At first glance, President Vladimir Putin's Russia may seem like a traditional rogue dictatorship whose actions are impossible to predict. In reality, it's a crony capitalist state with relatively open markets. That means you can always know what's going to happen slightly in advance by following the financial dealings of insiders.

Two Ph.D. students at Cornell, Felipe Silva and Ekaterina Volkova, recently confirmed that after analyzing Russian stock trades ahead of Russia's annexation of Crimea. In a yet unpublished paper, they show that insiders began selling stocks while outside observers, even sophisticated ones, were still struggling to accept the possibility of an armed Russian attack on Ukraine.

Silva and Volkova's research is based on the concept of probability of informed trading, originally developed in the mid-1990s by David Easley and Maureen O'Hara, also of Cornell. The researchers developed a way to track something they call Volume-Synchronized Probability of Informed Trading (VPIN). Essentially, it's the share of trading orders that are likely made by informed participants or insiders, based on their ability to correctly anticipate a move in prices. If the VPIN value for a stock or index rises sharply compared to an historical benchmark, it means insiders have become a lot more active. That suggests a momentous event is probably coming. The VPIN model predicted the Flash Crash of 2010 two hours before it took place.

Silva and Volkova applied the model to trading in 161 Russian stocks and the RTS index futures between Jan. 6 and April 4, 2014. For the RTS futures, the typical VPIN is 34 percent, compared with 22.5 percent for the E-Mini S&P 500 futures. (That doesn't mean a third of the orders are usually placed by criminals using illegal insider information; VPIN broadly defines "insiders" as people with better information than others.)...MORE

Wednesday, February 25, 2015

Predict Putin's Next Moves By Tracking Crony Insider Trading

From Bloomberg:

Larry Summers' Feb. 19 Speech: "Reflections on Secular Stagnation"

From the blog of Lawrence H. Summers:

Summers gave the keynote address at Princeton University’s Julius-Rabinowitz Center for Public Policy 4th Annual Conference on February 19, 2015. In his remarks, Summers gave his perspective on the “profound macroeconomic challenge of the next 20 years in the industrial world: secular stagnation.”

Lawrence H. Summers

Speech at Julius-Rabinowitz Center, Princeton University

February 19, 2015

Thank you for those generous words. I am glad to be here, glad to see so many old friends, my former Treasury colleague Josi Chapmen, from whom I learned much of what little I know about the international economic interactions relating to Europe. My former student, and then government colleague, Alan Krueger, whose work has illuminated so much to do with the working, or the non-working, of labor markets. My friend David Wessel, who’s covered my activities in government for many, many years at the Wall Street Journal. I can now tell you that on any occasion when I looked good, it was because he was reporting accurately. On any occasion when I looked bad, it was because he did not have an accurate rendering.

I just want to say, before I launch into my topic, that as someone who has spent his life, in a way, shuttling back and forth between government and university, I think that conferences like this one, and centers like the one that it’s convened in, are really profoundly important. If, for example, the United States has had a more successful response for financial crisis than Europe or Japan, it is importantly because of the kind of close connections between the worlds of thought and the worlds of action, that the American system makes possible. I believe the cultivation and support of worldly academic research in economics is something that is very, very important. I also believe that economic ideas, when either right or wrong, spur change and spur progress. When right, they make an important contribution. When wrong, they provide important clarification that ultimately proves to contribute to public policy.

What I’d like to do today is talk about my perspective, and I’ll try to recognize that there are multiple perspectives, on what seems to me to be the profound macroeconomic challenge of the next 20 years in the industrial world, and that is a problem of what I like to call secular stagnation, following Alvin Hansen.

I’m going to talk about six things. I’m going to talk about why we’re talking about secular stagnation, the dismal performance of the industrial world in recent years. I’m going to talk about the secular stagnation hypothesis, as Hansen framed it. Talk about what’s the central element in that, the low level of real interest rates. Reflect on some of the challenges that have been posed to the hypothesis, and then discuss what is it to be done.

This shows you US economic performance since 2007, measured relative to what we aspired to in 2007. What you see is that the economy went off a small cliff between 2007 and 2009 and that relative to what we aspired to in 2007, there has been no catch-up. The GDP gap is indeed smaller than it was in 2009, but that is entirely because our judgments about potential has been revised downwards, in the face of dismal performance. If anything, the picture is worse. In Europe, where there’s been essentially no progress, and where the gap relative to potential as we had assumed it would be, has steadily increased, and is continuing to increase. Of course, this is all reminiscent of the Japanese experience, and it would be be a rough summary of macroeconomics in this decade to say that Japan is the old Japan, and Europe is the new Japan. Europe today looks very much like Japan did seven or eight years post-bubble. Demographically challenged, incipiently deflating with severe financial strains, with dysfunctional politics, and ineffective decision-making....MORE

PowerShares ‘Temporarily’ Halts Creations in 11 Commodity/Currency ETFs (DBC; UUP)

From Barron's Focus on Funds:

Fund company PowerShares “temporarily suspended” share creations in nearly a dozen commodities and currency exchange-traded funds on Wednesday as it assumes full responsibility for those funds’ management.

