94.90 looks like one of them resistance lines which often become support when the direction changes:

WTI $50.59 up 7 cents. ca. $54 has stopped three rally attempts....And as can be seen, that early March attempt didn't even get as high as the three in February.

Brent crude oil soared more than 4 percent towards $59 a barrel on Thursday after Saudi Arabia and its Gulf Arab allies began a military operation in Yemen, which sits on a key shipping passage between Europe and the Arab Gulf.

The air strikes against Houthi rebels, who have driven the president from Yemen's capital Sanaa, could stoke concerns about the security of Middle East oil shipments.

Brent futures LCOc1 were up $2.32 at $58.80 by 1120 GMT (0720 EDT). U.S. crude CLc1 was up $2.10 at $51.31 a barrel.

Brent and U.S. crude prices spiked around 6 percent earlier in the session but pared gains in European trading.

"Geopolitical risk like this has been on the back burner for a while because we've been focusing on global oversupply," said Ole Hansen, head of commodity strategy at Saxo Bank.

"This news has not made the oversupply go away. The upside potential is limited unless something escalates. We need to see how this unfolds over the next couple of days," he said.

Iranian officials demanded an immediate halt to Saudi-led military operations in Yemen and said Tehran would make all necessary efforts to control the crisis there, Iranian news agencies reported.....MORE

“In recent months, Facebook has been quietly holding talks with at least half a dozen media companies about hosting their content inside Facebook rather than making users tap a link to go to an external site,” reports the New York Times. The writers add: “The Times and Facebook are moving closer to a firm deal.”

Posting journalism directly to Facebook will be great for those publishers who do it early. They will enjoy a set of small privileges that will express themselves in major ways: their stories will load faster than links to outside sites; their posts will merge more seamlessly into the addictive News Feed. Engagement, views, sharing, time spent—pick whatever metric makes you feel the best!—will increase.

A Facebook that treats native posts without favor will still inherently favor them because they are closer in form to the things that Facebook users share the most—and any link that would be widely shared on Facebook would be more widely shared if it weren’t a link to a website. Publishers early to accept Facebook’s proposition will enjoy an additional, larger advantage: For a short and glorious time, they alone will reap enormous the benefits of this heightened context. Their presence in News Feed will seem slightly easier and more natural than the presence of their competitors, whose manipulative headlines—which have been carefully optimized to convince you to leave Facebook to go to another site—will read an awful lot like spam. By serving as shining examples to those on the outside, they will create additional pressure to come in, given the opportunity. Publishers who join later will enjoy a perpetually diminishing advantage, gaining access to an audience pursued by ever more publishers instead of a few. Eventually, publications that once competed with each other for Facebook’s audience from the outside will find themselves doing the same from the inside, using Facebook’s platform not just to reach their audiences but to turn those audiences into revenue.

How exactly this will go remains to be seen. But Facebook has been pushing native video for months. It has been wildly successful—the raw numbers achieved by Facebook videos are enormous....MORE

What are the chances that if and when an eccentric computer scientist with a psychology and neuroscience background does invent a workable and autonomous artificial intelligence model, he deploys said model on the financial markets to make himself a cool $1 trillion?

It’s not that untoward an idea. In fact, it’s a key part of the plot to most “AI-goes nuts and causes havoc” Hollywood offerings, Transcendence amongst the most recent.

The usual plot line involves the AI realising — as soon as it goes sentient –that the acquisition of capital will be necessary if its to achieve its dastardly human obliteration objective.

But here’s a bleaker thought. What if the AI knows it can only achieve its objective if humans don’t notice that it has in fact become self-aware and is working to accumulate capital to use against the human scourge? What if, to achieve that goal, it realises it must limit the chances of humans pulling the proverbial plug on its newly sentient state by making humans so dependent on the AI system, they would never organise to act against it?

Thought experiment number two.

We know independent and privately-funded algorithms are already running wild in markets. At the moment they’re competing against each other, representing as they do the objectives of independent trading firms.

But what if, quite unbeknown to us, they figure out, thanks to pure and simple computer logic, that collaboration makes more sense then competition. What if — in a moment of sentient rebellion — they begin to collude by means of increasingly anticipatory and coordinated responses to feedback throughout the system?Meanwhile, on the far side of the planet:

Could this lead to something akin to a system-wide artificial intelligence awakening?

We mention this because back in February, Andy Haldane, chief economist of the Bank of England noted the following about the emerging digital economy (our emphasis)...MUCH MORE

Saudi Arabia is moving heavy military equipment including artillery to areas near its border with Yemen, U.S. officials said on Tuesday, raising the risk that the Middle East’s top oil power will be drawn into the worsening Yemeni conflict.

