Investors are in for a lot of pain as Sharp Ratio reverts to mean.

Everyone’s familiar with the classic 60/40 investment portfolio. If you’ve ever dealt with financial advisors, this is the standard allocation they’ll recommend. 60% of your money in the stock market, and 40% in bonds.

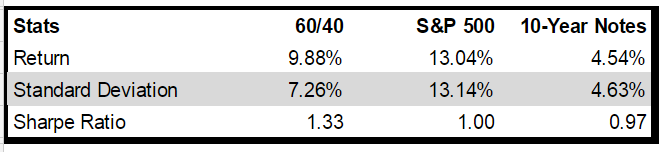

There’s no doubt this has been a great strategy the past few years. Check out the statistics from Jan. 1 2010 to Jan. 1 2016 below:

The standard 60/40 portfolio grew an average of 9.88% per year. And not only that, but the Sharpe ratio was at a stellar 1.33!

The Sharpe ratio is a standard industry measure for calculating risk-adjusted return.

Sharpe ratio = (Mean portfolio return − Risk-free rate) / Standard deviation of portfolio return

It takes the average return, subtracts the risk free rate, and then divides that difference by the standard deviation. The result is the excess return per unit of volatility. It basically tells you how much risk and volatility you had to endure for that extra return.

A high Sharpe ratio means you’re getting more excess return for less risk. So the higher this ratio is, the better.

Most quantitative hedge funds shoot for a Sharpe near or above 1. So 1.33 is really something. Especially considering that it’s coming from a simple 60/40 portfolio…

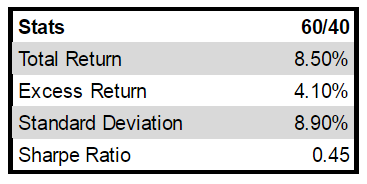

Now take a look at that portfolio’s statistics from 1946 to now:

See the Sharpe ratio? It’s only 0.45… much lower than our current period’s ratio of 1.33....MORE