The suspension affects 11 ETFs including the $4 billion PowerShares DB Commodity Index Tracking Fund (DBC) and the $1.2 billion PowerShares DB Dollar Index Bullish Fund (UUP), and curtails the ability of specialized dealers to create new ETF shares, possibly increasing investors’ trading costs.

PowerShares said it will “work quickly” to file necessary paperwork with Securities and Exchange Commission and National Futures Association to allow for normal functioning. PowerShares is the fourth largest U.S. ETF provider and a unit Invesco (IVZ). In October, the company said it would take over complete responsibility for the funds, which had been run jointly with Deutsche Asset & Wealth Management. PowerShares had previously been in charge of the ETF suite’s marketing and distribution.

In the ETF market, so-called authorized participants work continuously to create and destroy shares to align an ETF’s market price with the value of its underlying securities. If no mechanism exists to create new shares exists, the funds’ prices have potential to veer away from their net asset values, like a closed-end fund. In other words: beware....MORE

"Be Calm, Robots Aren’t About to Take Your Job, MIT Economist Says"

I'm open to a convincing argument but I don't think this is it.

From Real Time Economics:

From Real Time Economics:

David Autor knows a lot about robots. He doesn’t think they’re set to devour our jobs.

MIT economics professor David Autor says, “If we automate all the jobs, we’ll be rich.”

As an economics professor at the Massachusetts Institute of Technology who focuses on the impact of automation on employment, he’s in a good position to know. He’s surrounded by people creating many of the machines behind the latest wave of techno-anxiety.

His is “the non-alarmist view,” he says.

The 50-year-old believes automation has hurt the job market—but in a more targeted way than most pessimists think. He also doesn’t see the automation wave killing a wider array of jobs as quickly as many predict. Machines are invading the workplace, but in many cases as tools to make humans more productive, not replace them.

His research—presented in August to a packed audience of international central bankers in Wyoming—shows middle-skill jobs like bookkeeping, clerical work and repetitive tasks on assembly lines are being rapidly gobbled up by automation. But higher-paying jobs that require creativity and problem-solving—often aided by computers—have grown rapidly, as have lower skilled jobs that are resistant to automation, resulting in a polarized labor market and stagnant wages.

But many other economists and tech-watchers are ringing a louder bell.

“We’re entering an era where human beings are becoming dispensable in more parts of the economy and at a faster rate than ever before,” said Vivek Wadwa, a futurist at the Rock Center for Corporate Governance at Stanford University.

A recent Pew survey found just under half of technology experts said automation would displace “significant numbers of both blue- and white-collar workers” over the next decade. Some said it would leave “masses of people who are effectively unemployable.” But the other half said it will create more jobs than it destroys.

Mr. Autor—who always sports a single gecko-shaped silver earring, his trademark symbol also pasted on his iPhone—says the fear has outpaced reality. Automation is advancing, but we are still far from the day when machines can do complex physical and mental tasks that are easily and cheaply done by humans.

He encourages people to watch online videos of robots developed for the Pentagon, some built by his MIT colleagues. “They’ll put them in the field and if a gust of wind unexpectedly nudges a door open, they tip over,” he says with a chuckle....MORE

Chartology: Crude Oil

WTI has been bouncing between $54 and 48 (approx) I had thought that might change when April became the new front mont but nothing yet.

$49.27 down a penny. We're going lower but it may take until the end of the quarter, futures appear to be levitated at present.

From Nifty Charts:

Descending Triangle and support levels of CRUDE OIL

...MORE

$49.27 down a penny. We're going lower but it may take until the end of the quarter, futures appear to be levitated at present.

From Nifty Charts:

Descending Triangle and support levels of CRUDE OIL

...MORE

Rule Britannia: FTSE Finally Sets a New Record, Now Wot?

Yeah, yeah, never, never, never shall be slaves is wot.

From FT Alphaville:

How to play Footsie

Reminds one of the time Kinsley Amis said about F. Scott Fitzgerald:

From FT Alphaville:

How to play Footsie

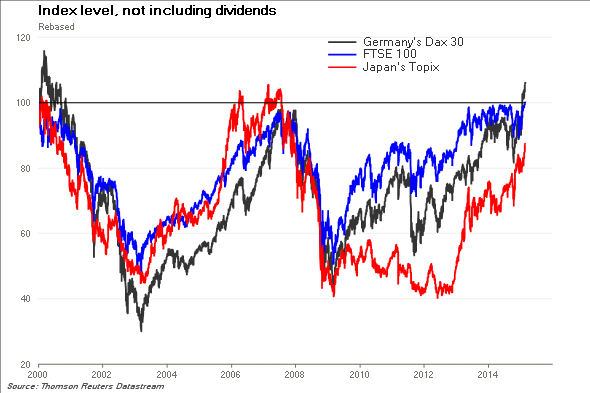

Now the FTSE 100 has broken through to a new high, there are a lot of myths about what it means peddled by people who should know better – including the grand old BBC.