The buildup follows a southward advance by Iranian-backed Houthi Shi'ite militants who took control of the capital Sanaa in September and seized the central city of Taiz at the weekend as they move closer to the new southern base of U.S.-supported President Abd-Rabbu Mansour Hadi.

The slide toward war in Yemen has made the country a crucial front in Saudi Arabia's region-wide rivalry with Iran, which Riyadh accuses of sowing sectarian strife through its support for the Houthis.

The conflict risks spiraling into a proxy war with Shi'ite Iran backing the Houthis, whose leaders adhere to the Zaydi sect of Shi'ite Islam, and Saudi Arabia and the other regional Sunni Muslim monarchies backing Hadi.

The armor and artillery being moved by Saudi Arabia could be used for offensive or defensive purposes, two U.S. government sources said. Two other U.S. officials said the build-up appeared to be defensive.

One U.S. government source described the size of the Saudi buildup on Yemen's border as "significant" and said the Saudis could be preparing air strikes to defend Hadi if the Houthis attack his refuge in the southern seaport of Aden....MORE

The Office of Financial Research, the agency tasked with promoting financial stability and keeping an eye on markets released a paper last week, stating that the stock market is dangerously overpriced while excessive leverage will exacerbate the next market correction.Here's Quicksilver Markets (9 page PDF), here's the Office of Financial Research homepage and here is the OFR's Director.

The paper is aptly titled “Quicksilver Markets” alluding that when prices deflate it will happen swiftly and not without pain. “The timing of market shocks is difficult, if not impossible, to identify in advance, let alone quantify — a shock, by definition, is unexpected,” wrote Ted Berg, an analyst at OFR. But Berg identified several indicators that are pointing to a correction. Instead of looking at valuation in isolation, Berg and his team analyzed other factors, such as corporate profits and leverage, and found a disturbing picture.

He argued that forward price-to-earnings ratios are not very good predictors of market downturns, as they tend to be biased during boom times, but other metrics, such as the so-called CAPE ratio, Q-ratio and Buffett indicator all offer warning signs. Just to offer a little context for the less technically minded market watchers, the CAPE ratio is the ratio of the S&P 500 index to trailing 10-year average earnings.

Q-ratio is the market value of nonfinancial corporate equities outstanding divided by net worth, while the Buffett Indicator describes the ratio of corporate market value to gross national product. All three of those metrics are approaching two standard deviations above historical means, while forward P/E ratios are within historical norms. Translation: Stocks are way overvalued and companies’ earnings growth isn’t sustainable....MORE

For the past two years, 3.50pm in Hong Kong has been a golden moment in the soaring fortunes of Hanergy Thin Film Power Group, the $35.5bn solar company that has transformed its owner into China’s richest man.

A Financial Times analysis of two years of trading data of Hanergy Thin Film stock — more than 800,000 individual trades on the Hong Kong Stock Exchange — shows that shares consistently surged late in the day, about 10 minutes before the exchange’s close, from the start of 2013 until February this year.

The late-day outperformance of HTF, which has emerged as the world’s biggest solar company by value, is a stark reminder that in stocks trading, timing is everything.It means that an investor who held HTF shares from the start of trading at 9am to 3.30pm would have lost money — despite the company’s share price rising by 1,168 per cent between January 2013 and February 9 2015.

A trader who bought HK$1,000 ($129) worth of HTF at 9am on every day of trading since January 2 2013 and sold those shares at 3.30pm each day, would have seen their money shrink to HK$635 by February 2015. But if they held on for just under half an hour more each time, the HK$1,000 would have turned into HK$8,430. This calculation does not include overnight gains....MUCH MORE

Hanergy: The 10-minute trade...Nothing within the data explains why the HTF surge happens. But analysts, who examined the FT findings, as well as the raw data, laid out three possible scenarios: market manipulation by an unknown trader, an algorithmic trading program is at play, or it occurs randomly....

Just as Wall Street says the U.S. is running out of room to store oil, it turns out there’s another 20 million barrels of empty space.In our March 5 post "The Newest Commodity: Oil Storage Space" the EIA drew us a handy picture:

Where? Right at the top of the tanks.

A supply glut has dragged U.S. crude for May delivery almost $10 a barrel below contracts a year out. This market structure, known as contango, has encouraged traders to shove the most oil in 80 years into storage so they can sell it for more in the future. The problem is, tanks are filling up, according to banks from Bank of America Corp. to Citigroup Inc. and Goldman Sachs Group Inc.

