showed until mid-July:

This is a recurring theme of CalPERS propaganda: pay no attention to expert opinion, zero percent interest rates, or historically high valuations. CalPERS can always expect high returns because CalPERS earned high returns in the past.Long-time readers may remember the spokesperson spin back in March 2009:

After a second consecutive year of dismal returns, the statements above about 20- and 30-year returns are no longer true. This spreadsheet shows the past 21 years of returns, taken from CalPERS annual reports (we could not find data prior to 1996). CalPERS’ 20-year annualized return is now just 6.57%… and it’s about to go a lot lower because it is rolling off four more consecutive years of double digit returns from the tech/internet bubble.

Last year, CalPERS semi-acknowledged that it needed slightly less crazy assumptions, promising to eventually lower expected return… but only after it has a really good investment year first. That’s like a heroin addict promising to quit after just one more fix....MUCH MORE

Public pension funds’ rosy forecasts pose problems

...Last week we linked to a Bloomberg story "Hidden Pension Fiasco May Foment Another $1 Trillion Bailout", which took public plans to task. Here's CalPERS response via the Sacramento Bee's The State Worker blog:

Beware of the anti-pension ideologues who come out of the woodwork during market downturns. Like vultures, they prey on the highly charged and negative investment environment, looking for ways to convince you a temporary performance downturn will be typical for all time! They know -- but don't tell you so -- that we set our rates based on a fiscal year investment return. They don't tell you that our assumed rate of return is made based on advice from a range of experts within CalPERS and within the industry and that it is regularly evaluated every two to three years in public session. They don't tell you what you would learn from a textbook on pension management: that some years investment returns are as expected; other years, they will be more than expected and yes, some years they will be less than expected.

They don't tell you that over the last 24 years, we have exceed our assumed rate of return 17 times, and eight of those years were more than double the 7 3/4 percent assumed rate of return.Alrighty then....

(And here's an interesting fact: For five years after the Great Depression, there were multiple double digit return years.)

We will withstand the market swings, with our goal in mind: to achieve our assumed rate of return averaged over many, many decades. That's what we are designed to do. That's the math that matters.

Patricia K. Macht

Assistant Executive Officer

Office of Public Affairs