Myth 1: The Footsie’s been really slow to get back to its peak because British shares have done so much worse than those of other countries

The Footsie took 15 years to get back to its high last seen at the end of 1999, which is a long time. Germany’s Dax index, people keep pointing out, made a new post-Lehman high two years ago. The problem is the Dax includes dividends, while the FTSE 100 doesn’t. Calculate the Footsie on the same basis, and it made a new post-crisis high in December 2010.

Here’s what the FTSE 100 and the Dax look like when dividends are excluded: the Dax has recently made a new post-Lehman high, but is still about 10 per cent below its dotcom peak. I added in Japan’s Topix, to make British investors feel good.

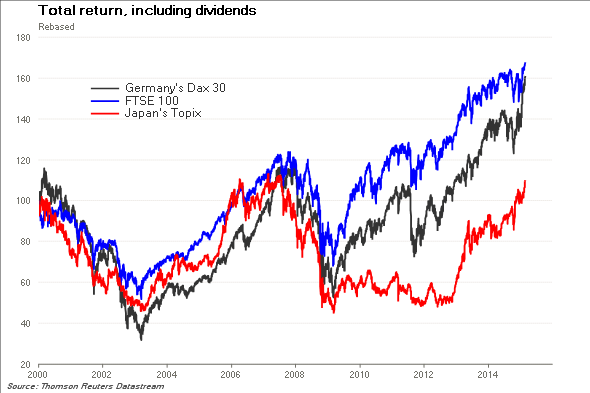

Much more relevant for investors of course is how much they would have made including dividends, since over the long run it is reinvested dividends which provide most of the gain:

Even this is misleading, though. Currency moves have a huge impact, and can’t be ignored. For a British investor who didn’t hedge their currency risk, these are the (sterling-denominated) total returns. I’ve added in the US and France, for a broader comparison: Since the Footsie peaked, US blue-chip shares have done best, then German, British and French, with Japanese stocks almost back up to where they started, in sterling terms. But the US outperformance is really quite recent....MOREI think he's calling Americans upstarts.

Reminds one of the time Kinsley Amis said about F. Scott Fitzgerald:

"...brings a whiff of the parvenu."

Amis ended up living with his first wife's third husband.

Recently:

Amis ended up living with his first wife's third husband.

Recently:

Roman Abramovich Invests $15M In New US Fracking Technology

Do not buy this stock.

I'm posting this as a lead in to some stuff on the oil service companies, NOT as a recommendation of any sort.

Bulletin board stock, away from the market financing, kindly old Russian men, 20 roubles says the smart thing to do is run.

From OilPrice.com:

Why is Russian Billionaire Roman Abramovich Investing in Texas in a New Fracking Technology?

I'm posting this as a lead in to some stuff on the oil service companies, NOT as a recommendation of any sort.

Bulletin board stock, away from the market financing, kindly old Russian men, 20 roubles says the smart thing to do is run.

From OilPrice.com:

Why is Russian Billionaire Roman Abramovich Investing in Texas in a New Fracking Technology?

Are the Russians coming to Texas riding the tailwinds of fracking? That depends on who you ask, as some believe Russian forces were behind the anti-fracking vote in Denton, while a $15 million investment in new Texas fracking technology by Roman Abramovich perhaps tells another story.

When the anti-fracking campaign started to heat up late last year in Denton, Texas—the heart of the shale revolution—conspiracy theories were spread from within the pro-fracking community that the Russians were behind the whole thing. The logic was that the American shale revolution threatened Russia’s market share.

Yet just months after a successful vote to ban fracking in Denton, Russian billionaire Roman Abramovich has invested $15 million in Houston-based Propell Technologies Group, Inc. (OTC:PROP) and its new fracking technology from wholly owned subsidiary Novas Energy. Significantly, this new enhanced oil recovery (EOR) technology enables ‘clean’ hydraulic micro/nano fracturing of oil reservoirs—that is, without water, without polluting chemicals and without earthquakes.HT: Economic Policy Journal

According to Propell, the Plasma Pulse patented downhole tool creates a controlled plasma arc within a vertical well, generating a tremendous amount of heat for a fraction of a second. The subsequent high-speed hydraulic impulse wave emitted is strong enough to remove any clogged sedimentation from the perforation zone without damaging steel. The series of impulse waves/vibrations also penetrate deep into the reservoir causing nano fractures in the matrix which increase reservoir permeability for up to a year per treatment....MORE

Tuesday, February 24, 2015

"First Solar, Inc. Announces Fourth Quarter and Full Year 2014 Financial Results" (FSLR)

The after-hours reaction is muted, down 7 cents at $54.63.