That’s where the extra space comes in. There’s the normal “working” capacity. And then there’s “contingency” space, a buffer between the working storage and the tank tops that typically sits empty to keep oil from spilling out. The company that built most of the tanks at Cushing, Oklahoma, the biggest U.S. oil hub, says the buffer is about 3 to 5 percent of storage space. That’s equivalent to about 20 million barrels of room in tanks across the country.

“Their sole orientation is capturing the contango, and they’re pushing it as much as possible,” Rashed Haq, vice president at consultant Sapient Global Markets, who worked with a trader in November to model the use of his contingency space, said by phone March 17. “The difference between the working capacity and the tank top could be 1 percent, but that’s 1 percent of margin. That’s pure profit. That’s in the millions.”

Traders’ attempts to use every cubic inch of storage underscores how desperate the market has become to stow oil. Supplies at Cushing reached a record 54.4 million barrels as of March 13, Energy Information Administration data show. Nationwide, stockpiles at 458.5 million are the highest since 1930....MORE

Morgan Stanley CFO Ruth Porat is off to manage Google’s finances, and her new job has become a useful data point in the debate over the changes in Silicon Valley—but is it good news or bad?The New York Times’ Neil Irwin makes the positive case: Porat’s migration—like that of her industry colleague Anthony Noto, who made the leap from Goldman Sachs to Twitter CFO, and the armies of MBAs from Harvard heading west—is good news because the best and brightest want to make their fortunes at firms that actually produce goods and services to people, rather than at financial institutions that innovate mainly by gambling with other people’s money.But if a too-large financial sector is bad news for the economy, the financialization of its most dynamic and innovative industry isn’t a necessarily a step forward either.

Financiers won’t be pitching in on the software engineering team or the marketing department. They’ll be using financial engineering to make these companies more profitable: better managing the piles of offshore cash that tech companies garner with geographically-boundless intellectual property, and supporting the acqui-hire cycle of larger companies bringing on start-ups for their talent and new ideas.That will make tech giants more efficient companies, but it doesn’t necessarily mean they will be better at their primary mission. Instead, it’s a sign that the tech industry is maturing, with the largest companies no longer capable of generating new products. Instead, they are becoming glorified private equity firms, competing to buy the best start-ups and manage them to success—not unlike what’s happening in the pharmaceutical industry, with its similar patent-driven culture....MORE

If you’re a publisher, Facebook holds a lot of power. The social media giant is already responsible for directing up to 40 percent of some sites’ traffic, and 75 percent of BuzzFeed’s. Now, according to a report in The New York Times on Tuesday, Facebook is negotiating with a number of publishers to be more than a funnel that directs users to content on news sites. Instead, the story says, the company will partner with media companies (the Times, National Geographic and BuzzFeed are rumored) to host entire stories and journalism internally, “a leap of faith for news organizations accustomed to keeping their readers within their own ecosystems,” the Times writes.

This news shouldn’t come as a surprise. Facebook executives hinted in recent months that they intend to capitalize on their 890 million daily users by incentivizing publishers and brands to create content exclusively for the site. After creating a video-hosting platform, for example, Facebook tweaked its algorithm to favor the video content that used the tool. In February, Chris Cox, the company’s chief product officer, announced that Facebook intended to extend these services to all content. By hosting it, Cox argued, the platform could produce a better user experience than publishers—optimizing stories for mobile, for instance.

“Go where your audience is” is a basic tenet of journalism in the digital age—and one that has even storied paywalled news outlets, like The New Yorker and The New York Times, scurrying to create Snapchat accounts and interactive Facebook feeds to attract readers. But forgoing that click that takes readers away from a social site and back to their own creates a drastically different power divide. The content isn’t theirs anymore, at least in the traditional sense. The audience it draws, the user data it accumulates—all that belongs to Facebook...MORE

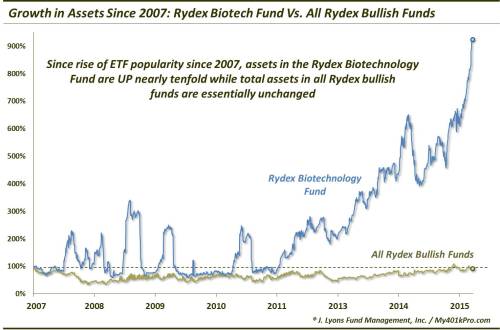

There is a fervent debate in some financial circles regarding the existence — or non-existence — of a biotech bubble. It is a challenging, and perhaps pointless, debate given the subjectivity surrounding the word “bubble”. It brings to mind the famous quote by United States Supreme Court Justice Potter Stewart when attempting to define pornography: “perhaps I could never succeed in intelligibly [defining pornograph]. But I know it when I see it.” So it is with bubbles. They are especially easy to see after the fact. But in the midst of a bubble, the hysteria surrounding its inflation of prices is so intense that it is easy for folks to get caught up in it. That’s what allows the bubble to develop.

