From Alhambra Investment Partners:

Repo markets are flashing warnings again, as conventional

explanations fall short of full comprehensiveness. We learned today that

US treasuries across the curve are once again trading very special in

the repo market, meaning negative repo rates for US notes from 2 to 10

years in maturity. Technical factors play a role, as this week’s

auctions will change over the on-the-run CUSIPs (with the last auction’s

bonds shifting to off-the-run, they will no longer provide enough

liquidity to be more broadly accepted as collateral).

As Bloomberg explains,

“Many times traders short, or sell securities they’ve borrowed in the

repo market, ahead a Treasury sale to profit if prices of the securities

fall after the auction.” That is true, as far as it goes, but it does

not explain why there is suddenly so much special repo trading in 2013.

We have seen negative repo rates, all the way up to and past the 3%

fails penalty, in bonds such as the benchmark 10-year. The auction cycle

does not explain why 2013 has been so different in the repo “market”,

particularly why these specials seem to be persisting.

In fact, there have been quite a few wholesale money anomalies this year, from the gold smashes to eurodollar funding turmoil.

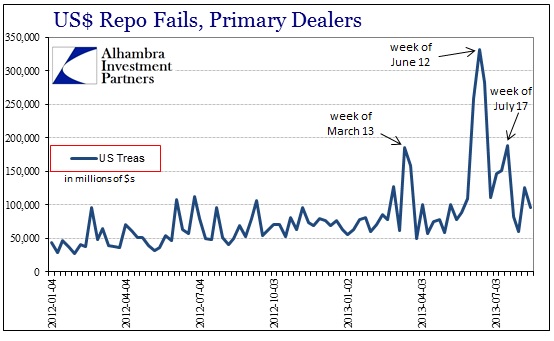

Starting from what we know with a high degree of clarity, there have

been three separate and significant spikes in repo market fails. A large

increase in repo fails can only be due to collateral shortages, so a

spike in fails shows any shortage becoming an operational problem.

The reason for the treasury shortage according to the conventional

narrative is an increase in “shorts”, or those betting on higher rates.

While that is correct in a certain sense, I think there is much more

nuance here that is necessary to tease out the complete funding picture

(with ramifications that flow destructively global, as we see now).

While shorting treasury bonds can be a primary source of specialness

in the repo markets, principally on-the-run, we cannot forget about

other trades driving collateral demand. I’m talking primarily about

derivatives trades, interest rate swaps in particular. In one of the

last bastions where mark-to-market is still enforced, swaps are

generally collateralized at the onset and then collateral is “called” up

and down as the market value of the swap contract floats with “market”

conditions. Banks and speculators have to settle positions, factoring in

netting, every day.

If I’m paying fixed to a bank counterparty that pays me floating in

return, when interest rates fall I will have to post additional

collateral to reflect that change in market value in the bank’s favor.

The opposite is true in the case where interest rates rise – the bank

would have to post the incremental collateral.

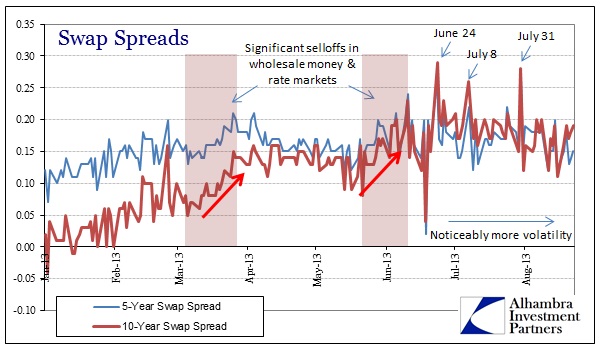

The behavior of swap spreads, in light of the impact on collateral

demand, aligns far too closely to the repo fails above to be mere

coincidence.

From March 6 through March 26, the 10-year spread moved up from 5bp

to 15bp, encompassing the whole of the first spike in repo fails. Then

from June 3 through June 11 the 10-year spread jumped from 14bp to 23bp.

The second spike in repo fails occurred the week of June 12....MUCH MORE