Conference call at 4:30 PM EST, more to come.

From the company:

Conference call at 4:30 PM EST, more to come.

From the company:

TEMPE, Ariz.--(BUSINESS WIRE)-- First Solar, Inc. (Nasdaq: FSLR) today announced financial results for the fourth quarter and year ended December 31, 2014. Net sales were $1,008 million in the quarter, an increase of $119 million from the third quarter of 2014. The sequential increase in net sales resulted from the sale of the Solar Gen 2 project, initial revenue recognition on the Silver State South project and other projects under construction. Revenue recognition from the Desert Sunlight and Topaz projects were lower as the projects reached completion.

- Net sales of $1.0 billion for the fourth quarter and $3.4 billion for 2014

- GAAP earnings per fully diluted share of $1.89 for the fourth quarter and $3.91 for 2014

- Cash and marketable securities of $2.0 billion, net cash of $1.8 billion

- 2014 full year bookings of 2.5GWdc; 2015 year-to-date bookings of 311MWdc

The Company reported a fourth quarter GAAP earnings per fully diluted share of $1.89, compared to earnings of $0.87 in the prior quarter. The increase in net income compared to the prior quarter was due to higher profit from the sale of the Solar Gen 2 project and project cost improvements.

Cash and marketable securities at the end of the fourth quarter were approximately $2.0 billion, an increase of approximately $876 million compared to the prior quarter. Cash flows from operations were $928 million in the fourth quarter. The increase in cash and marketable securities during the quarter was due to the sale of the Solar Gen 2 project and the collection of retention payments on the Topaz and Desert Sunlight projects....MORE

"Wait For the ‘Second Low’ Before Buying Energy Stocks" (XLE; XOP)

After touting the hydrocarbon equities for the last six months, Barron's may have caught on to the fact that the decline in prices is a sea-change and that listening to some hipster analyst, whose long-term frame of reference maybe goes back to 2009 and who may not have the intellectual chops to figure it out, might prove dangerous to their readers.

XLE $80.34; XOP $51.69; WTI $49.17.

Good on Ben Levisohn for posting this, the first cautionary piece I can remember.

From Barron's:

XLE $80.34; XOP $51.69; WTI $49.17.

Good on Ben Levisohn for posting this, the first cautionary piece I can remember.

From Barron's:

Should investors be betting in a bottom on energy-sector stocks like ExxonMobil (XOM), Chevron (CVX) and ConocoPhillips (COP)? Not if some recent observations are correct....MORE

Sure, oil seems to have bottomed. But Evercore ISI’s Ed Hyman notes that energy stocks usually lag the recovery in oil prices. He explains:

In the Past, Shares of Oil Companies Have Tended to Lag the Lows In Oil - The six previous V-shaped bottoms in oil started out U-shaped and double-bottomed. The bottoms took roughly two months to form. In every case, shares of oil companies bottomed coincident with or after the second low in oil. That is, you could have waited to see the second low in oil before buying the shares.Cumberland’s David Kotok explains why he remains underweight Energy in client portfolios:

We are underweight the Energy sector in the US stock markets and the rest of the world. We hold this underweight position because we are not convinced that a bottom has occurred in the oil price. In the scenarios that we envision, we see more downside risk to the price than upside potential. That said, there are some scenarios with a strong upside, but they are event-driven, and the events are not predictable as to time or magnitude.....

"The Fed Is Not Going To Hike Interest Rates, Not Now, Not Ever"

From iBankCoin:

You Will Lose Betting Against Governments

Who's Afraid of Janet Yellen?

You Will Lose Betting Against Governments

Big moves happening in the solar sector today. I would not chase those fuckers after such a run higher. Although I liked the airlines, I’ve convinced myself that crude is going to bounce this week. As such, I eliminated my exposure to the airlines and added to my oil longs. The QIWI position is nothing more than a play off Russia. Given my bullish position in crude, I figure Russia will bounce with stronger oil prices. Plus anyway, QIWI is trading at a 50% discount to where it was trading last year, in terms of PE and P/S ratios.See also MacroBusiness:

Everyone expected Yellen to disappoint today. I think the speech went well and there is no fucking way the Fed tightens now, as the CRB index hits 1996 lows. I’ll say it again and to the point: THE FED IS NOT GOING TO HIKE INTEREST RATES, NOT NOW, NOT EVER, ESPECIALLY WHEN WE ARE FIGHTING DEFLATION.

What if they did hike rates?...MORE

Who's Afraid of Janet Yellen?