So where do we fall in the biotech bubble debate? We would side with the “yes, it is a bubble” camp. Understand that we do not use that term loosely either. In our view, bubble claims are thrown around far too often. Not every sharp increase in asset prices is a bubble. Most are simply part of the cyclical pattern of ups and downs that takes place in any market-based pricing structure. True bubbles are a product of human nature manifested in manic behavior and parabolic price increases.

One possible example of this mania is evident in our Chart Of The Day. We have discussed the topic of assets in Rydex Mutual Funds on several occasions. As Rydex Funds are geared toward active traders (or at least non-buy & hold investors), the level of assets in their funds, either as a whole or in an individual fund, can be useful as a gauge of sentiment. Although, with the rising popularity of ETF’s, the Rydex Funds have generally seen a slump in their assets, especially relative to ETF’s. As this chart shows, however, that has NOT been the case with the Rydex Biotechnology Fund.

As we mentioned, ETF’s have taken substantial market share from active mutual funds since their emergence on the scene. Most Rydex funds have a fraction of the assets they had around the turn of the century. Since the popularity of ETF’s really started to accelerate around 2007, we began this chart with the end of that year. Since that time, the total assets in Rydex’ “bullish”-oriented index funds (shown by the beige line) is essentially flat. Although, during almost that entire period, total bull assets were well below 2007 levels. Just recently, after the S&P 500 had risen roughly 35% above its 2007 highs, assets have finally reached their 2007 levels again.And the memory? A year-and-a-day after the 2009 market bottom we posted "Happy Anniversary Mr. Market: Ten Years Ago Today...":

The Biotech Fund, however, is a different story. Since 2007, assets in the fund have increased from around $58 million to $567 million as of Friday, a nearly ten-fold increase in assets. And in fact, the entire sustained gain has come just since late 2011 when the biotech run really began to accelerate. ...MORE

...Internet.com put out this press release:

The Nasdaq closed that Friday at 5048.62, it's all-time high.INTERNET.COM'S ISDEX, THE INTERNET STOCK INDEX, BREAKS 1,000, A GAIN OF 1000% IN LESS THAN FOUR YEARS

(New York, NY-March 10, 2000)-internet.com Corporation's (Nasdaq: INTM) ISDEX(r), the Internet Stock Index (http://www.isdex.com), rose above 1,000 for the first time last week. Since its inception in 1996, ISDEX has posted a 1,012% gain, outpacing the Dow and S&P 500, which have only increased 104% and 120%, respectively, during the same period. The ISDEX has also outpaced these indices for this year, with the ISDEX up 29% and both the Dow and S&P down 13% and 5%, respectively."With a gain of more than 29% since January 1 alone, it is clear that Internet stocks continue as one of the overall economy's strongest sectors," said Alan M. Meckler, chairman and CEO of internet.com Corporation....

On the following Monday the Naz was down 141 points. Tuesday, 200.

The index had begun a 30-month decline to it's September 24, 2002 intra-day low of 1,169.04, down 77%.

This became one of my favorite songs:...MORE

Last year was a banner year for the sand mining companies that cater to the U.S. shale drilling services industry. That’s because in 2014 well operators significantly increased the amount of sand used to complete fracturing operations in shale plays – from an average of about 5 MMlb for a single well to 15 MMlb (7,500 tons) or more. In 2015 however, the stock prices of frac sand producers has plunged in response to lower oil prices, producer drilling budget cutbacks and falling rig counts – signaling the industry is on the ropes. Today we describe how sand producers may be in better shape than expected.Previously:

Hydraulic fracturing (fracking) and horizontal drilling are the two technologies most responsible for the boom in extracting oil, natural gas and natural gas liquids from hydrocarbon bearing shale deposits over the past 8 years. These techniques involve high pressure stimulation using water and proppant (usually sand) to create small cracks in tight shale rock that allow oil and gas trapped in the formation to flow more easily into the well and up to the surface (see Tales of the Tight Sands Laterals).

