Now, if the Fed could do something about the job market. (but I don't think they can)

From Wolf Street, November 4:

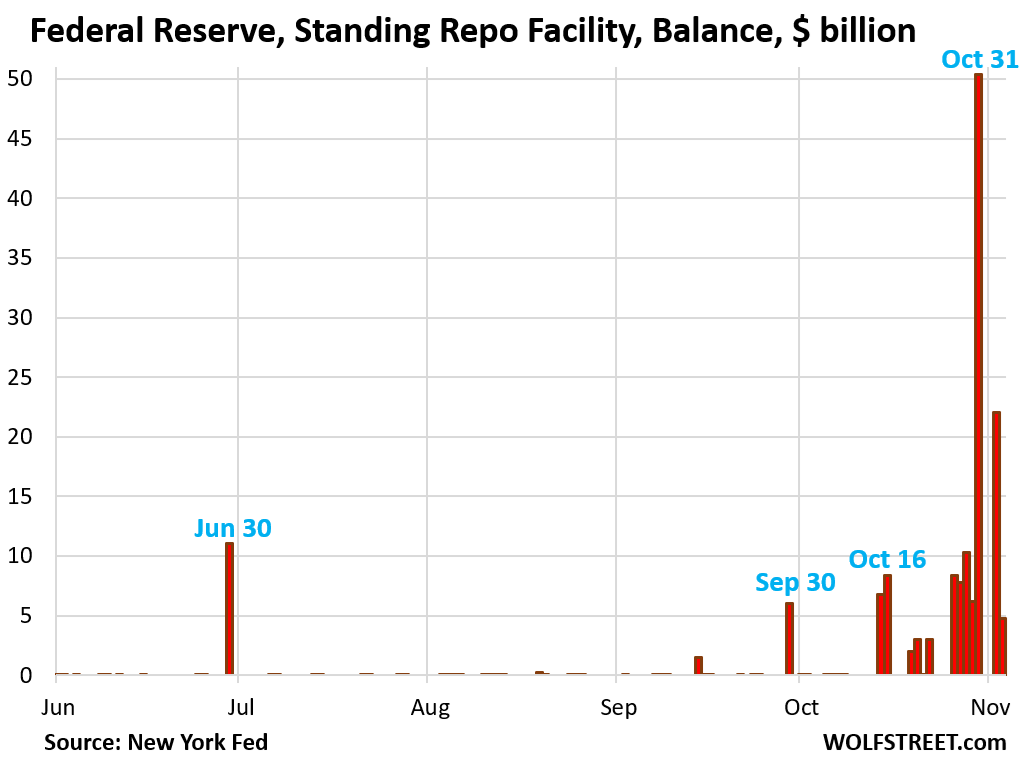

The uptake at the Fed’s Standing Repo Facility (SRF) plunged to $4.8 billion today: $2.8 billion at the morning auction and $2.0 billion at the afternoon auction. The approved counterparties at the SRF are big banks and broker-dealers.

This was down from $22.0 billion on Monday, and from $50.4 billion on Friday, which had been a record of this new facility that the Fed revived in July 2021.

These repos (“overnight repurchase agreements”) will mature on Wednesday, when the Fed gets its $4.8 billion back and the banks get their collateral back. The collateral is Treasury securities and government-guaranteed “agency MBS.” The $50 billion in repos taken on Friday matured on Monday, when the Fed got its $50 billion back and the banks got their collateral back. So that liquidity that these repos provided on Friday got reversed on Monday. Then on Monday, $22 billion in new repos were taken, and that liquidity was reversed today. And today’s $4.8 billion in liquidity will be reversed tomorrow. The total balance outstanding at the SRF is now $4.8 billion.

The purpose of the SRF is to provide liquidity to banks and dealers so that they can lend to the repo market. This is a profitable trade when repo market rates are significantly higher than the Fed’s rate at the SRF (currently 4.0%). And repo market rates have been higher in recent weeks.

Repo rates. The Secured Overnight Funding Rate (SOFR), which tracks a $3-trillion-a-day segment of the repo market, declined to 4.13% on Monday, from 4.22% on Friday (the NY Fed will release today’s rate tomorrow)....

....MUCH MORE

Previously:

Federal Reserve Repo Operations: It's Probably Nothing