Precisely nobody, with markets bid across the board as she warned in Congress:

The FOMC’s assessment that it can be patient in beginning to normalize policy means that the Committee considers it unlikely that economic conditions will warrant an increase in the target range for the federal funds rate for at least the next couple of FOMC meetings. If economic conditions continue to improve, as the Committee anticipates, the Committee will at some point begin considering an increase in the target range for the federal funds rate on a meeting-by-meeting basis. Before then, the Committee will change its forward guidance. However, it is important to emphasize that a modification of the forward guidance should not be read as indicating that the Committee will necessarily increase the target range in a couple of meetings. Instead the modification should be understood as reflecting the Committee’s judgment that conditions have improved to the point where it will soon be the case that a change in the target range could be warranted at any meeting....MORE

Some Details on Porsche's Tesla-fighter: 600 Horsepower...

From autoblog:

Porsche's Tesla-fighter could have 600 hp and 300-mile range

Porsche's Tesla-fighter could have 600 hp and 300-mile range

Will this be the Ragin' Pajun? Some details on the all-electric "Tesla fighter" from Porsche have been revealed by UK's Car magazine, and, to put it bluntly, the model that has preliminarily been dubbed the 717 will be an absolute beast when it hits the road as early as 2019.

With some technological help from parent company Volkswagen, Porsche is planning a model that will have about a 300-mile single-charge range, and a version that may deliver as much as 600 horsepower. The four-door will also be four-wheel-drive, with one electric motor per axle, and four-wheel steering, all for the sake of consistency, Car says....MORE

International Tech City Metrics

From the Wall Street Journal's Venture Capital Dispatch:

Austin Beats San Francisco in Savills’ Tech City Metrics

Austin Beats San Francisco in Savills’ Tech City Metrics

San Francisco may have cool startups and some of the biggest names in the technology business, but when compared with 11 other global cities with strong tech clusters, the city that is home to Silicon Valley under-performs in key metrics like business environment, quality of life and property prices, according to a new report by property consultants Savills.

Measured against five metrics, San Francisco came fifth on business environment; fourth on tech environment; second on quality of life; sixth on talent pool and 8th in property affordability.

Austin, Texas, came first in the overall ranking. “It’s got the talent,” said Paul Tostevin, lead research analyst for Savills.

Mr. Tostevin said there is “a herd effect” when it comes to living in San Francisco. “As the most established tech center, there is a large pre-existing pool of talent in San Francisco. For a company looking for experienced employees… this is the place to be,” he said.

Israeli-born Sagi Shorrer, co-founder of London-based Brainbow Ltd., developer of a brain-training app called Peak, said that while he’s happy in London, a move to San Francisco makes sense for his firm. Mr. Shorrer highlights proximity to venture capitalist, access to early adopters that test products, and top talent to recruit. However, he also sees some downsides, including cost of talent and office space. Still, San Francisco has a “strong appeal of course,” he said.

Amongst the 12 cities surveyed on four continents, Austin, which is a big student city, also has some of the youngest pool of talented people, Mr. Tostevin said. Tel Aviv, New York and Stockholm, each with its own growing tech sector, came third, fourth and fifth respectively in the overall ranking.

The survey pulled data on measures like business costs, talent pool and tech infrastructure from government statistics, population census and forecasts around age and population all the way through 2024....MORE

The Softer Side Of Goldman: "...human beings as our greatest resource, and from time-to-time, they make mistakes" (GS)

From Footnoted:

Goldman Sachs says “People are People”

Goldman Sachs says “People are People”

Buried in the 405-page tome that Goldman Sachs filed at 9:44 pm last Friday several hours after the SEC closed its electronic window, which means the filing did not become publicly available until Monday morning was a very interesting (and new) disclosure that provided some insight into the company’s view of the world and should be welcome news to Goldman’s 34,000 employees.

In an age of high frequency trading and big data, the company said that human beings are the company’s greatest resource.

This disclosure came buried at the bottom of a 1,500 word risk factor on cyber-security attacks a risk factor that has grown significantly at many companies this 10-K season, mostly because of the growing number of high-profile attacks on companies including Sony, JP Morgan Chase, Home Depot and Target.

While little of Goldman’s risk factor related to cyber attacks was new, the part about humans was. Here’s the new disclosure in its entirety:

Notwithstanding the proliferation of technology and technology-based risk and control systems, our businesses ultimately rely on human beings as our greatest resource, and from time-to-time, they make mistakes that are not always caught immediately by our technological processes or by our other procedures which are intended to prevent and detect such errors. These can include calculation errors, mistakes in addressing emails, errors in software development or implementation, or simple errors in judgment. We strive to eliminate such human errors through training, supervision, technology and by redundant processes and controls. Human errors, even if promptly discovered and remediated, can result in material losses and liabilities for the firm.When we first read this, we couldn’t help but reminisce about our college days listening to Depeche Mode.

Not only was this the first time that a company like Goldman mentioned its employees like this in one of their filings, it was also the first time the company mentioned the possibility of human error....MORE

After 8 centuries, Rats Exonerated in Spread of Black Death. It May Have Been Their Cute Cousins, the Gerbils

From the Washington Post:

After nearly eight centuries of accusations for spreading the bubonic plague, scientists say they have compelling evidence to exonerate the much-maligned black rat. In the process, they’ve identified a new culprit: gerbils.