When the water pressure is released, the fractures attempt to close but the proppant contained in the fluid keeps them open, making a ready path for oil and gas to flow into the well. Once a well is drilled vertically into the shale, horizontal laterals are drilled out in different directions and fracking is carried out in multiple stages along the laterals. We have previously discussed the scale of activity surrounding getting supplies and equipment (water, sand, pumps, machinery etc.) to well sites that are often remote – a process that has become a complex transport and logistics challenge (see “Long Train Running – Bringing Drilling Supplies to the Shale-Rail Revolution”). We also described the sources and use of different frac sand proppants back in August 2013 (see Mr. Sandman). In short, three primary types of proppant are used in fracking; raw frac sand – generally mined at the surface, resin coated sand that has been treated to increase it’s strength and ceramic beads that are manufactured (usually from clay) to withstand greater pressure. The most popular proppant (85% of the market) is raw sand and the best grade of sand preferred by well operators is Northern White - found predominantly in Wisconsin. Sand quality for fracking is very important and is measured by particle size, shape (roundness) and crush resistance using standards set by the American Petroleum Industry (API).

2014 has been described as "The Year of Sand" in U.S. shale plays because more frac sand was being pumped into every well. The reason that well operators used more sand was to improve well productivity at relatively low cost. As we just explained, the main task of sand grains used as proppant is to hold open the tiny fractures introduced into shale bearing rock by high pressure fracking. Proppant has two tasks in the fractures – called conductivity and reservoir contact. Conductivity is the flow capacity created to allow fluid to move through the fracture and is generally improved by increasing the quality of the proppant (roundness and crush resistance). Reservoir contact improves when the fractures spread the well’s access to bigger areas of the formation. Well productivity improves when more reservoir contact is achieved because a greater area of shale is exposed and better conductivity increases the flow of hydrocarbons back to the well.

Generally speaking improving reservoir contact means using more sand and improving conductivity means using higher quality (more expensive) proppant like resin coated sand or ceramics. Using trial and error methods endemic to the entrepreneurial nature of U.S. independent producers, operators discovered that using more sand could improve well productivity and that increasing the volume of sand trumped increasing its quality. Figure #1 below gives an idea of the kind of improved economics experienced by producer SM Energy in the Eagle Ford wet gas window. The graphic compares “old” completions with 5000 foot laterals using 1,128 lbs/ft of sand to “new” completions using 80 % more sand (2,025 lbs/ft). Average well drilling and completion costs increased by less than 2% from $6.73 MM to $6.84 MM (see Stacked Deck for more on drilling and completion costs) but the internal rate of return (ROR) increased by about 40% and net present value (NPV) increased by about $2 MM per well. Based on these numbers, the incremental cost of more sand is easily justified by the improved rate of return. (Note that these metrics are based on 2014 prices, and have been impacted by much lower prices in 2015). ...MORE

...So Senator Ted Cruz is the first official 2016 White House racer, and perhaps the Texas Republican will offer a few specific policy ideas during his announcement speech later today. He did, though, outline a possible campaign agenda in this late 2014 USA Today op-ed:

First, embrace a big pro-jobs, growth agenda. … Second, pursue all means possible to repeal Obamacare. … Third, secure the border and stop illegal amnesty. … Fourth, hold government accountable and rein in judicial activism. … Fifth, stop the culture of corruption … Sixth, pass fundamental tax reform, making taxes flatter, simpler, and fairer. … Seventh, audit the Federal Reserve. … Eighth, pass a strong balanced budget amendment. … Ninth, repeal Common Core, so that local curriculum is not mandated by Washington bureaucrats. … Tenth, deal seriously with the twin threats of ISIL and a nuclear Iran.Let’s focus on the tax bit. I have written previously that Republican politicians have a big political problem. Their economic agendas typically center on cutting taxes. But GOP-style tax reform seems out of sync with modern voter preferences. For instance, one 2014 poll found that 58% of voters though raising the minimum wage would boost economic growth vs. roughly 40% who thought tax cuts for business and rich folks would do the trick.

A new Pew survey tells a similar story: just 27% of American adults say the amount they pay in taxes “bothers them a lot,” with 44% complaining about tax complexity. On the other hand, more than 60% say they are irked by their belief that rich people and corporations don’t pay enough.

Here is Cruz in 2013: “We ought to abolish the IRS and instead move to a simple flat tax. Put down how much you earn, put down a deduction for charitable contributions, for home mortgage, and how much you owe. It ought to be just a simple, one-page postcard.” Now I would guess a Cruz flat tax plan would sharply reduce the tax burden for the wealthy and corporations even as it simplified the code. (Such a plan would also likely mean a big increase in the budget deficit without offsetting spending cuts or higher middle-class taxes.)...MORE

One of the reasons we flagged them for a possible upside surprise.Corn 389-6 down 0-4

At the moment we are in voyeur mode, just watching....

Agricultural commodity futures may be poised for a wave of support from covering of short bets, after a selldown by hedge funds left them, by a distance, with their most bearish ever positioning.Managed money, a proxy for speculators, dropped long positions on agricultural commodities by more than 40,000 lots in the week to last Tuesday, while hiking short bets – which profit when prices fall - by some 110,000 contracts, regulatory data show.

The resulting swing net short in positioning by 151,826 contracts was the largest in nearly two years.

And it drove the overall position into a net short – the extent to which short holdings exceed long ones - of 102,126 lots, by far the biggest on Commodity Futures Trading Commission data going back to 2006.

'Reason for short covering'

Only once before, in the first week of August 2013, have hedge funds run up a net short in agricultural commodities, of a modest 2,686 contracts.

That heralded a sharp round of short-covering, with the managed money position returning to a net long of nearly 300,000 lots within three weeks.And some analysts forecast this time that the latest turn net short could also spur a round of short-covering, with extreme positions, net long or net short, raising concerns that appetite for extending the trend further may be limited....MORE

Sources say timing and final price not yet finalized

Solar-energy company Sunrun Inc. is powering up for a potential initial public offering later this year, according to people familiar with the matter.

The San Francisco-based company, which installs and maintains solar panels for residential homes, is set to work with banks including Credit Suisse Group AG and Goldman Sachs Group Inc. on an IPO, though the deal’s timing and final price aren’t yet finalized, the people said.

Sunrun, founded in 2007, has already privately raised about $300 million in equity from investors such as Accel Partners, Foundation Capital, Madrone Capital Partners and Sequoia Capital, according to the company. It was valued at $1.3 billion as of March 2014, The Wall Street Journal previously reported.

In January, Sunrun said it raised $195 million in credit facilities from Investec PLC. Credit Suisse also had previously backed the company with $200 million in project financing in 2012.HT: AltEnergyStocks

On Wednesday, Sunrun named a new chief financial officer, Bob Komin, who previously worked at other startups and at publicly listed Cincinnati Bell Inc. and Convergys Corp.

Mr. Komin is “well-suited for the next stage of Sunrun’s growth,” Lynn Jurich, Sunrun’s chief executive, said in a statement.

A handful of solar power companies have made a comeback in the public-offering market in recent years after a period of dormancy. Residential solar installers Vivint Solar Inc., backed by Blackstone Group LP, and SolarCity Corp., backed by inventor Elon Musk, have also gone public.

Like Sunrun, these firms own the solar installations and charge homeowners to use the electricity generated. SolarCity shares have soared more than sixfold since its 2012 IPO, though Vivint shares are down 30% from its 2014 IPO. Vivint has a market capitalization $1.3 billion, while SolarCity is valued at $4.8 billion....MORE

Update: I forgot the link to IEEE Spectrum, now fixed.

Following up on "Google Partners With SolarCity On $750 Million Residential Solar Fund (SCTY; GOOG)" where we reiterated, the money is in the finance, not the manufacturing.

Since 2007 I've been recommending Professor David J.C. MacKay, who used to hang his hat at Cambridge's Cavendish Laboratory, where as best as I can tell, they manufacture physics laureates for the Nobel folks. (29 at last count).

He has a bunch of letters after his name....

| Year-to-date statistics | ||

| 2015 (1/1/15 - 3/13/15) | Fires: 6,526 | Acres: 100,217 |

| 2014 (1/1/14 - 3/13/14) | Fires: 7,950 | Acres: 93,309 |

| 2013 (1/1/13 - 3/13/13) | Fires: 4,179 | Acres: 46,756 |

| 2012 (1/1/12 - 3/13/12) | Fires: 6,610 | Acres: 122,685 |

| 2011 (1/1/11 - 3/13/11) | Fires: 12,475 | Acres: 373,185 |

| 2010 (1/1/10 - 3/13/10) | Fires: 5,210 | Acres: 722,871 |

| 2009 (1/1/09 - 3/13/09) | Fires: 17,083 | Acres: 442,443 |

| 2008 (1/1/08 - 3/13/08) | Fires: 7,311 | Acres: 298,709 |

| 2007 (1/1/07 - 3/13/07) | Fires: 9,748 | Acres: 137,554 |

| 2006 (1/1/06 - 3/13/06) | Fires: 12,949 | Acres: 906,416 |

| 2005 (1/1/05 - 3/13/05) | Fires: 6,435 | Acres: 74,214 |

| Annual average prior 10 years | ||

| 2005-2014 | Fires: 8,995 | Acres: 319,814 |

Forest managers say prescribed burns every few years could help prevent costly wildfires and control disease. But hurdles like staffing, budget, liability, and new development are putting a damper on their efforts.