It’s always the cute ones you have to watch out for, isn’t it?

According to a study published in the Proceedings of the National Academy of Sciences, climate data dating back to the 14th century contradicts the commonly held notion that European plague outbreaks were caused by a reservoir of disease-carrying fleas hosted by the continent’s rat population.

“For this, you would need warm summers, with not too much precipitation,” Nils Christian Stenseth, an author of the study, told the BBC. “… And we have looked at the broad spectrum of climatic indices, and there is no relationship between the appearance of plague and the weather.”

Instead, the fearsome “Black Death,” as the epidemic was known, seemed curiously tied to the climate in Asia. Analysis of 15 tree-ring records, which document yearly weather conditions, shows that Europe always experienced plague outbreaks after central Asia had a wet spring followed by a warm summer — terrible conditions for black rats, but ideal for Asia’s gerbil population. Those sneaky rodents and their bacteria-ridden fleas then hitched a ride to Europe via the Silk Road, arriving on the continent a few years later to wreak epidemiological havoc....MORE

Ahead of the Report: "Fed Chief Yellen Will Dampen Expectations of a June Rate Hike"

From LearnBonds:

Five charts to help the Yellen-fest

Federal Reserve Chair Janet Yellen is scheduled to deliver the central bank’s semi-annual economic report to the U.S. Congress at 10:00 AM ET on Tuesday. Analysts and investors will focus on Yellen’s testimony for further clues on when the Fed will hike interest rates. Yellen is likely to give away very little in her prepared testimony to the Senate Banking Committee. But her answers to lawmakers’ questions will be critically dissected to get an insight into her views on the weak inflation and stagnant wage growth. The minutes from Fed’s January policy meeting revealed that a mid-year rate hike was highly unlikely. But events since that meeting, especially the robust January jobs report, may have altered the views of quite a few Fed officials....MOREAnd From FT Alphaville:

Five charts to help the Yellen-fest

As Fed Chair Janet Yellen prepares to answer questions from members of the US Senate’s banking committee on Tuesday, understanding the background is vital. Here are some charts presenting alternative measures Wall Street (mostly) hasn’t been looking at.

First, if you’re worrying about the deflation in the eurozone, the US is no different. Eurozone inflation is calculated without taking account of housing costs. Put the US on the same basis by stripping out “imputed rent” (calculated by surveys, complex maths and a finger in the air) and the US has exactly the same deflation problem as Europe....MORE

"...Japan’s Best Strategy to Defeat China at Sea"

From The Diplomat:

In order to win, Japan should give China a dose of its own medicine.

In order to win, Japan should give China a dose of its own medicine.

The Japanese Maritime Self-Defense Force (JMSDF) is a highly capable navy, although it is the smallest of Japan’s military branches. It is technologically more advanced, more experienced, and more highly trained than its main competitor – the People’s Liberation Army Navy (PLAN). Yet, in the long-run, the JMSDF and the Japanese Coast Guard (JCG) – Tokyo’s principle enforcer of maritime law – are at a relative disadvantage if one looks at the bourgeoning naval rearmament program of China, which is gradually shifting the regional maritime balance in Beijing’s favor.

“From a military perspective, Tokyo is becoming the weaker party in the Sino-Japanese rivalry,” argues Naval War College professor Toshi Yoshihara, in a 2014 report by the Center for a New American Security (CNAS). “Japan (…) finds itself squeezed between China’s latent military prowess that backs up Chinese coercion over the Senkaku/Diaoyu Islands dispute and China’s ability to disrupt access to the global commons should conventional deterrence fail,” he further notes.

According to the Institute of International Strategic Studies, China’s share of regional military expenditure rose from 28 percent in 2010 to 38 percent in 2014 totaling $129.4 billion. In contrast, in Japan, despite fears of resurgent militarism under Shinzo Abe, regional share of expenditure fell from 20 percent in 2010 to less than 14 percent in 2014, leaving Tokyo’s defense budget at $47.7 billion.

Given Tokyo’s apparent relative decline in military strengths what is the JMSDF’s best strategy for confronting China in the years ahead?