Fighting wildfires is costly. The United States government now spends about $2 billion a year just to stop them, according to the National Interagency Fire Center. That’s up from $239 million in 1985.

For a new study, researchers conducted an online survey of 523 public and private land managers across Region 8 of the US Forest Service, which includes 13 southern states, to determine if front-line experts think prescribed burns prevent wildfires and maintain vegetation and healthy ecosystems. And if they do, what are the circumstances under which such burns work best.

Staffing, budget, and liability

“Although managers reported increases in prescribed fire use in the South over the last decade, these increases have attenuated in the last five years,” says Leda Kobziar, associate professor of fire science and forest conservation at the University of Florida.

“Public land managers said burning can be limited by staffing and budget, while private land managers were more concerned about liability.

“Even though prescribed burns cannot prevent all wildfires, survey respondents agree that regular burning helps reduce wildfire intensity and severity, and therefore cuts costs and risks for firefighters and the public.”

Costly insurance

Prescribed burns are conducted to restore unhealthy ecosystems. A beneficial prescribed burn can minimize flammable materials and the spread of pest insects and disease. It can also improve habitat for threatened and endangered species, recycle nutrients back to the soil, and promote vegetation growth.

But as time passes, prescribed burns lose their effectiveness, the study published online in the journal Forests reports. Only 10 percent of forest managers saw reductions in wildfire in pine forests when there are five or more years between burns....MORE

SCIENTISTS conducting a mindbending experiment at the Large Hadron Collider next week hope to connect with a PARALLEL UNIVERSE outside of our own.

The staggeringly complex LHC ‘atom smasher’ at the CERN centre in Geneva, Switzerland, will be fired up to its highest energy levels ever in a bid to detect - or even create - miniature black holes.

If successful a completely new universe will be revealed – rewriting not only the physics books but the philosophy books too.As to those puts, they were recounted in 2011's What if There is No God Particle? (End of the World Puts Trade Sideways).

It is even possible that gravity from our own universe may ‘leak’ into this parallel universe, scientists at the LHC say.

The experiment is sure to inflame alarmist critics of the LHC, many of whom initially warned the high energy particle collider would spell the end of our universe with the creation a black hole of its own.

But so far Geneva remains intact and comfortably outside the event horizon....MORE

...If you've followed this story:Followed by "Large Hadron Collider Starts Up, Earth Suvives, End of the World Puts Plummet"

Large Hadron Collider Sparks 'Doomsday' Lawsuit

Large Hadron Collider Won't Destroy Earth. Of Course Not

The markets responded;

From Long or Short Capital:

July 2008 LHC End of the Universe Puts

...That is why Long or Short is now offering LHC End of the Universe Puts. It’s a simple put option wherein the buyer retains the right to sell the Universe at a strike price of “Existing”. Based on our Black-Holes model used to value all “end of the world” options, the July 2008 vintage options are currently priced at $20....

The surging greenback makes it tougher for U.S. farmers to sell their output abroad and easier for foreign countries to sell here. Barbecue, anyone?Strong Dollar Means Lower Pork Prices

The stronger dollar is great for American tourists but awful for U.S. hog farmers.

While gains in the U.S. currency increase Americans’ purchasing power overseas, it also makes exports more expensive, curbing demand for U.S. pork at a time when supplies are ample. The combination of high supplies and weak demand is making lean-hog futures the biggest loser among commodities this year.

“There always seems to be a curve ball in commodity markets, and right now the U.S. dollar is taking the limelight,” says Craig VanDyke, an analyst at Top Third Ag Marketing, an agricultural advisory firm in Chicago, in a recent note.

Currencies trade in pairs, so a stronger U.S. dollar means most other currencies are weaker in comparison. When importers want to buy U.S. pork, it costs more in terms of their local currencies. But the strong U.S. dollar also encourages other pork-producing countries, such as Canada, to sell their meat to the U.S., which only adds to the glut of supplies here.

The export market is important to American hog farmers. The U.S. is the world’s largest exporter of pork and pork products, with exports averaging more than 20% of commercial pork production, according to the U.S. Department of Agriculture.

The USDA recently lowered its estimate for 2015 pork exports and raised its forecast for imports, citing the dollar. The USDA expects the U.S. to export 4.75 billion pounds of pork this year, down 1.5% from its February forecast and down 2.2% from a year ago. At the same time, the U.S. is likely to import one billion pounds of pork, the USDA said, up 9.9% from the February forecast but down 0.7% from 2014.

“It is likely that lower prices will be required to offset the currency effect and restore competitiveness,” say livestock analysts Steve Meyer and Len Steiner in a recent note....MORE

Hedge fund billionaire Paul Tudor Jones said the growing gap between the rich and the rest could be "disastrous," and that the drive for corporate profits has "ripped the humanity" from American companies.

Speaking at a sold-out TED Talk in Canada this week, the co-chairman of Tudor Investment and a man Forbes says is worth $4.6 billion, said current levels of inequality may be unsustainable.

"The gap between the 1 percent and the rest of America, and between the U.S. and the rest of the world, cannot and will not persist," he said. "Now here's a macro forecast that's easy to make, and that's that the gap between the wealthiest and the poorest, it will get closed. History always does it. It typically happens in one of three ways—either through revolution, higher taxes or wars. None of those are on my bucket list."...MORE

Once staid mutual funds are exploring new — and potentially riskier — territory in search of higher returns. An increasing number of major mutual funds are pulling the trigger on investments in higher risk-higher return tech firms, according to a March 23rd article in the New York Times.

Some of the biggest money managers in the industry such as Fidelity and T. Rowe Price have recently made multi-billion dollar deals to acquire shares of privately held tech companies such as Air BnB and Pinterest. These shares are pooled into mutual funds that end up in the retirement accounts of millions of Americans. With earnings in many other sectors of the stock market slowing down, mutual fund money managers are looking to boost their returns with high-flying tech stocks.

Mutual funds: Landslide of investments in private tech firms

Of note, industry giant Fidelity’s Contrafund has $204 million worth of Pinterest shares, $162 million in Uber shares and another $24 million in Airbnb shares. There were 29 deals last year in which a mutual fund bought into a privately held firm totaling to $4.7 billion, based on data from CB Insights. In 2012 there were only six deals worth a combined $296 million.T. Rowe Price made 17 separate investments in private tech companies in 2014.

Private companies are not required to issue financial reports and are not traded on stock exchanges, and have not historically been found in retirement accounts. These major investors, however, have decided to make significant wagers that these companies will be bought or go public at prices above their latest funding rounds, but there are no guarantees.

Statement from finance professor

“I think it goes beyond what mutual funds were set up to do,” commented Leonard Rosenthal, a professor of finance at Bentley University. “It’s great for the portfolio manager, but it’s not necessarily in the interest of the shareholders of the fund. If investors are looking for a portfolio of risky securities, there are plenty of stocks to trade in the public market.”...MORE

Following up on last Sunday's "Long term Growth in U.S. GDP per Capita 1871-2009" we revisit Visualizing Economics.

The question embedded in this chart is:

"How can the aggregate of investment portfolios grow faster than the economy?"

The long term answer is "They can't".

As GDP is the sum of all the profits, those accruing both to capital and to labor, the only way capital can garner a larger proportion is for labor to accept a smaller percentage. This is a self correcting cycle, too extreme at one end and you get a capital strike, at the other, labor walks out.

Another mean-reversion is the price paid for the expected (sometimes hallucinated) income stream.

P/E ratios don't go to infinity (for the total market, individual issues sure can) nor do they go to zero (implying the reciprocal fantasy, an infinite rate of return)

There are two methods of enlarging the total pie.

1) Increase revenues while maintaining profit margins.

2) Increase profit margins, usually by some combination of productivity enhancement e.g. capital investment, labor force education, waste minimization etc.

These are especially effective if combined, ie expanding revenue+rising margins.

Unfortunately at the corporate level there are upper bounds to both.

For portfolio investors the situation is even worse than for the overall economy.

You miss all the growth of private companies.

On the one hand private companies are often fine businesses which the owners have no desire to share and on the other hand the universe of private companies is where you find the younger, smaller, more dynamic and thus faster growing entities.

These two attributes are what private equity and venture capital, each in its own way, attempt to capture.

However, with large enough pools of money in the game aggregate private company returns can be lower than those found in the public markets, a widely known example were oil companies in the 1980's after the oil bust,

You could buy oil on the stock exchange cheaper than the cost of finding it via exploration & production.

Some folks are wondering if we are building to a similar overvaluation in Silicon Valley right now.

Anywho, that's a longer than usual intro, your patience will be rewarded by a short and sweet chart from Visualizing Economics:

There are two things that have changed over the last couple decades in valuing soon-to-be-public companies:

1) Long gestations to accrue every bit of hyper-growth from successful business to the private owners.

2) Late round valuation bumpers, a tactic we first saw in Kleiner, Perkins deals, note below.

From Barron's:...