According to Toshi Yoshihara, it is an anti-access operational concept with Japanese characteristics. In short, Japan should give China a dose of its own medicine and emulate the PLAN’s alleged anti-access/area denial (A2/AD) strategy (although there is little actual evidence that the Chinese Navy is placing a high priority on such a strategy. See: “The One Article to Read on Chinese Naval Strategy in 2015”). An A2/AD operational concept with Japanese characteristics would take into account Japan’s role as a gatekeeper to the open waters of the Pacific and would center around exploiting Japan’s maritime geographical advantage over China by skillfully deploying the JMSDF along the Ryukyu Islands chain, bottling up the PLAN in the East China Sea until the U.S. Navy and other allied navies can deploy in full-strength....MORE

"Anti-Aging Experts Made a Million-Dollar Bet on Who Dies Last"

From Gizmodo:

...MOREEven 10 years ago, the idea of reversing aging and conquering human mortality was still fringe science, seen as snake-oil research by most scientists, large pharmaceutical companies, and the public. What a difference a decade makes. Anti-aging science is poised to become a major industry in the biotech world.To prove its promise, the first million-dollar bet on who can live the longest (for company stock—a signed deal likely made public later this week) was recently struck. It was made last month by two leading longevity advocates at the biggest annual healthcare investing event of the year, the JPMorgan Health Care Conference.Dmitry Kaminskiy, senior partner of Hong Kong-based technology venture fund, Deep Knowledge Ventures, and Dr. Alex Zhavoronkov, PhD, CEO of bioinformatics company Insilico Medicine Inc. which specializes in drug discovery and drug repurposing for aging and age-related diseases, signed a wager to indicate exactly how sure they are that science is turning the tide against the eternal problem of human aging.The terms go like this:- If one of the parties passes away before the other, $1 million dollars in Insilico Medicine stock will be passed to the surviving party- The agreement will vest once both parties reach 100 years- Parties agree not to accelerate each other's demise (i.e. try to kill each other)

Sunpower Reports Earnings (meh) Merrill Surprised By Scope of JV Yieldco Plans (SPWR)

Here are SPWR's Q4 and Year End 2014 numbers, good, not great. The stock is up 16.44% at $32.37.

From Barron's:

First Solar Up 14%, SunPower Up 16% on YieldCo. Plan; Merrill Surprised by the Scale

From Barron's:

First Solar Up 14%, SunPower Up 16% on YieldCo. Plan; Merrill Surprised by the Scale

Shares of solar energy technology provider First Solar (FSLR) are up $6.87, or up 14%, at $56.61, and SunPower (SPWR) stock is up $4.40, or almost 16%, at $32.20, after the two yesterday afternoon said that they will merge certain assets into a publicly traded YieldCo.

Among the initial responses this morning is Krish Sankar of Merrill Lynch, who has an Underperform rating on First Solar and a Buy on SunPower, writes that “the potential scale of this vehicle, not to mention the implications for each development company, comes as a surprise.”

“Nevertheless this is likely to be viewed as a positive catalyst for each stock in the near-term,” he believes.

There are some concerns, such as the seasonality of solar, and the divergent tech approaches of the two firms in the solar energy field:

One obvious attribute of the proposed YieldCo is that it will be solar focused, at least in its early years. Most of the initial assets contributed to the company are likely to be North America-based, which means that there could be significant seasonality to distributable cash generation. Another consideration is the implication for each integrated development company considering their divergent solar technology bets, ownership structures, and business models. Finally, management of the combined entity, and how inherent conflicts of interest between First Solar and SunPower, and between general and limited partnership unit holders will be addressed and mitigated are key concerns, in our view.Sankar does some back-of-the-envelope math on what the two will contribute...MORE

"First Solar, SunPower Ink Deal For YieldCo" IPO, Stocks Soar (FSLR; SPWR)

Just like old times, 10%+ moves just to make sure you're paying attention.

In pre-market trade FSLR up 14% at $56.59, SPWR up 15.61% at $32.14.

SunPower will be releasing earing in a few minutes.

More to follow.

From Investors Daily via Yahoo:

In pre-market trade FSLR up 14% at $56.59, SPWR up 15.61% at $32.14.

SunPower will be releasing earing in a few minutes.

More to follow.

From Investors Daily via Yahoo:

Solar panel manufacturers First Solar (FSLR) and SunPower announced Monday they're in "advanced negotiations" to form a joint, publicly traded yield company that would own and operate solar-power assets to generate revenue for investors.

The companies could use capital generated from the "yieldco" to fund new power projects, a growing trend in the industry.The two companies said in a statement they intend to file a registration statement with the Securities and Exchange Commission for an initial public offering for the yieldco. The companies didn't offer a time frame or say how much they would seek to raise through the IPO....MORE

The Riddle of Tampa Bay: Two of The Best Stock Pickers Of All Time

From Chief Investment Officer:

Harold and Jay Bowen who alone have managed billions for Tampa's police and firefighters for forty years may be two of the greatest stock pickers of all time. So why don't they act like it?

Harold and Jay Bowen who alone have managed billions for Tampa's police and firefighters for forty years may be two of the greatest stock pickers of all time. So why don't they act like it?

HT: The Big PictureCrime seems a mild affair in Lady Lake, Florida.Home to the world’s largest retirement community, the town sits a lazy 90 minutes northeast of Tampa Bay. Given the demographics, the local police force is compact. Recent criminal activity includes a counterfeit $50 bill proffered at the local dog groomers, several golf cart-related DUIs, and a scammer pretending to be retirees’ grandson asking for $2,000 to repair his car. Miami, it is not.

Like the larger force down the road in Tampa, the police tasked with protecting the citizens of Lady Lake from such scourges have a pooled investment account that will one day pay for their retirement. And like the police of Tampa, they have for years entrusted 100% of this money to a single manager: Bowen, Hanes & Co. of Atlanta, Georgia.

Or, at least, they used to.

On June 12, 2013, Lady Lake’s Police Pension Board gathered in the town hall for what was supposed to be a typical quarterly meeting. Four board members and three town staffers were present, along with the fund’s lawyer and its investment consultant, David West. Also present was their money manager, represented by Bowen, Hanes’ deputy David Kelly.

Public pension board meetings are predominantly dreary affairs. Consultants deliver the latest investment figures; managers review markets; invoices get approved; board members occasionally nod off. But by the time consultant West of the Bogdahn Group mentioned he had “an administrative item to bring up,” no one was sleeping.

West’s firm had been looking into Bowen, Hanes’ investment practices on behalf of a number of public pension clients. What it found was troubling.

Bowen, Hanes “do not appear to be keeping up with other managers’ industry standards, trading procedures, and compliance procedures,” West said. Bogdahn had been “comparing other managers’ operational procedures to Bowen, Hanes’,” and found the latter lacking. A state-of-the-art back office system “minimizes error, potential error, and provides for more sound accounting, fair allocation of trades, and minimizes dispersion.” Bowen, Hanes had no such system in place.

West told the board that he had no issue with the manager’s long-only investment strategy, and stated that “they are not doing anything illegal.” Even the recent lagging performance would not justify what amounted to an exceedingly rare move by a consultant to recommend firing a fund’s primary manager. Bogdahn’s issues with Bowen, Hanes were administrative, West said, not personal. Although the firm’s dated website advertises that it sets “the industry standard from a trading and portfolio accounting standpoint,” Bogdahn felt otherwise. “Bowen, Hanes’ operational infrastructure is lacking in state-of-the-art systems for portfolio compliance procedures and trade settlement procedures,” West said. For this reason, he advised Lady Lake to find new money management.

Then, incredibly, things got even weirder.

Bowen, Hanes’ Kelly asked the pension’s lawyer how often Bogdahn or any investment consultant really needed to be involved with the fund. State law required once every three years, the attorney said, but it was his “opinion that having a third-party consultant reporting on the manager’s performance is a prudent thing to do.”

Kelly disagreed. “Every three years is enough,” he argued. Kelly had handed out a letter from his firm’s president detailing issues between Bowen, Hanes and Bogdahn, who share a number of clients. The money manager had made a decision not to actively engage and work with investment consultants, including Bogdahn—a move unheard of in this industry.

Then came the ultimatum: “If the board chooses to go the multi-manager route with Bogdahn Group quarterbacking the plan, then Bowen, Hanes will resign.”

Lady Lake’s lawyer, likely incredulous at this turn of events, tried to clarify what was happening. “Mr. Kelly,” he asked, “if the board keeps the Bogdahn Group as its consultant, will Bowen, Hanes then resign as the fund’s manager?”

Yes, Kelly confirmed.

Lady Lake fired Bowen, Hanes. A few months later, taking Bogdahn’s recommendation, the board invested its $5 million between two new managers.

Like a bad rash, Bogdahn’s consultants have stayed on Bowen, Hanes, advising public pension clients across the state of Florida to take their money elsewhere. Although the consulting firm’s president declined an interview, public records attest to an effective campaign. The City of Hollywood’s Firefighters’ fund pulled its entire $15 million investment in 2012. In 2013, Venice’s police pension board voted 5-0 to heed Bogdahn’s advice and look at new management options. And just a few months ago, a Bogdahn consultant urged the City of Edgewater’s $10 million firefighters’ fund to rethink the risk it shouldered by having all its eggs in Bowen, Hanes’ basket.

But at one of the largest retirement funds in the state—the $1.9 billion Tampa Fire & Police Pension—there’s no Bogdahn to press this message.

Since 1974, Tampa has done what most in the industry consider unthinkable. Casting aside the sacred tenet of diversification, the fund’s board entrusts all of its members’ retirements with a single money manager. And Harold ‘Jay’ Bowen III—and his father Harold Bowen II before him— have delivered, fabulously so.

Tampa’s 12.3% annualized returns under Bowen, Hanes make it not only the most strangely managed public pension in America, but also perhaps the best performing. The massive and acclaimed Ontario Teachers’ Pension Plan think Harvard to Bowen, Hanes’ community college touts itself as the highest earner among major institutional investors worldwide. But the five-person shop in Atlanta beats Ontario Teachers’ in the short game (22.1% to 10.9% last reporting year) and the long (9.8% versus 8.9% over 10 years)....MORE

Subscribe to:

Comments (Atom)